The loss ratio measures the relationship between claims paid and premiums collected, evaluating the profitability of contracts.

💡 Importance

It allows for assessing financial viability and adjusting premiums to cover risks.

📈 Risk Management

A strategic tool to analyze trends and adopt corrective measures.

👥 Impact on policyholders

High loss ratios can lead to premium increases and restrictions in coverage.

🔢 Example of calculation

Divide claims paid by premiums collected, then multiply by 100.

🔍 Monitoring

Regular monitoring of the rate helps anticipate risks and adjust policies.

⚠️ Consequences of a high ratio

Premium hikes, reduction in coverage, and loss of trust.

✅ Advantages of a low rate

Stable premiums, efficient risk management, and an improved reputation.

⚙️ Influential factors

Frequency and severity of claims, geographic area, and type of insurance.

🛡️ Prevention

Identify risks, raise policyholders’ awareness, and adopt modern management tools.

🚀 Technological innovations

Use of AI, big data, and automation to predict and manage risks.

🤝 Ethics

Protect vulnerable policyholders and strengthen transparency in contract management.

📜 Conclusion

The loss ratio is essential for balancing risks, adjusting premiums, and maintaining a balanced relationship between insurers and policyholders.

The loss ratio is a central concept in the insurance field. It allows evaluating contract profitability by comparing indemnities paid by the insurer to premiums collected. This indicator has strategic importance for insurance companies, which must adjust their offers, as well as for policyholders, whose premiums may change based on this rate. In this article, we will explore the definition of the loss ratio, the factors influencing it, the consequences of a high rate, and solutions for effective management.

What is the loss ratio in insurance?

The loss ratio is an essential tool to measure the financial performance of insurance companies. It is an indicator that compares the amounts paid by the insurer to cover claims and the premiums collected from policyholders. In other words, it determines whether the revenues from premiums are sufficient to cover the costs of claims.

Why is it important?

This indicator is fundamental for two main reasons. First, it provides a clear view of contract profitability. A high loss ratio, close to or exceeding 100%, means that the insurer spends as much, or more, than it earns, jeopardizing the economic viability of its activity. Second, the loss ratio is used to adjust premiums, ensuring that the risks undertaken are properly evaluated and covered.

A risk management indicator

The loss ratio is not just a measure of profitability. It is also a forecasting and risk management tool. Insurers use it to analyze trends in various segments, like health, auto, or home insurance. This helps them identify sectors with higher risks and adopt corrective measures, such as revising coverage, adding deductibles, or adjusting contractual conditions.

An impact on policyholders

For policyholders, this rate can directly influence the amount of their premiums. When claims increase in a specific category, insurers are forced to compensate for losses by raising tariffs. For example, an increase in claims related to natural disasters can lead to higher premiums in affected regions.

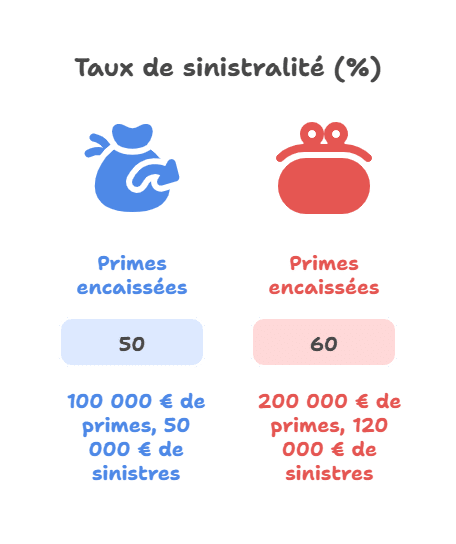

Example of calculating the loss rate

Premiums collected (€)

Claims paid (€)

Loss ratio (%)

100,000

50,000

50

200,000

120,000

60

To calculate this rate, simply divide the claims paid by the premiums collected, then multiply the result by 100.

Why monitor the loss ratio?

Monitoring the loss ratio is essential for both insurers and policyholders. This indicator plays a strategic role in financial risk management and policy adjustment.

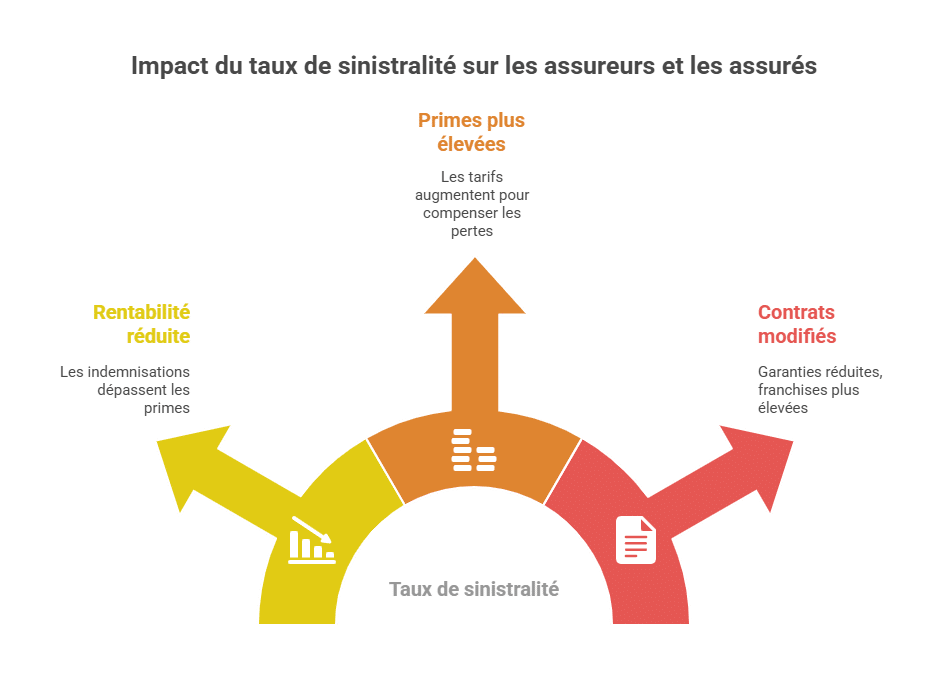

Consequences of a high loss ratio

Compromised profitability for the insurer

A high loss ratio means that the insurer spends a significant, or even all, of the premiums collected to pay claims. This can lead to financial losses and threaten the economic viability of the company.

Example: A ratio above 100% reflects a situation where indemnities exceed premiums, endangering the insurer’s financial stability.

Premium increases for policyholders

To offset losses, insurers must adjust their rates upward, directly impacting policyholders’ budgets. These increases can make certain insurance contracts less accessible, especially in high-risk sectors or regions.

Contract modifications

Insurers may reduce coverage, increase deductibles, or introduce more restrictive clauses to limit their risk exposure.

Advantages of a low loss ratio

Effective risk management

A low loss ratio demonstrates good control of insured risks and increased profitability. It enables insurers to offer competitive contracts while maintaining stability.

Premium stability

Policyholders benefit from constant or even reduced rates, enhancing their satisfaction and loyalty.

Enhanced reputation

A low loss ratio improves the insurer’s image as an entity capable of effectively managing claims while preserving resources.

Why is this monitoring strategic?

Regular monitoring of the loss ratio allows to:

Identify trends by sector, geographic area, or coverage type.

Make informed decisions to adjust premiums and coverage options.

Prevent high claims situations by implementing prevention policies and raising awareness among policyholders.

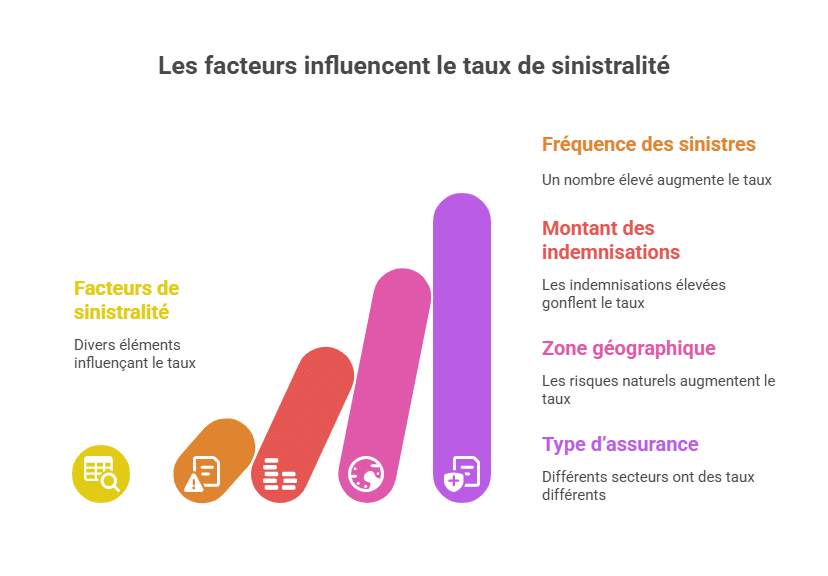

Factors influencing the loss ratio

The loss ratio is affected by several factors that vary depending on the type of insurance, the region, or risk management practices. These elements play a critical role in increasing or decreasing this indicator.

Factors

Potential Impact

Frequency of claims

High frequency increases the rate.

Amount of indemnities

High indemnities also inflate the rate.

Geographic area

Some regions present higher natural risks.

Type of insurance

Each sector has different claims levels.

Detailed analysis of the factors

Frequency of claims The higher the number of reported claims, the higher the loss ratio. For example, in densely populated areas, road accidents or claims related to natural disasters are more frequent, increasing costs for insurers.

Amount of indemnities The severity of claims directly influences claim payouts. Costly claims, such as serious bodily injuries or major damages from floods, greatly raise the rate.

Geographic area Certain geographic zones are more exposed to specific risks, such as natural disasters (floods, earthquakes, storms). Insurers must account for these risks to adjust premiums and prevent high claims.

Type of insurance Each insurance sector has distinct characteristics. For example:

Health insurance generally has a high claims rate due to significant medical costs.

Automobile insurance may have a moderate rate but remains influenced by accident frequency.

Home insurance is affected by claims related to natural disasters or water damage.

Importance of proactive management

These factors show that proactive risk management is essential to control the loss rate. Insurance companies can implement preventive measures such as:

Raising awareness among policyholders about specific risks.

Adjusting contracts to include clauses suitable for high-risk zones or sectors.

Using modern technologies to anticipate claims trends.

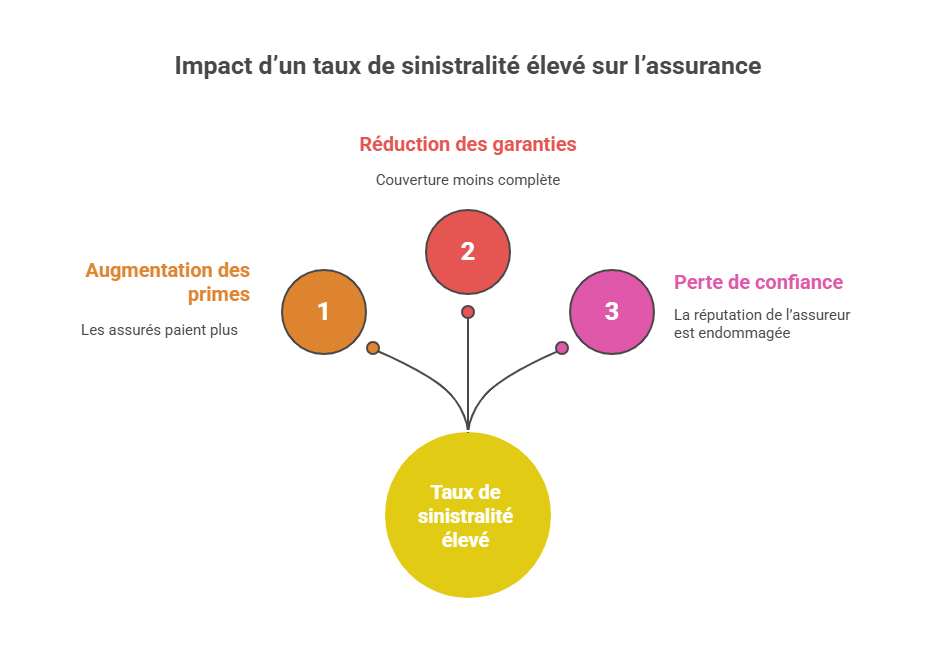

Consequences of a high claims ratio

A high claims ratio can have significant repercussions for both insurers and policyholders. Here are the main consequences to consider:

Premium increases

A high claims ratio forces insurers to rebalance their finances by raising insurance premiums.

Policyholders must pay higher premiums, which can directly impact their budget.

These rate hikes can make certain insurance policies less accessible, especially in high-risk sectors or regions.

Reduction in coverage

To limit financial losses, insurance companies adjust contract terms.

Coverage can be reduced, making protection less comprehensive.

Insurers may also introduce higher deductibles, shifting part of the risk onto policyholders.

This forces policyholders to bear a greater share of costs, especially in cases of recurrent claims.

Loss of trust

Excessive claims can harm the insurer’s reputation.

Customers perceive higher premiums and reduced coverage as a sign of poor risk management.

This situation can also affect the business relationships of insured companies, as high claims are often seen as an increased risk signal.

This can lead to a loss of credibility and complicate access to new policies or contract renewals.

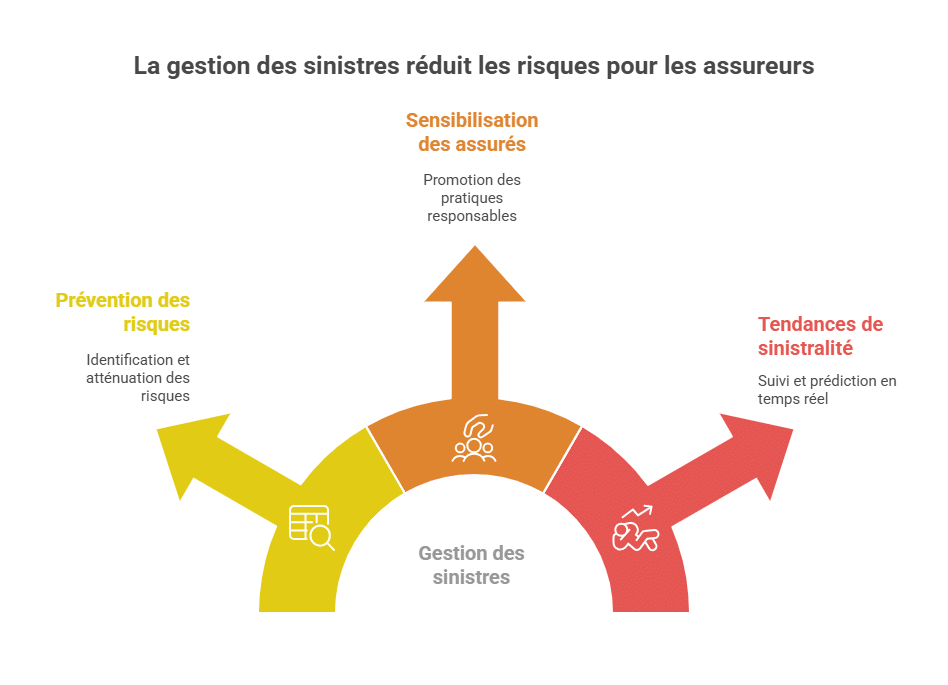

How to control the loss ratio?

Managing the loss ratio relies on a combination of preventive strategies and proactive management. These actions help limit risks and ensure better profitability for insurance companies while providing optimal conditions for policyholders.

Claim prevention

Identify major risks

A detailed analysis of past claims and current trends helps detect high-risk zones or sectors. This identification aids in predicting and preventing future claims.

Educate policyholders on best practices

Training policyholders on preventive measures and responsible behaviors reduces the frequency and impact of claims. For example, in the auto sector, awareness campaigns on road safety can help reduce accidents.

Modern management tools

Current technologies offer effective solutions for monitoring and predicting claims trends.

Real-time monitoring: Analytical software allows continuous surveillance of claims and detection of significant deviations.

Data-driven predictions: Using artificial intelligence and big data helps identify emerging risk factors and adjust policies accordingly.

Automation of processes: Rapid claims management and immediate corrective measures minimize losses.

Sector-specific examples

Sector

Average claims rate

Health insurance

85%

Car insurance

70%

Home insurance

65%

These figures show that each sector has unique characteristics influencing its claims rate.

Health insurance: High medical costs and prolonged treatments increase claims.

Car insurance: Accident frequency depends heavily on driving behavior and road conditions.

Home insurance: Claims are often related to natural disasters or water damage.

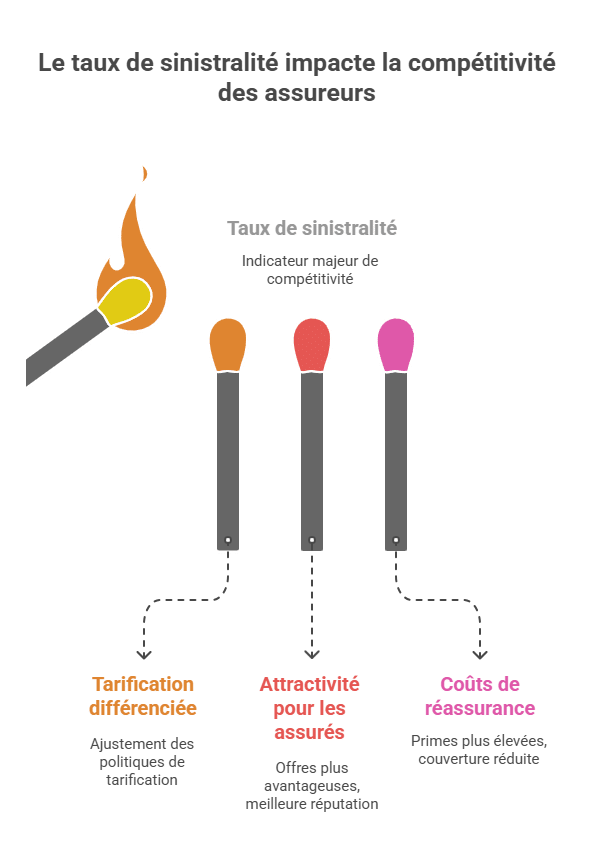

Strategic issues related to the loss ratio

Direct influence on competitiveness

The loss ratio is a key indicator for assessing the competitiveness of an insurance company in a constantly evolving market. Insurers able to maintain a low rate can offer competitive deals, attracting more customers.

Differentiated pricing: Based on observed loss levels, companies adjust their pricing policies. For instance, a low-risk area may benefit from reduced premiums, while high-risk sectors will see their premiums increased. This ensures that premiums reflect the actual risk level, optimizing profitability.

Appeal to policyholders: When insurers control their loss ratio, they can propose more attractive contracts, strengthening customer loyalty and attracting new policyholders. This control demonstrates effective risk management and enhances the reputation of the insurer in the market.

Impact on reinsurance policies

Insurers use reinsurance as a tool to transfer part of their financial risks to other companies. However, a high loss ratio directly impacts this process:

Increased costs: The higher the claims ratio, the more reinsurance companies demand higher premiums to cover risks, reducing insurers’ profit margins.

Reduced coverage: In case of excessive claims, reinsurers may limit guarantee levels, exposing insurance companies to potentially larger losses. This forces insurers to review their strategies and adopt proactive measures to reduce risks.

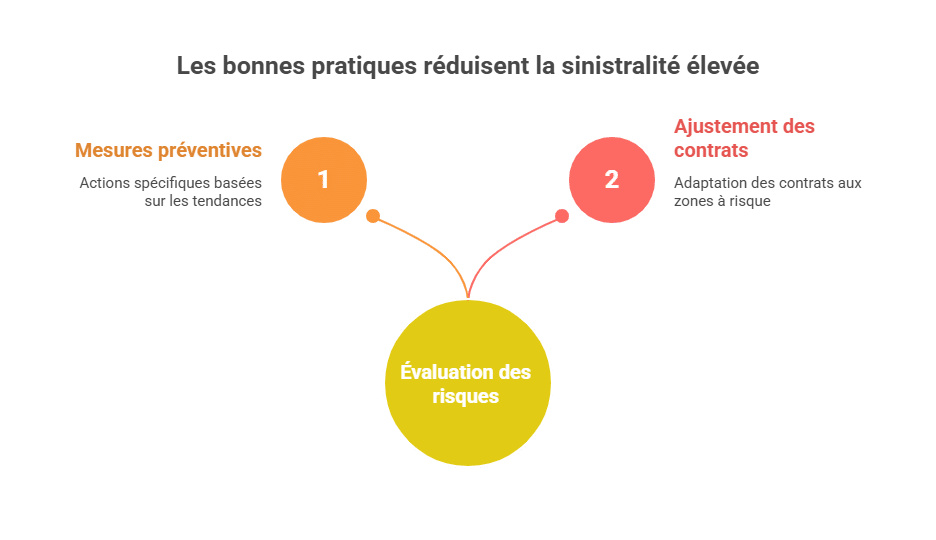

Best practices to prevent a high claims ratio

Continuous risk assessment

To prevent an increase in claims ratio, insurance companies must engage in regular risk evaluation.

Analysis of historical data: Insurers need to examine past claims to identify recurring trends. For example, an increase in road accidents during winter may signal a need for specific preventive measures for that period.

Mapping sensitive zones: Some regions have higher natural risks, such as floods or earthquakes. Mapping high-risk zones helps companies anticipate periods of high claims and adjust policies accordingly.

Training and policyholder education

Raising awareness among policyholders plays a key role in reducing claims.

Prevention workshops: Companies can organize sessions to inform clients about simple steps that reduce risks, such as maintaining electrical equipment or practicing safe driving.

Encouraging safety: Offering reduced premiums for policyholders using safety devices, like smoke detectors or alarms, encourages responsible behaviors.

Collaboration among actors

Effective claims management relies on close cooperation among different players in the insurance ecosystem.

Insurers and regulators: Regulators can impose guidelines to ensure appropriate pricing and fair coverage, even in high-risk zones.

Brokers and policyholders: Brokers play an important role in raising awareness among policyholders, explaining claims issues, and helping select appropriate coverage.

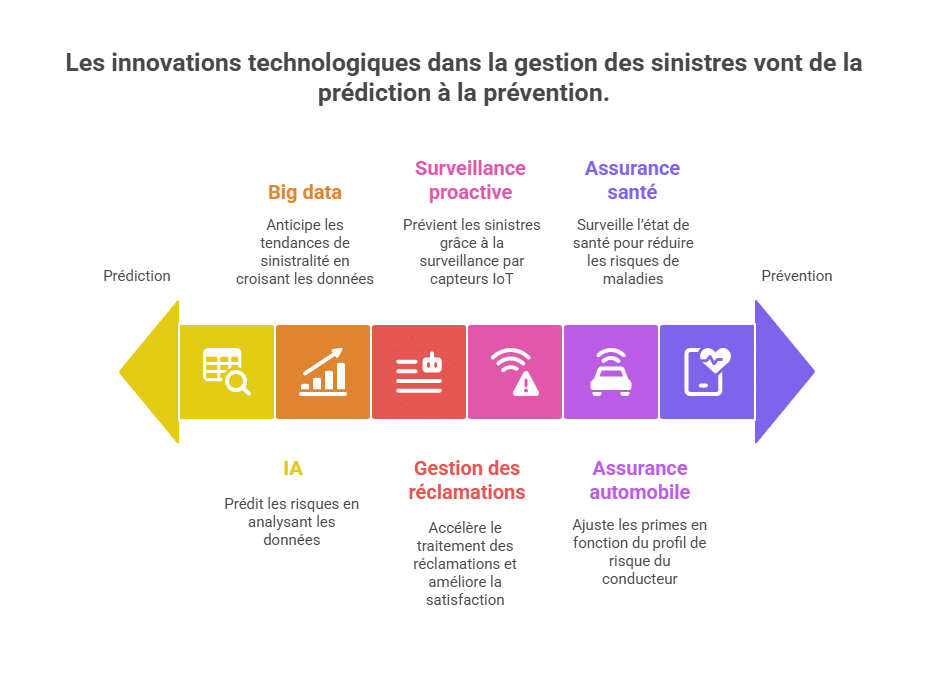

Technological innovations for claims management

Predictive tools

Modern technologies, such as artificial intelligence (AI) and big data, are transforming claims management.

AI to predict risks: Machine learning algorithms analyze millions of data points to identify risk factors before they become problems. For instance, a system can forecast an increase in road accidents under specific weather conditions.

Big data analysis: Combining demographic, environmental, and historical data enables companies to anticipate claims trends, allowing them to adjust premiums or propose preventive actions.

Process automation

Automation makes claims management faster and more efficient.

Claims handling: Automated systems can process claims within a few hours, reducing indemnification delays and improving customer satisfaction.

Proactive monitoring: Using Internet of Things (IoT) devices, companies can install sensors to prevent claims. For example, water detectors can alert property owners and insurers of a leak before it causes major damage.

Concrete examples of innovation

Auto insurance: Connected devices, or “telematics”, measure driving behavior (speed, braking, etc.) to adjust premiums based on risk profile.

Health insurance: Monitoring apps enable policyholders to track their health status, reducing the risk of serious illnesses through early detection.

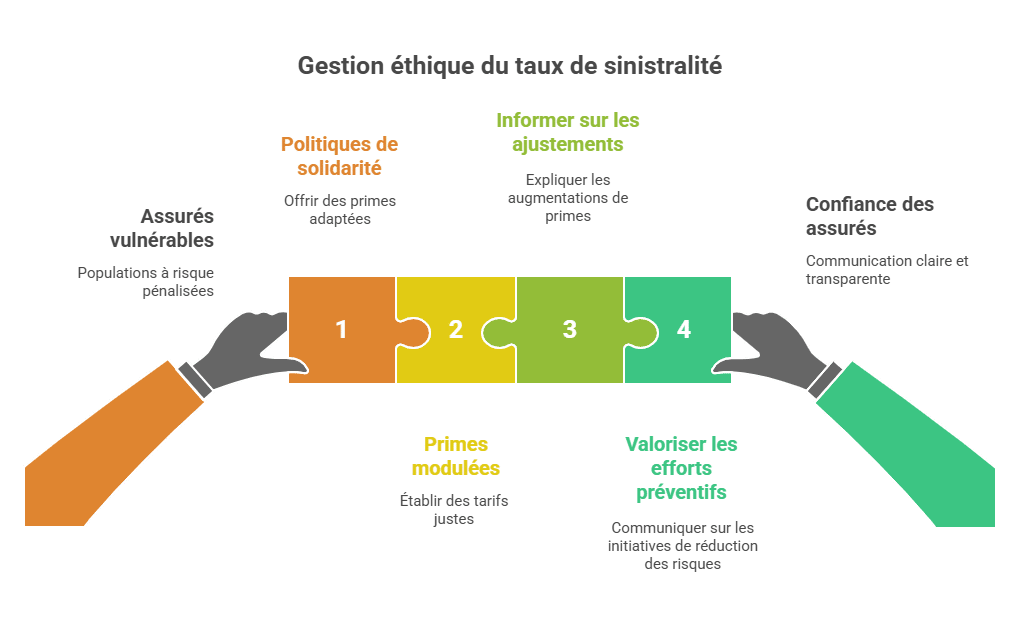

Ethical management of the loss ratio

Protecting vulnerable policyholders

Insurance companies must ensure they protect at-risk populations without unfairly penalizing them.

Solidarity policies: Offering adjusted premiums for areas prone to natural disasters without overburdening policyholders financially.

Modulated premiums: Establishing fair rates for policyholders with a high claims history, while promoting preventive solutions.

Transparency and communication

Clear communication about loss ratio management enhances policyholder trust.

Inform about adjustments: Explaining why some premiums increase, highlighting specific claims data relevant to a sector or region.

Value preventive efforts: Communicating initiatives taken by insurers to reduce risks, such as prevention campaigns or technological partnerships.

Conclusion

The loss ratio is an essential indicator for insurers and policyholders. It allows assessing profitability, adjusting contracts, and preventing risks. Proactive management, modern tools, and effective awareness are key to controlling this indicator and maintaining a balanced relationship between insurers and policyholders.

BTS Insurance Graduate Founder aidebtsassurance.com Active since 2019

BTS Insurance graduate, I have been helping students prepare for and pass their exams since 2019. This site brings together all my courses, study guides and tools.

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.