Understanding the PTZ and Decree No. 2010-912 of August 3, 2010, regarding the attachment to the tax household of parents

In summary

| Section | Summary |

|---|---|

| Fundamental principles of the Zero Interest Loan (PTZ) in 2025 | The PTZ is an interest-free loan aimed at first-time buyers. It complements a traditional bank loan and finances part of the purchase or construction, with caps varying depending on zones and income levels. |

| Impacts of decree n°2010-912 of August 3, 2010, on the tax household attachment of parents | Since 2010, only the applicant’s personal income is considered for PTZ eligibility, even in case of fiscal attachment to parents, to facilitate young people’s access to the scheme. |

| Eligibility conditions for the PTZ for young borrowers attached to the parental tax household | The attachment must appear on the parents’ tax return. The considered income is solely the applicant’s personal income, respecting resource caps, main residence requirement, and supporting documents to be provided. |

| Documents and essential steps to obtain the PTZ with fiscal attachment | Banks require the applicant’s and parents’ tax notices, income simulations, proof of non-ownership, and evidence of fiscal attachment to validate the file. |

| Banks and financing bodies involved in the PTZ: roles and specificities? | The Deposit Office plays a central role, while banks (BNP, Crédit Agricole, Caisse d’Épargne, etc.) grant and manage the PTZ. Action Logement and the ANAH can supplement the financing. |

| Limits, timeframes, and challenges related to obtaining the PTZ under the 2010 decree | Complex procedures, long delays, and disparities among banks. Multiple supporting documents secure the scheme but slow down its acquisition, risking rejection if the application is incomplete. |

| Comparison of the PTZ with other homeownership assistance programs | Beyond the PTZ, there are Action Logement, the Social Access Loan (PAS), and aids from the ANAH. The PTZ is interest-free and combinable, but limited by resource thresholds and fixed amounts. |

| FAQ: Key questions about the PTZ and the decree n°2010-912 regarding the tax household | Simple answers about how the PTZ operates, the impact of the 2010 decree, banks that favor it, necessary supporting documents, and average processing times. |

- The fundamental principles of the Zero Interest Loan (PTZ) in 2025

- Impacts of decree n°2010-912 of August 3, 2010, on the tax household attachment of parents

- Eligibility conditions for the PTZ for young borrowers attached to the parental tax household

- Documents and essential steps to obtain the PTZ with fiscal attachment

- Banks and financing bodies involved in the PTZ: roles and specificities?

- Limits, timeframes, and challenges related to obtaining the PTZ under the 2010 decree

- Comparison of the PTZ with other homeownership assistance programs

- FAQ: Key questions about the PTZ and the decree n°2010-912 regarding the tax household

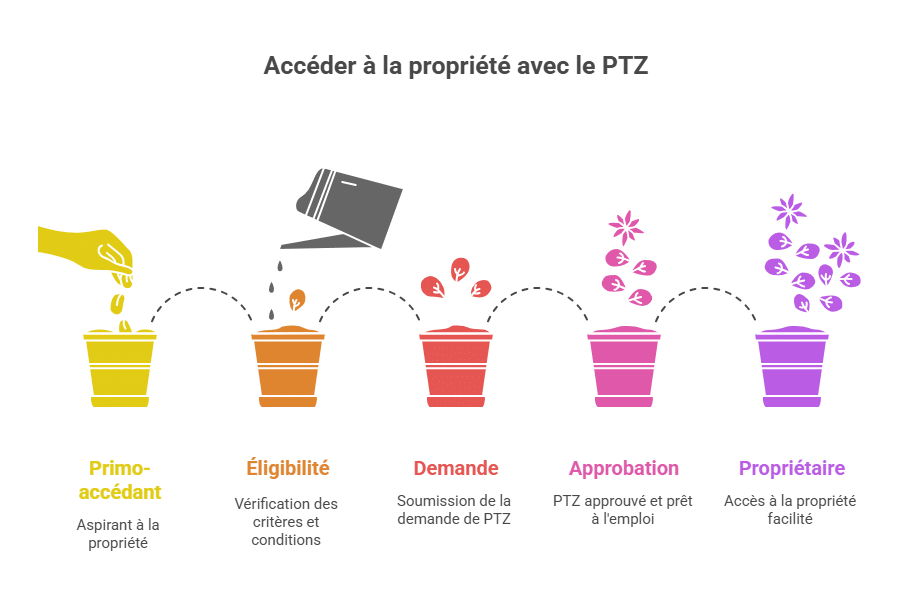

The fundamental principles of the Zero Interest Loan (PTZ) in 2025

The Zero Interest Loan (PTZ) is an essential financial aid to facilitate homeownership, especially aimed at first-time buyers. In 2025, its operation is based on the fact that it is an interest-free loan with no opening fees, issued alongside a traditional bank loan. Its goal is to reduce the financial burden of real estate financing and promote the construction or purchase of a primary residence.

This aid is conditional on several criteria, such as the type of dwelling, geographic location, income levels, and of course, the commitment to occupy the property as a primary residence. The PTZ never finances the entire real estate operation but serves as a supplement to personal savings or other more traditional loans.

In 2025, the PTZ offers several advantages for the borrower:

- No interest: you reimburse only the principal, significantly reducing the total cost of the real estate loan.

- Deferred repayment period: depending on your income, you may benefit from a delay before starting to repay the PTZ, up to several years.

- Adjusted amounts and caps: they vary depending on the geographic zone and household composition.

To effectively access this scheme, it is important to understand how the PTZ is calculated and applied to real estate transactions, which also requires knowledge of the financial and social eligibility conditions. This foundation is crucial before addressing how the decree n°2010-912 of August 3, 2010 modifies certain rules around the fiscal attachment of young borrowers—a key point directly impacting the considered resources.

| Main characteristics of the PTZ | Description |

|---|---|

| Type of loan | Interest-free, no fees |

| Beneficiaries | First-time buyers and some conditions |

| Amount | Covers part of the acquisition or construction |

| Repayment term | Flexible depending on resource conditions |

| Eligible zones | Zones A, B, and C with different caps |

The process to access the PTZ continues to evolve thanks to agreements between banks and organizations like the Deposit Office, which plays a central role in managing and financing this product. It is therefore advisable to compare it with other aids, particularly through Action Logement or the National Agency of Habitat, to optimize your financial arrangement.

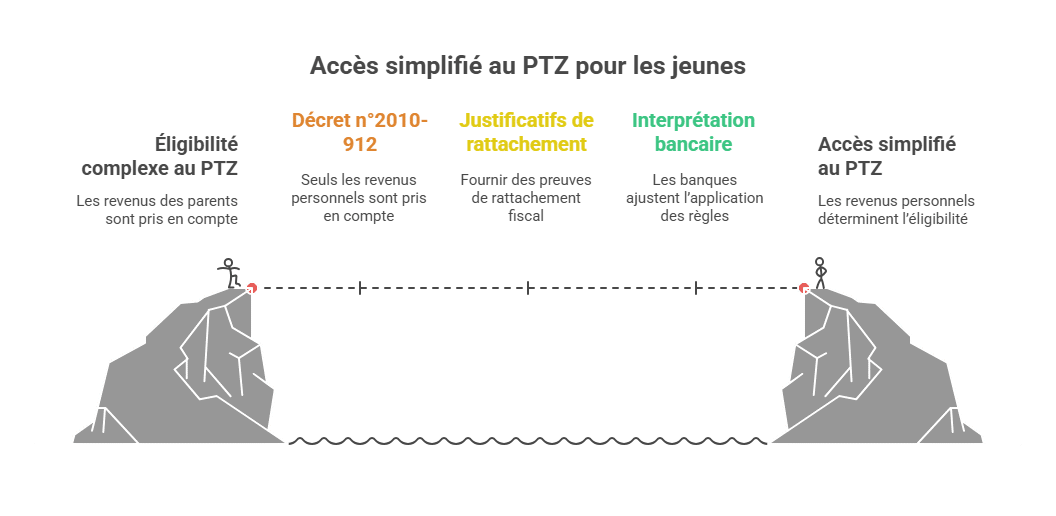

Impacts of decree n°2010-912 of August 3, 2010, on the tax household attachment of parents

Adopted in 2010 and still in force in 2025, decree n°2010-912 of August 3, 2010, profoundly modifies how the tax household attachment to the parental household is considered for PTZ eligibility. This text specifies that, for loans issued since July 1, 2010, only the applicant’s personal resources are to be considered when they are attached to the parental household.

In other words, before this date, some organizations considered the full resources of the parental household when calculating eligibility, which could disadvantage young people still fiscally attached but earning little or no personal income. The decree clarifies this situation by restricting the verification to the individual resources of the applicant, provided they are fiscally attached to the parent.

This reform aims to facilitate young people’s access to the PTZ who do not yet declare their own household, such as students or young employees beginning their professional lives. However, it introduces additional constraints regarding supporting documents to prove this attachment and sometimes complicates the reading of fiscal documents.

As highlighted by several banking actors in 2025, including BNP Paribas and Crédit Agricole, interpreting the rules related to this decree required an adjustment. Some banks, such as Caisse d’Épargne or La Banque Postale, remain cautious on certain files, reflecting difficulties in standardizing application.

It is important to understand that this decree directly influences the calculation of the resource caps for the PTZ. For example, a young person fiscally attached to parents will have only their personal income considered, unlike in a situation where they declare their own household. This can make the difference in meeting eligibility thresholds.

| Entry into force date | Main effect | Practical consequence |

|---|---|---|

| July 1, 2010 | Only the personal income of fiscally attached applicants is considered | Better adaptation of eligibility to the young borrowers’ situations |

| Since 2010 | Necessity to produce specific proof of attachment | More complex administrative procedures but secure the scheme |

This topic is widely discussed on specialized forums and expert sites such as MoneyVox and CommentCaMarche.fr, where users share their experiences. To learn more about the precise procedures, consulting official resources—including this particular exchange on MoneyVox—is a good starting point.

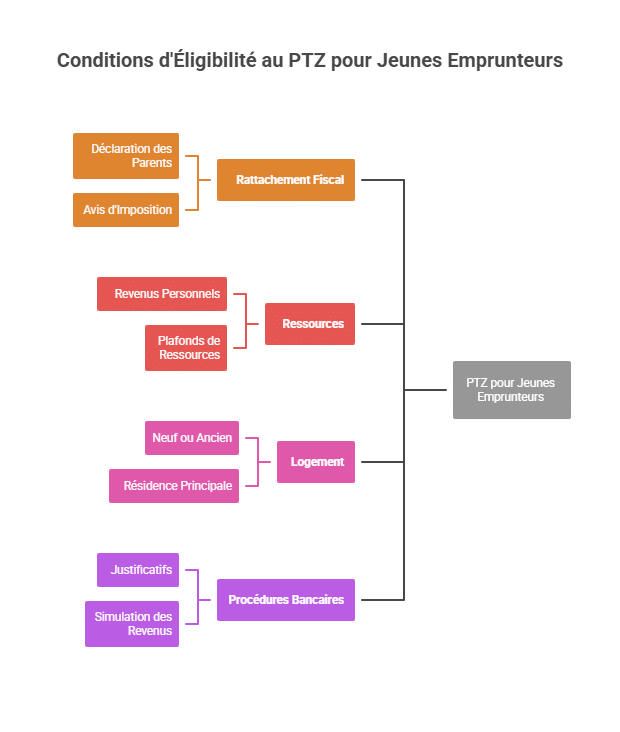

Eligibility conditions for the PTZ for young borrowers attached to the parental household

The attachment to the parental household involves specific conditions for accessing the PTZ. For a young borrower who has not yet established their own household, eligibility mainly depends on:

- Confirmation of fiscal attachment via the parents’ income tax declaration showing the young person.

- Resources considered: only their actual personal income, not aggregated with the parental household incomes.

- Respect for resource caps: specific to the PTZ, which vary depending on household composition and property location.

- Nature of the property: new or old with eligible renovations.

- Commitment to occupy the property as a principal residence within a given timeframe.

Special attention must be paid to the supporting documents requested by banks, notably:

- The last personal tax notices

- The fiscal declarations of the parents mentioning the attachment

- Declarations of non-property made within the last two years

- Income simulations from official platforms

These criteria may seem demanding, but their goal is to make the process fairer and more precise, while limiting fraud. Each bank applies its internal rules based on these guidelines, which explains different practices.

For example, BNP Paribas and Crédit Agricole have adapted their procedures to secure and better integrate these criteria, as evidenced by internal documentation circulated in branches. This approach differentiates their position from that of Caisse d’Épargne, which is more cautious about granting PTZ under these conditions, showing that the choice of bank can influence the success of the application.

| Criterion | Specific requirement for attachment |

|---|---|

| Fiscal attachment | Appearance on the parents’ declaration explicitly indicating the attachment of the young person |

| Resources | Only personal income, verified for the current fiscal year |

| Property | New or old with renovations on the primary residence |

| Bank procedures | Documented application with supporting evidence (tax notices, non-property attestations, etc.) |

To better understand these conditions, it is recommended to consult a comprehensive guide like the one offered by Comment Ca Marche, which details all current rules as well as possible negotiation margins with banks.

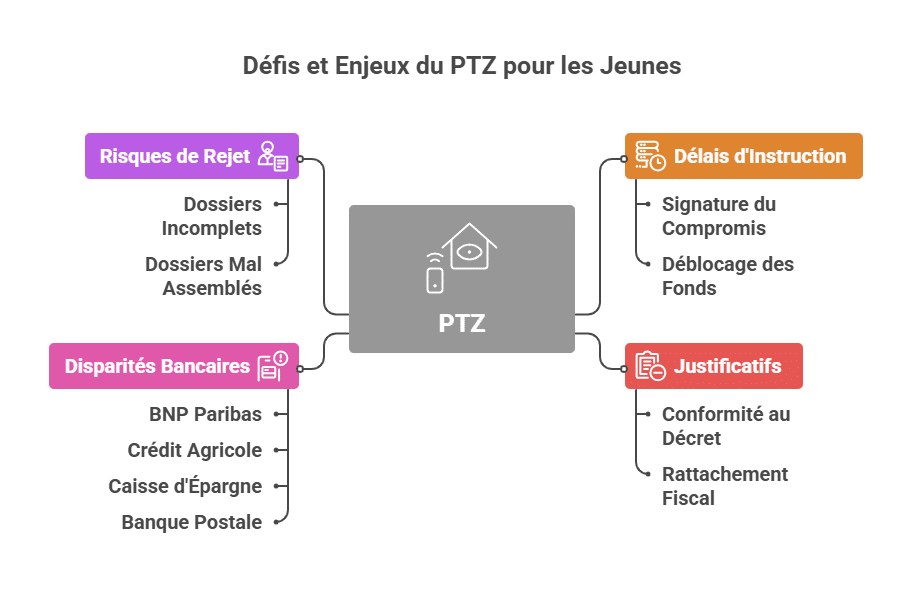

Documents and essential steps to obtain the PTZ with fiscal attachment

Obtaining the PTZ, especially when there is a fiscal attachment to the parental household, requires thorough preparation of administrative documents. Banks and financing organizations require a series of specific documents to validate the application:

- The last two personal tax notices, to verify personal income.

- The last two tax notices and declarations of the parents where the fiscal attachment of the candidate is clearly indicated.

- A simulation of the income of the young borrower for the last two years, extracted from official tax sites, often requested to anticipate financial solidity.

- Proof of non-ownership from the last two years, such as rent receipts or signed attestation if the young person lived with their parents, and sometimes a cadastral extract to certify the parents’ property.

A real case in 2025 illustrates the difficulties and patience required: a borrower took four and a half months between signing the sales agreement and receiving the PTZ funds, after convincing several banks like BNP Paribas and Crédit Agricole through internal documents and clarifications provided by the broker CAFPI.

It should be noted that some banks, such as Caisse d’Épargne and La Banque Postale, remain more cautious and often require additional explanations or documents. The extreme prudence of institutions emphasizes the importance of a perfectly compliant and prepared file in advance.

| Document | Importance | Source or origin |

|---|---|---|

| Parents’ tax notice | Attests to fiscal attachment | Tax office or official website |

| Income simulation | Anticipates repayment ability | Tax site (impots.gouv.fr) |

| Proof of non-property | Shows absence of recent real estate assets | Rent receipt, sworn statement, cadastral extract |

| Personal tax notice | Used to evaluate personal income | Tax office |

For more practical advice on properly structuring your application, reading dedicated resources on sites like MoneyVox or Service-Public.fr is recommended.

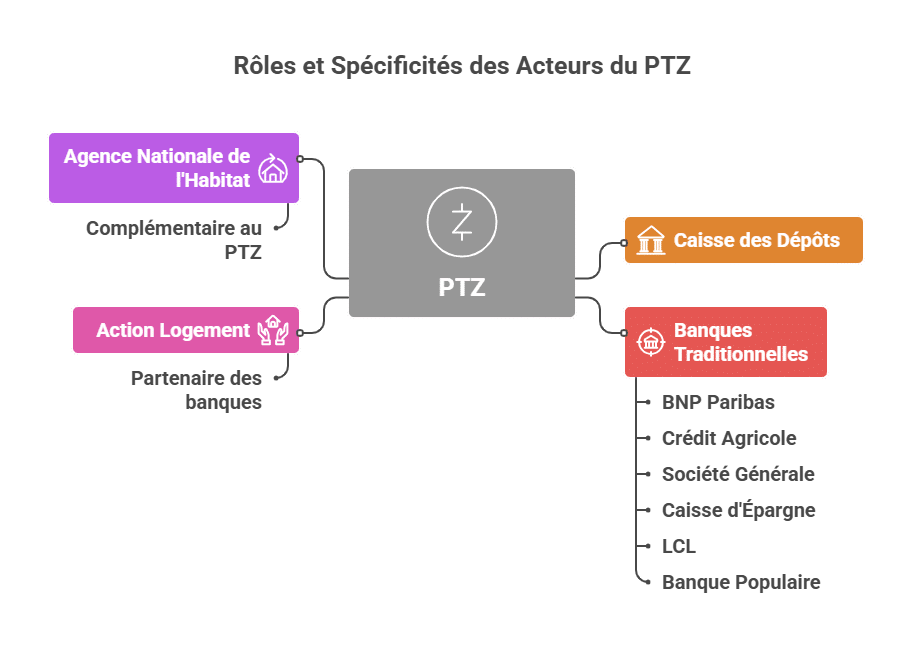

Banks and financing organizations involved in the PTZ: roles and specificities?

The PTZ is not distributed by a single entity but through a network of banks and public or semi-public organizations, each with its own specificities and conditions. Understanding the role of each will help you make the best choice when preparing your file in 2025.

- The Deposit Office: a key player in funding, guaranteeing and co-financing a large part of PTZs, coordinating the scheme nationwide.

- Traditional banks: BNP Paribas, Crédit Agricole, Société Générale, LCL, Banque Populaire, and Caisse d’Épargne. They analyze files, grant the main loan and the PTZ, and oversee repayment.

- Action Logement: a partner in some cases, offering gateways to other complementary assistance for homeownership.

- National Housing Agency (ANAH): although mainly focused on grants for renovation and energy efficiency improvements, it sometimes complements the financial setup with the PTZ.

Some banks are more receptive to files presenting a young applicant’s fiscal attachment, notably BNP Paribas and Crédit Agricole, which have internal procedures adapted to facilitate access.

Each establishment applies its own timing and internal criteria, which can raise questions for borrowers. For example, Caisse d’Épargne and La Banque Postale are often more cautious and have longer processing times. This point is crucial to consider, especially now when demand for PTZs is high at year-end.

| Bank / Organization | Role in the PTZ | Notable specificities |

|---|---|---|

| BNP Paribas | Grants the PTZ and main loan | Flexible internal procedures for fiscal attachment |

| Crédit Agricole | Funding and advice | Internal documentation to secure young applicants’ files |

| Société Générale | Grants PTZ according to standard criteria | Less frequent in cases with fiscal attachment |

| Caisse d’Épargne | Slow and cautious distribution | More demanding on supporting documents |

| LCL | Access to standard PTZ | Intermediate processing time |

| Banque Populaire | Loan granted after detailed analysis | Personalized follow-up but strict requirements |

| Action Logement | Additional aid and accessory loans | Partner of banks |

| National Housing Agency | Support for renovation | Complementary to PTZ |

To better choose, it is advisable to evaluate each criterion precisely with the help of a specialized broker. Cafpi, for example, regularly produces specific documents and studies to guide borrowers in assembling their files, especially given the adaptations related to the decree of August 3, 2010.

Limits, timeframes, and challenges related to obtaining the PTZ under the 2010 decree

Although the PTZ is a powerful lever to facilitate homeownership, particularly for young people fiscally attached to their parents, some constraints remain, especially regarding the implementation of decree n°2010-912.

Banks often hesitate to grant the PTZ when the applicant is attached to the parental household. This caution leads to:

- Longer processing times: sometimes several months between signing the agreement and disbursing funds;

- Increased documentation requirements: more administrative complexity;

- Risks of misunderstanding: errors in assessing the income taken into account;

- Disparities among banks: some are more flexible (BNP Paribas, Crédit Agricole), others more cautious (Caisse d’Épargne, La Banque Postale).

This situation sometimes forces borrowers to be patient and persistent. For example, a file processed at the end of 2024 required multiple exchanges with the broker and the submission of authentic copies to the tax office.

The stakes are twofold: on the one hand, ensuring the correct application of the scheme to target aid to those genuinely in need; on the other hand, avoiding fraud or misuse through increased administrative rigor. Candidates must adopt a patient and methodical approach.

| Challenges | Explanations |

|---|---|

| Long delays | Complex procedures slow fund release |

| Multiple supporting documents | Ensures compliance with the fiscal attachment decree |

| Bank disparities | Lack of uniformity in file processing |

| Rejection risks | Incomplete or poorly assembled files against requirements |

To better anticipate this framework, it can be helpful to consult active discussions on specialized forums, such as via this link Comment Ca Marche, which provides details on timelines and procedures to follow, as well as a review of current legislation.

Comparison of the PTZ with other homeownership aid schemes

Within the landscape of aid programs for homeownership, the PTZ is often the main pillar, but other schemes can be combined or sometimes replace the PTZ partly depending on profiles:

- Action Logement: offers assisted loans to fund the personal contribution or related renovation works;

- Social Access Loan (PAS): reserved for certain households under income conditions;

- Local aids: grants or low-interest loans from local authorities;

- National program of the National Housing Agency: mainly targeted at renovation and energy improvement assistance.

The PTZ can be combined with these aids under certain conditions. Its particularity lies in its interest-free nature, which provides a real benefit over the total duration of the loan.

Compared to other banking products, the PTZ often offers better conditions for first-time buyers but must be evaluated case by case, particularly through a careful study of the borrower’s profile and project.

| Dispositif | Objectif | Advantages | Limits |

|---|---|---|---|

| Prêt à Taux Zéro (PTZ) | Ease of purchasing a primary residence | Interest-free, combinable | Resource caps, limited amounts |

| Action Logement | Personal contribution and renovation | Direct aid, supplementary loans | Employment-related conditions |

| Social Access Loan (PAS) | Support for modest households | Lower interest rates, social guarantees | Resource restrictions |

| ANAH | Renovation and energy improvement | Significant grants | Not for new builds |

To deepen understanding of these schemes, exploring detailed analyses such as those shared on Aide BTS Assurance is helpful, where various SWOT studies highlight their strengths and weaknesses in real estate matters.

FAQ: Key questions about the PTZ and decree n°2010-912 concerning the tax household

R1: The PTZ is a loan without interest intended to facilitate the purchase of a new or old home under conditions, repayable with deferred payments depending on the situation.

R2: It ensures that only the applicant’s personal income, even if attached to the parental tax household, is considered, not the parents’ income.

R3: BNP Paribas and Crédit Agricole stand out due to their adapted procedures and better handling of such files.

R4: It is necessary to provide the parents’ tax notices, the declaration indicating attachment, the applicant’s personal tax notices, and proof of non-property.

R5: The duration can vary significantly, often several months, depending on the bank, the quality of the file, and the time of year.

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.