In summary

| 🚗 Section | 🧾 Content |

|---|---|

| Auto insurance objective | Protect the driver and the third parties in case of an accident |

| Main policies | Third-party, Enhanced third-party, All risks |

| Current coverages | Civil liability, glass breakage, theft, fire, all accidents damages |

| Bonus-Malus | System of discount or surcharge based on driving behavior |

| Optional coverages | Legal protection, 0 km assistance, driver protection, transported objects |

| Important exclusions | Alcohol, invalid license, false declarations, misuse, fraud |

| Practical cases | Concrete examples: third-party accident, fire, glass breakage, theft of objects |

| Choosing your policy | Compare the actual needs and offers using a comparison tool |

| Steps in case of a claim | Secure, inspection report, quick declaration, documents, assessment, compensation |

| FAQ | Answers to frequently asked questions: third-party vs all risks, bonus-malus, useful coverages |

Auto insurance holds an essential place in the daily lives of French drivers. Mandatory for all motor land vehicles, it constitutes an important financial and legal protection in case of accidents, theft, or damages. Between different coverage options, additional options, and the bonus-malus system, it’s not always easy to navigate.

In this article, we will review the essential basics of auto insurance: its purpose, main policies, key coverages, as well as best practices to choose the most suitable contract for your profile. Whether you are a young driver, an insurance student, or simply curious to better understand your policy, this guide will give you a clear and structured overview to master the fundamentals.

What is auto insurance used for?

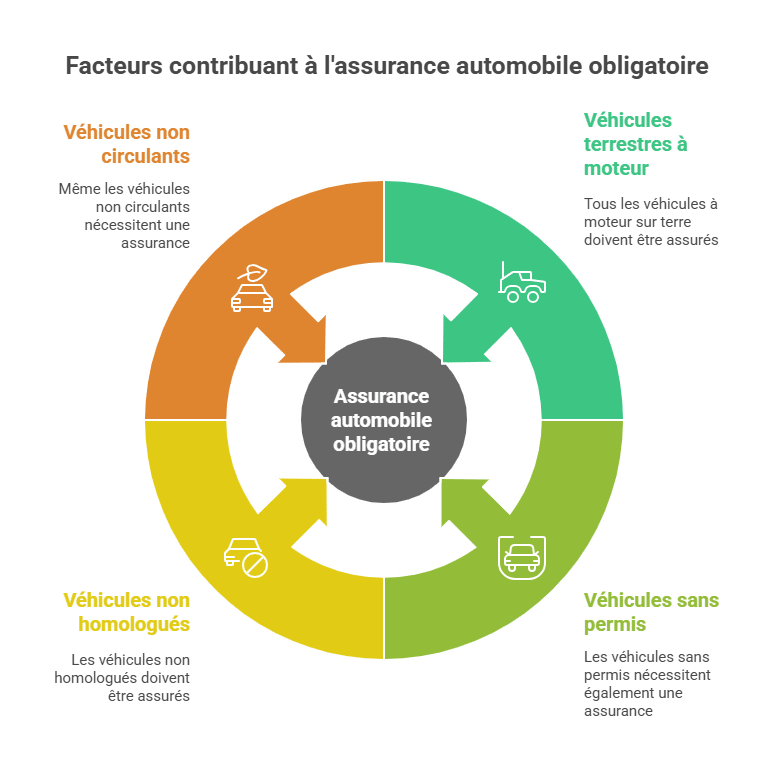

Insurance is ubiquitous in the daily lives of the French. Auto insurance is a guarantee that provides coverage in case of a claim. In many situations, auto insurance helps you face difficulties. There is an obligation to insure all motor land vehicles, such as:

- utility vehicles,

- two- and three-wheeled vehicles,

- motorcycles and scooters,

- quad bikes,

- even riding mowers.

This obligation extends to vehicles:

- without a license,

- to non-approved two- or three-wheelers (mini-motorcycles),

- as well as vehicles that do not circulate. Such as collectible vehicles.

What does an auto insurance contract consist of?

In most companies, we find 3 coverage options:

Third-party policy:

The insurance that every driver must have is the civil liability coverage. This coverage protects against damages that the driver or drivers of the vehicle could cause to others. Damages can be to a pedestrian, another vehicle, or to the passenger in the car.

This policy also includes a defense and recourse coverage. This coverage helps cover some legal expenses in case of a dispute. The defense and recourse guarantee only applies with the relevant contract.

For example, if you have a defense and recourse coverage with your auto policy, it will only intervene for disputes related to that policy.

The third-party policy allows paying the minimum insurance premium. Insurers recommend this insurance for young drivers with old cars. A low premium means less coverage.

Enhanced third-party policy:

This policy includes the same guarantees as the third-party policies. Fire, glass breakage, and theft coverages are added.

The fire and theft guarantees will compensate the insured up to the value of their vehicle on the day of the fire or theft. This value is called the market value, corresponding to the vehicle’s value on the used car market.

It mainly depends on the vehicle’s age and mileage. Experts setting the market value rely on the “Argus quote”. It is a reference used by professionals in the automotive sector.

Note: for cars over 30 years old that are not collectibles, since they are no longer listed in the Argus, the expert cannot reference the Argus. Instead, they will consult the used car market data for this type of vehicle.

Here are some examples of cars over 30 years old that are no longer listed in the Argus: Citroën BX, Renault 25.

Glass breakage guarantee

The glass breakage guarantee covers breakages or replacement of your windshield. This coverage is not very expensive and is available starting from the enhanced third-party policy. Make sure to verify whether your policy covers mirrors and panoramic roofs, as some insurers do not include these elements. Often, the glass breakage guarantee is offered with a zero euro deductible.

When replacing a windshield, there may be a deductible at your expense. However, repairs at an insurer-approved center cost nothing. Certain conditions apply, such as the impact being smaller than a 2-euro coin and outside the driver’s field of view.

The compensation is never immediate: the deadline for finalizing the claim is detailed in the contract, typically around one month.

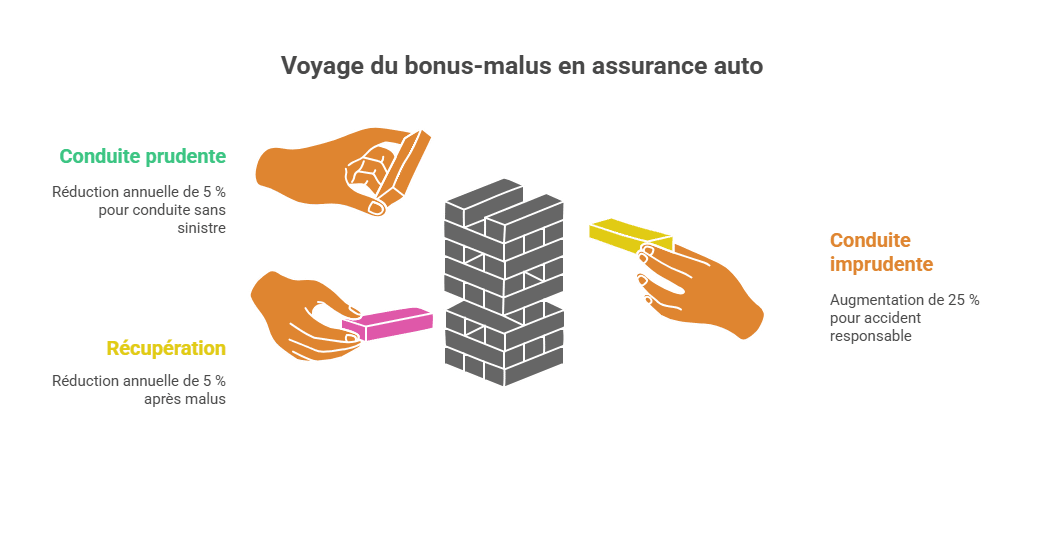

📊 The Bonus-Malus system in auto insurance

The bonus-malus system is one of the most influential elements in determining your auto insurance premium. It involves a reduction or increase applied to your annual premium, depending on your driving record over the past year.

➕ The bonus: reward for good driving

Each responsible accident free year results in a 5% reduction of your premium, calculated on the current coefficient. The starting coefficient is 1.00, and the bonus can decrease to 0.50, which means a maximum 50% reduction on the premium.

Example:

-

1st responsible accident year → coefficient 0.95

-

5th accident-free year → coefficient 0.77

-

13 years accident-free → coefficient 0.50 (legal maximum)

➖ The malus: penalty in case of responsible accident

Each responsible claim leads to a 25% increase in the coefficient. The coefficient can go up to 3.50, which can more than triple the premium amount.

-

A responsible claim with a coefficient of 1.00 → increases to 1.25

-

Two claims within a year → coefficient multiplied by 1.25 twice

🔄 Returning to a bonus after a malus

In the absence of new claims, the coefficient decreases by 5% annually after a malus. After 2 years without an accident, the malus is removed (returning to 1.00).

📌 Evolution example

| Year | Responsible claims | Applied coefficient | Impact on premium |

|---|---|---|---|

| 1 | 0 | 1.00 → 0.95 | -5% |

| 2 | 0 | 0.95 → 0.90 | -5% additional |

| 3 | 1 | 0.90 → 1.125 | +25% |

| 4 | 0 | 1.125 → 1.06875 | gradual decrease |

| 5 | 0 | 1.06875 → 1.0153 | gradual return to 1.00 |

👉 For young drivers, the bonus-malus can significantly vary the premium over the years. Therefore, adopting cautious driving from the outset is essential.

Recovery costs with your insurer’s approval

Restoration costs with an appraisal and within the market value limit

For the theft guarantee to activate in case of attempted theft, the insured must provide material proof of the attempt (forced lock, broken windows, disassembled anti-theft device, witnesses, etc.) Only the restoration cost is indemnified.

– If the vehicle is found after one month, the owner can abandon or decide to buy back the vehicle from the insurer by reimbursing the sums received.

– The insurer may require the insured to install a GPS tag to facilitate recovery. For cars valued at over €70,000, this installation will always be required.

– Beware of false declarations, which many people do to pay a few euros less on their premium. If during subscription you declared your vehicle was parked in a closed garage but it was actually parked on the street, in front of your home.

– Typically, valuable items are not covered unless specific protection has been purchased. Some parts of the vehicle, such as the battery, are also not guaranteed.

In case of a claim, your bonus will not change, but insurers will compensate by raising your premium, increasing it.

All-risk insurance covers damages caused by your own fault.

All-risk policy:

This policy includes the same guarantees as the enhanced third-party policy, with the addition of all-accidents damage coverage and new car replacement within 24 or 36 months.

The all-accidents damage guarantee covers damages even if you are responsible. For example, a typical case: you collide with a retractable barrier, damaging your bumper. The insurance will cover the damage amount exceeding the deductible. Suppose you have a €150 deductible and damages total €300. The insurer pays €150, your responsibility, and you cover the remaining €150.

New car replacement guarantee

This guarantee is available for new vehicles or those in circulation for less than 24 or 36 months, depending on the insurer. After theft or total destruction, the insured can choose to:

- Replace the damaged car with a new vehicle of the same value;

- Or, get reimbursed the purchase price of the vehicle.

To learn how to determine your indemnity entitlement after a claim, click here.

If you want to understand the claims management process, click here.

You now have the basics of auto insurance.

Thank you for reading this article. Remember, you can receive review questionnaires by clicking the button below.

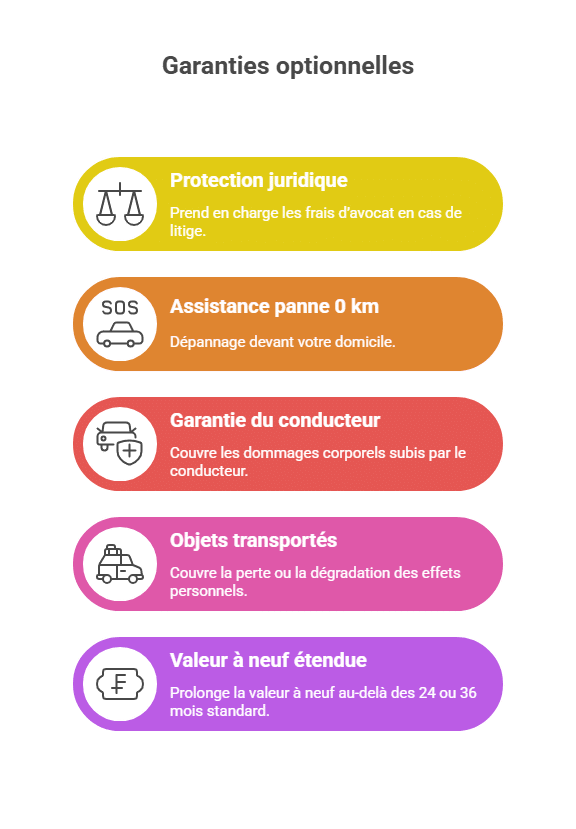

Optional coverages

🧾 Important optional coverages to know

In addition to basic policies, insurance companies often offer optional guarantees. They help tailor the contract to each driver’s specific needs.

🧑⚖️ Legal protection

This guarantee covers lawyer fees, assessments, or legal proceedings in case of disputes (e.g., after an accident or responsibility challenge). It offers valuable legal assistance, particularly in cases of conflicts with a third party or administration.

🚐 0 km breakdown assistance

Unlike standard roadside assistance, this option provides on-site help at your home. It is very useful for older vehicles or in case of unforeseen immobilization.

🚑 Driver protection

Often overlooked, this guarantee covers injuries to the driver, which are not covered by civil liability. It can include compensation in case of disability or death.

💼 Transported objects

It covers loss or damage to personal effects left in the car (laptop, bag, suitcase…), provided they are properly secured.

🆕 Extended new value

Some companies allow extending the new value coverage beyond the standard 24 or 36 months. This ensures, in case of total loss, compensation equivalent to the original purchase price, even years later.

👉 These options are especially appealing for frequent drivers, families, or owners of new vehicles.

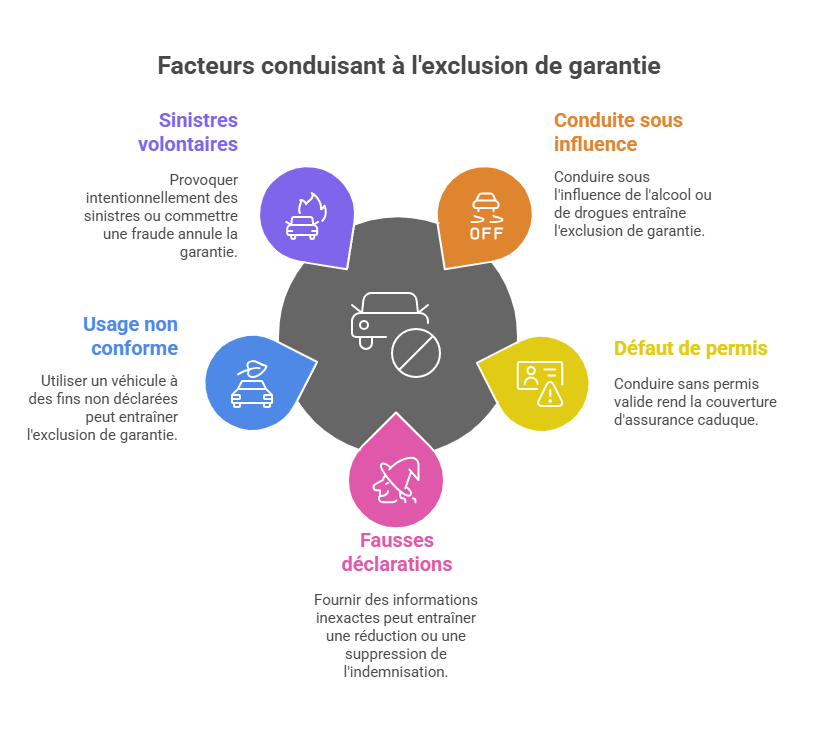

Coverage exclusions

⚠️ Important coverage exclusions to understand

Auto insurance policies do not cover all situations. Some legal or contractual exclusions result in complete non-coverage, even if you are insured.

🚫 Driving under the influence of alcohol or drugs

This is an automatic exclusion: no reimbursement is provided if the driver is at fault.

🚗 Disqualification or license withdrawal

The insurance becomes void if the involved driver does not possess a valid license at the time of the claim.

📝 False declarations

For example, declaring that your vehicle is parked in a closed garage when it was actually on the street in front of your house can lead to a reduction or denial of compensation.

💼 Non-compliant use

Using a vehicle declared for “personal” use in a professional setting without informing the insurer may be considered a false declaration.

🔥 Voluntary claims or fraud

Any attempt of fraud or intentionally caused claim results in outright cancellation of coverage, and possibly legal action.

👉 Carefully reading the general conditions is essential to avoid unpleasant surprises in case of a claim.

Practical cases / Concrete examples

🧪 Practical cases for better understanding

To make the theory more concrete, here are typical examples illustrating the differences between policies:

🚗 Responsible third-party accident

A driver hits a parking barrier. The “third-party” policy only covers damages caused to others → no coverage for their vehicle.

🔥 Fire with enhanced third-party

A vehicle is set on fire in a parking lot. With the “enhanced third-party” policy, the insurer compensates for loss based on market value at the time of the claim.

🧊 Glass breakage

A crack smaller than a 2-euro coin on the windshield is repaired free of charge at an approved center, with no deductible.

🧍♂️ Driver guarantee

The driver alone injured in a responsible accident will only be compensated if they have purchased the driver guarantee.

💼 Stolen items from the car

A bag left on the seat is stolen. Without a “carried objects” guarantee, no compensation is provided.

👉 These real-world scenarios are particularly useful for BTS Insurance students because they are close to exam practical cases.

How to choose among different auto insurance policies?

As we see, the world of auto insurance is quite complex. Indeed, offers can vary greatly from one insurer to another, which can confuse many drivers. Between third-party, comprehensive coverage, and options, it’s understandable that choosing can be difficult. Fortunately, there is a simple solution for selecting the right insurance for your vehicle.

Insurance comparator, an essential ally for choosing the right policy

When insuring a first vehicle or renewing an existing car insurance contract, it’s wise to consider the various options available. Depending on your situation, different policies or packages may be suitable for you. However, always compare the different proposals before making your decision.

To be effective in your search for the best auto insurance contract, be rigorous. Start by assessing your real insurance needs. If you drive little, it may be more advantageous to subscribe to a specific policy for low mileage, for example. This can help reduce your premium.

Next, use an online insurance comparator—it’s simple and quick. You will see a list of insurers best suited to your request in just a few moments.

Savings at stake

To learn everything about the different auto insurances available on the market, check out a specialized comparison site like Les Furets. This well-known website analyzes proposals from various insurers for you, allowing you to compare offers with equivalent guarantees. This way, you can opt for the cheapest insurance policy with the same coverage as a more expensive competitor.

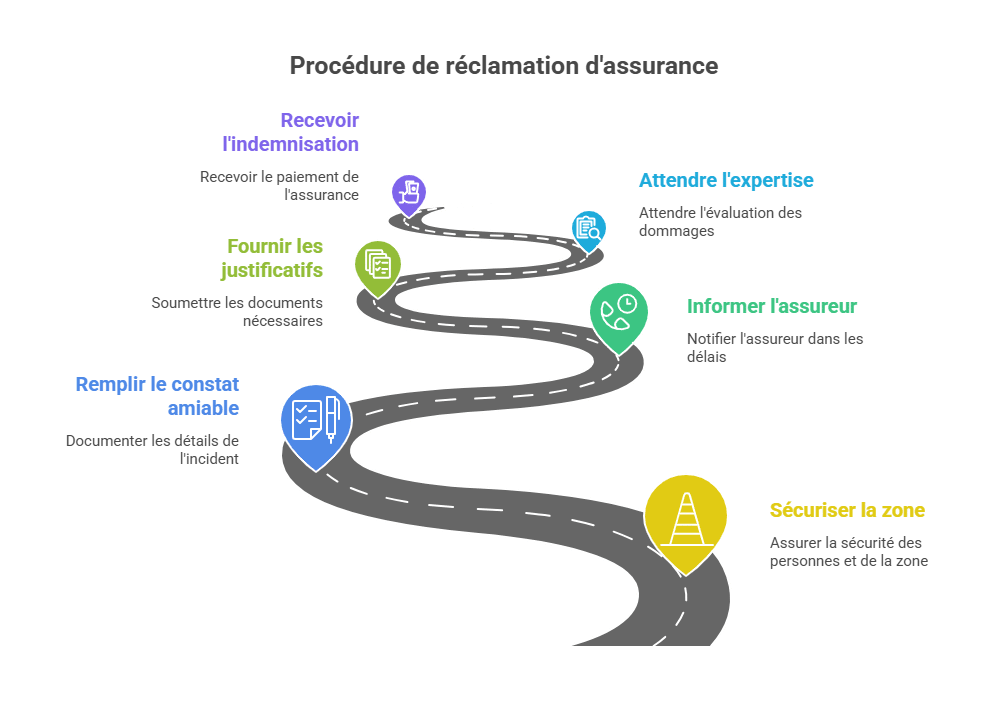

Procedures in case of a claim

📝 Steps to follow in case of an accident

In case of an accident or theft, it is crucial to follow a rigorous procedure so that your indemnification process goes smoothly:

-

🚨 Secure the scene: mark the area, protect people, call emergency services if necessary.

-

📄 Fill out the accident report immediately, accurately, and legibly.

-

📞 Notify the insurer within 5 working days (2 days in case of theft or vandalism).

-

📚 Provide all supporting documents: report, photos, estimates, invoices, police report…

-

🧑🔧 Wait for assessment if necessary (especially in case of major damages).

-

💰 Receive compensation based on the coverage and the market value of the vehicle.

👉 Failing to meet deadlines may lead to a reduction or outright denial of compensation. Acting quickly is always better.

🏁 Conclusion

Auto insurance is more than just a legal obligation: it is a daily security measure. Understanding the differences between policies, knowing what coverages are included or optional, and anticipating how the bonus-malus system works allows you to make informed choices and avoid surprises in case of a claim.

Before signing a contract, take the time to compare offers, assess your real needs, and carefully read the general conditions. Good preparation will help you get optimal coverage while controlling your budget.

👉 To go further, you can consult our other articles or download our revision quiz for testing your auto insurance knowledge.

❓ FAQ about auto insurance

What is the difference between third-party and comprehensive insurance?

→ Third-party insurance only covers damages caused to others, while comprehensive also covers damages to your own vehicle, even when you are at fault.

Is it mandatory to insure a car that is not driven?

→ Yes, every motor land vehicle must be insured at least with third-party coverage, even if parked on private property.

How does the bonus-malus system work?

→ The bonus reduces your premium each responsible year; the malus increases it after responsible accidents.

Which coverages are useful for a young driver?

→ Enhanced third-party policy + driver protection + 0 km breakdown assistance for balanced protection at lower cost.

🚗 Assurance Auto — Articles liés

🔧 Protégez votre véhicule contre les pannes mécaniques

La garantie panne mécanique couvre les réparations imprévues après la garantie constructeur. Obtenez un devis personnalisé en 2 minutes.

Obtenir un devis gratuit →Lien sponsorisé

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.