In summary

| Type of deductible | Explanations and examples |

|---|---|

| Relative (or simple) deductible | The insured is compensated only if the loss exceeds the amount of the deductible. Example: deductible €150 → loss €100 → no reimbursement; loss €200 → full reimbursement. Present in legal protection contracts. |

| Absolute deductible | The deductible is always deducted, regardless of the amount of the claim. Example: €150 deductible → €100 loss → no reimbursement; €200 loss → €50 reimbursement. Common in auto and home insurance. |

| Proportional deductible | The deductible varies based on a percentage of the damage, with a minimum and maximum. Example: 10% of the loss with a minimum of €250 and a maximum of €450. If loss €2,600 → deductible €260; if loss €2,200 → deductible €250; if loss €5,600 → deductible €450. |

| Fixed deductible | Amount always identical, defined in the contract, regardless of the loss. Example: fixed €150 deductible → systematically deducted. Helps reduce the premium but increases the out-of-pocket share. |

| Variable deductible | Amount that adapts to the cost of the damage (often in %). Example: 10% deductible on a €1,000 loss → €100 remaining to pay. More fair on small claims but can be costly on large damages. |

| Minimum and maximum deductible | Framework for the proportional deductible. Example: minimum €50, maximum €500 → you will never pay less than the minimum nor more than the maximum, regardless of the claim value. |

In insurance, the concept of deductible plays a crucial role since it determines the portion of expenses remaining at the insured’s charge in case of a claim. Too often overlooked, it directly influences the amount of compensation as well as the insurance premium cost. Several forms of deductibles exist, each with its own specifics, advantages, and disadvantages. To better understand these differences and make an informed choice when subscribing to a contract, here is a summary table of the main types of insurance deductibles.

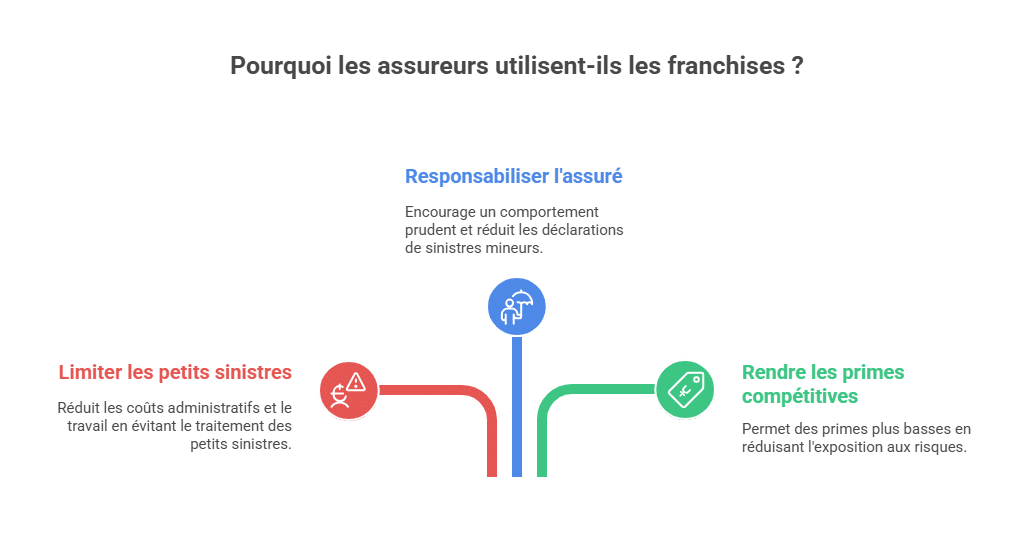

🎯 Why do insurers use deductibles?

The presence of a deductible in an insurance contract is not insignificant. It serves several key objectives for insurance companies:

-

Limit management of small claims : handling damage of a few tens of euros often costs more in administrative fees than the actual refund amount. The deductible prevents this workload overload and reduces internal costs.

-

Make the insured responsible : by leaving part of the damage to the client’s charge, the insurer encourages cautious behavior and discourages minor claim filings.

-

Make premiums more competitive : thanks to deductibles, insurers reduce their exposure to frequent risks and can offer more attractive contributions. This helps balance the cost paid by the insured and the level of coverage offered.

Relative deductible (or simple deductible)

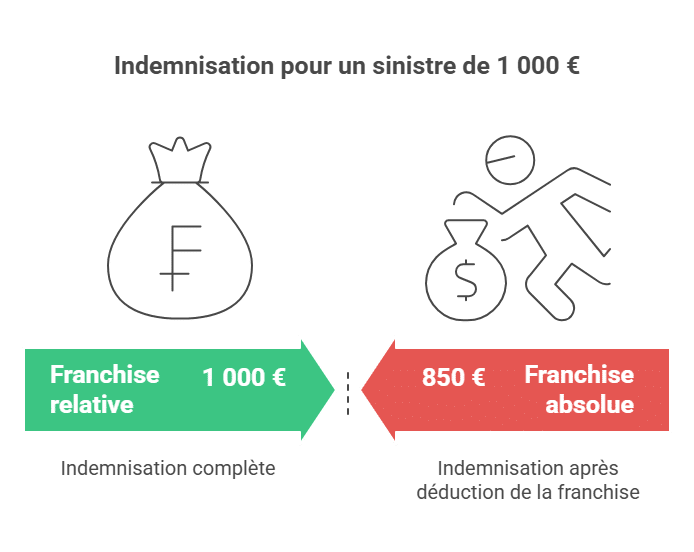

The relative deductible, sometimes called simple deductible, is an insurance mechanism based on a clear principle: you are only compensated if the amount of the claim exceeds the deductible specified in the contract. Otherwise, you receive nothing from your insurer.

Specifically, this deductible acts as a trigger threshold. It does not operate proportionally or deductibly but in a “all or nothing” manner.

👉 Detailed example :

-

If your contract provides a relative deductible of €150 and your claim is evaluated at €120, you will receive no compensation from the insurer.

-

If your claim amounts to exactly €150, the deductible still applies, and you will not be reimbursed.

-

Conversely, if your claim reaches €200, the insurer will cover the full amount, without deducting the deductible.

To remember :

-

The relative deductible blocks reimbursement below or at the level of the deductible, but disappears entirely once the damage exceeds it.

-

Unlike the absolute deductible, it does not reduce compensation for claims greater than the deductible: you then receive the full damage amount.

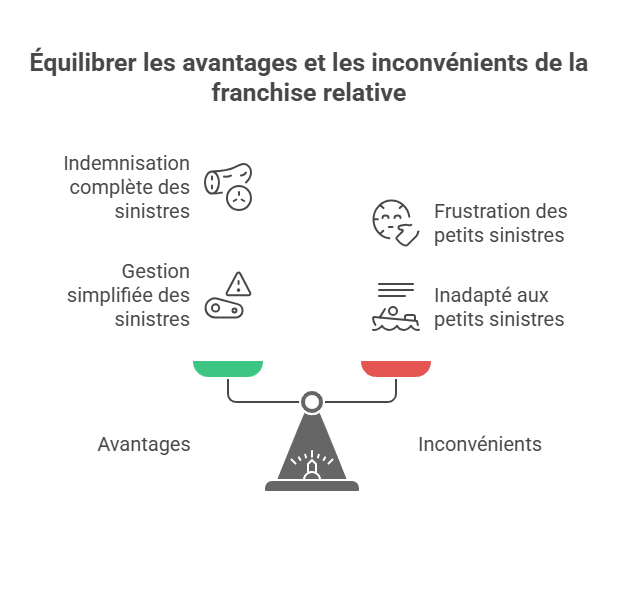

✅ Advantages of the relative deductible

-

The insured is fully compensated if the damage exceeds the deductible.

-

Allows filtering small claims, preventing insurers from handling minor cases.

-

Favors a win-win relation: the insured doesn’t lose anything on large claims, and the insurer limits management costs on minor ones.

❌ Disadvantages of the relative deductible

-

Can be perceived as frustrating for insureds if claims are frequent but low in amount.

-

Not suitable for contracts covering common and inexpensive damages, as the insured may feel like “paying for nothing”.

📌 Application areas

The relative deductible is usually found in legal protection contracts, where it helps avoid managing small disputes, while guaranteeing full coverage for larger cases. It can also appear in some health or specialized contracts, depending on insurers.

Absolute deductible :

The absolute deductible is the most common type in insurance contracts, especially in auto and home insurance. It operates systematically: the amount of the deductible is always deducted from the compensation, regardless of the severity of the claim.

Specifically, the insured is only compensated if the damage amount exceeds the deductible. And even then, they receive only the difference between the claim amount and the contractual deductible.

👉 Detailed example :

-

If the deductible is set at €150 and the claim is €100, you will receive no compensation, because the damage is less than the deductible.

-

If the claim reaches €200, the insurer will only reimburse you €50 (200 – 150).

-

For a claim of €1,000, you will be compensated up to €850 (1,000 – 150).

To remember : with the absolute deductible, the deduction applies in all cases where the claim exceeds the deductible. The insured must therefore always cover a portion of the costs.

✅ Advantages of the absolute deductible

-

Predictability : the amount of the deductible is clear and known in advance, facilitating claim management.

-

Reduced insurance premium : the higher the deductible, the often lower the premium.

-

Risk sharing : it makes the insured responsible by leaving them a part of the claim cost.

❌ Disadvantages of the absolute deductible

-

The insured is never fully compensated, even for very significant claims.

-

It can be burdensome for small claims, where final compensation might seem minimal.

-

It can be perceived as disadvantageous compared to the relative deductible, as the insured always has to participate financially.

📌 Application areas

The absolute deductible is widespread in most auto insurance contracts (glass breakage, accidents, theft, fire) and in home insurance (fire, water damage, burglary). It is favored by insurers because it reduces the number of small cases and systematically shares the cost of claims with the insured.

Proportional deductible :

The proportional deductible is a specific form that varies based on the amount of damage incurred. Unlike fixed or absolute deductibles, it does not correspond to a predetermined amount but to a percentage applied to the claim amount.

To prevent abuse or extreme situations, this deductible is always bounded by two limits:

-

a minimum deductible (floor amount below which the deductible cannot go),

-

and a maximum deductible (ceiling beyond which the deductible cannot increase).

👉 Detailed example (10% deductible with min. €250 and max. €450):

-

If the damage is €2,600, the deductible is €260 (10%). Since this amount is between the minimum and maximum, it is applied as is.

-

If the damage is €2,200, the 10% amounts to €220, but since it’s less than the minimum, the applied deductible will be €250.

-

If the damage is €5,600, the 10% amounts to €560, but since it exceeds the set ceiling, the deductible will be limited to €450.

To remember : the proportional deductible is flexible since it adapts to the size of the claim but also ensures fairness through the minimum and maximum system.

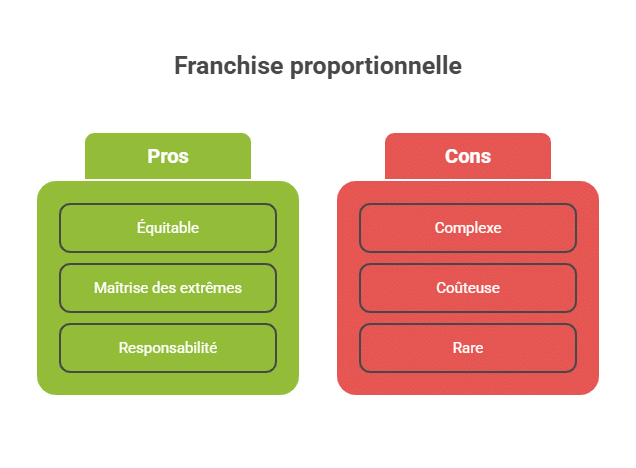

✅ Advantages of the proportional deductible

-

It is fair: the more significant the claim, the higher the insured’s proportional participation.

-

The minimum and maximum system allows controlling extremes and avoiding too heavy or too minimal charges.

-

It promotes responsibility as the insured always participates proportionally.

❌ Disadvantages of the proportional deductible

-

Can be complex to understand for the insured, especially with minimum and maximum notions.

-

Can be costly for medium to high claims because the deductible amount can increase rapidly.

-

Rarely offered in traditional contracts, it remains less common than the absolute deductible.

📌 Application areas

The proportional deductible is mainly encountered in certain specialized contracts, such as professional insurance or for particular risks (transport, fleet insurance, industrial risks). It is less common in home or auto insurance contracts for individuals.

The specifics of home insurance deductibles: choices and implications

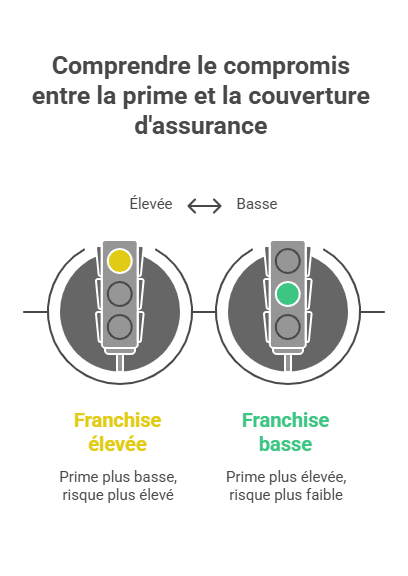

When choosing home insurance, one of the fundamental aspects to consider is the type of deductible applicable. Selecting an appropriate deductible level for your home insurance can significantly influence your annual premium, as well as the claim amount. For example, a high deductible can lower your premium but also means you’ll pay a larger part of the costs in the event of damage to your residence. It is an important calculation for homeowners and tenants who must weigh the risk against the potential cost.

Impact of different deductibles on claim management

Before proceeding, you need to understand how each type of deductible influences claim handling. With an absolute deductible, for instance, the claim must exceed the deductible amount for the insurance to act, which can be a barrier for frequent small damages. Conversely, a proportional deductible adjusts based on the claim amount, which can be fairer but requires careful review of the contract terms to avoid unpleasant surprises. Therefore, choose your deductible based on your specific needs and risk tolerance to optimize your coverage and peace of mind in daily life.

Comparison: high deductible vs low deductible

It is common to hesitate between a high deductible and a low deductible. Each option has its advantages and disadvantages.

-

A high deductible allows for lower insurance premiums. It is attractive for policyholders who consider themselves at low risk of claims. However, if a damage occurs, the insured’s share can be very significant.

-

A low deductible offers better protection in case of claim, as the insurer’s coverage is higher. On the other hand, the annual premium is typically more expensive.

👉 Comparative table to include:

| Type of deductible | Advantages | Disadvantages |

|---|---|---|

| High | Lower insurance premium 💰 | Lighter burden in case of claims ⚠️ |

| Low | Better coverage ✅ | Higher annual premium 📈 |

Therefore, the right choice depends on the insured’s profile, risk tolerance, and available budget.

FAQ about deductibles in insurance

What is a fixed deductible?

The fixed deductible is a sum of money remaining at your expense in case of a claim covered by your insurance. It represents part of the costs you must bear when using your policy’s coverages. The fixed deductible is specified in your insurance contract and remains the same regardless of the incurred expenses. It can be expressed as a percentage or a fixed amount depending on the type of coverages subscribed. For example, if you have auto insurance with a fixed €150 deductible for damages caused to a third party, you will need to pay the €150 plus your premium.

What is a fixed deductible and how is it defined?

The fixed deductible is a sum of money remaining at your charge in case of a covered claim. It represents part of the costs you must handle when using your insurance coverages. It is defined in your contract and remains the same regardless of the amount of expenses incurred.

It can be expressed as a percentage or a fixed amount depending on the type of coverage subscribed. For example, if you have car insurance with a fixed €150 deductible for damages caused to a third party, you will pay the €150 plus your premium.

The fixed deductible is generally used to reduce the cost of the insurance premium. By accepting to cover part of the costs in case of a claim, you can obtain a lower premium. However, it is important to understand the terms of the fixed deductible before subscribing to a contract to know what will remain at your charge in case of a claim.

What are the advantages and disadvantages of a fixed deductible?

Advantages:

- The insurance premium is usually lower when a fixed deductible is included in the contract.

- The fixed deductible can be suitable for individuals with a low risk of using their coverages.

Disadvantages:

- In case of a claim, you will need to pay the fixed deductible in addition to the premium. If the incurred expenses are high, this can represent a significant amount at your charge.

- The fixed deductible remains the same regardless of the amount of expenses, which can be advantageous in some cases but also disadvantages if expenses are very high.

- If you subscribe to insurance with a fixed deductible, you must be vigilant in respecting the conditions of the deductible to avoid financial penalties in case of a claim.

Can the fixed deductible amount be negotiated with the insurer?

It is possible to negotiate the amount of the fixed deductible with your insurer, but this depends on the insurer’s policy and its flexibility. Some insurers are more accommodating than others in negotiating the fixed deductible, while others are less willing to modify it.

Here are some factors that may influence the possibility of negotiating the fixed deductible:

- Your risk profile: If you have a good driving record or live in a low-risk area for fires, for example, your insurer may be more inclined to negotiate the deductible amount.

- Your insurance contract type: Some insurances are more complex, making it harder to negotiate the fixed deductible. For example, it may be easier to negotiate a car insurance deductible than one for life insurance, which involves numerous guarantees and variables.

- Your loyalty level: If you are a loyal customer, the insurer may be more willing to negotiate the deductible amount.

What is a variable deductible and how does it work?

A variable deductible is a sum of money that remains at your charge in case of a covered claim but varies according to the amount of expenses incurred. Unlike the fixed deductible, which is predefined and remains the same regardless of expenses, the variable deductible is proportional to the costs incurred.

Here’s how a variable deductible can operate:

- If you have car insurance with a 10% variable deductible for damages caused to a third party, you will pay 10% of the expenses plus your premium. For example, if expenses amount to €1,000, you will pay a deductible of €100 (10% of €1,000).

- If you have home insurance with a €50 variable deductible for a claim, you will pay €50 plus your premium, regardless of the expenses incurred. If expenses are higher than €50, you will pay the €50 deductible plus a part of the additional costs.

The variable deductible is advantageous if expenses are low because it prevents paying a high deductible amount. However, it can be costly if expenses are significant because you will then pay a part of the damages in addition to the premium.

Understanding the terms of the variable deductible before subscribing to an insurance contract is crucial to know what will remain at your charge in case of a claim.

What are the minimum and maximum deductible, and what are they used for?

The minimum deductible is the lowest amount of the deductible remaining at your expense in case of a covered claim. It is specified in your contract and cannot be less than this amount.

The maximum deductible is the highest amount of the deductible remaining at your expense in a covered claim. It is also specified in your contract and cannot exceed this amount.

The minimum and maximum deductibles are used to frame the variable deductible, which varies based on incurred expenses. If you have insurance with a variable deductible, it cannot be less than the minimum or more than the maximum.

Here’s an example of how the minimum and maximum deductibles work:

- If you have car insurance with a variable deductible of 10% and a minimum deductible of €50, you will pay €50 if expenses are less than €500 (since €50 is 10% of €500). If expenses exceed €500, you will pay 10% of the expenses plus your premium.

- If you have home insurance with a €50 variable deductible and a €500 maximum, you will pay €50 if expenses are less than €1,000 (since €50 is 5% of €1,000). If expenses surpass €1,000, you will pay a maximum of €500 regardless of the expenses incurred.

The minimum and maximum deductibles help limit the costs you must cover in case of a claim and better control your budget. It is important to understand their terms before subscribing to an insurance contract to know what remains at your charge.

Is it possible to eliminate the deductible in an insurance contract?

It is possible to eliminate the deductible in an insurance contract, but this will usually result in a higher insurance premium. By agreeing to cover part of the costs in case of a claim, you can obtain a lower premium. If you wish to eliminate the deductible, you should be prepared to pay a higher premium.

It is important to note that removing the deductible may not be possible in some cases. For example, some insurance companies may impose a minimum deductible that cannot be waived. In such cases, you will pay the minimum deductible in addition to your premium, even if you have chosen to eliminate the deductible.

It is recommended to understand the deductible terms thoroughly before subscribing, to know what will remain at your charge in case of a claim. If you want to eliminate the deductible, discuss with your insurer whether it is possible and at what cost. You can also compare offers from other insurers to find one that allows removing the deductible without significantly increasing the premium.

What happens if conditions of the deductible are not respected (e.g., failure to report a claim)?

It is important to respect the conditions of the deductible specified in your insurance contract to avoid financial penalties in case of a claim. If you do not respect these conditions, your insurer may refuse to cover the incurred expenses, and you will have to pay them entirely.

Here are some examples of potential consequences of not respecting the deductible conditions:

- If you fail to report a claim when required, your insurer may refuse to cover the associated costs, and you will have to pay them yourself.

- If you do not meet the reporting deadlines specified in your contract, your insurer may refuse to cover expenses or apply an additional deductible.

- If you do not adhere to claims prevention obligations (for example, by not implementing recommended safety measures), your insurer may refuse coverage or apply an additional deductible.

Therefore, it is essential to understand the deductible conditions before subscribing to a contract, to know what remains at your charge and to comply with these conditions to avoid issues.

Does the deductible apply to all coverages in my insurance contract or only some?

The deductible may apply to some or all coverages in your insurance contract, depending on the terms of your policy. It is therefore important to read your policy conditions carefully to understand which coverages are concerned and under what conditions the deductible applies.

Here are some examples of cases where the deductible may apply:

- If you have car insurance with a €150 deductible for damages caused to a third party, the deductible will only apply to the damages related to the third-party liability (for example, civil liability).

- If you have home insurance with a €50 deductible for a claim, the deductible will apply to all coverages related to covered risks (for example, fire, water damage, theft).

Understanding the terms of the deductible before subscribing to an insurance contract is crucial to know what will be at your charge in case of a claim and to choose the coverages that best suit your needs. If in doubt, do not hesitate to contact your insurer or carefully review your policy conditions.

🚗 Assurance Auto — Articles liés

🔧 Protégez votre véhicule contre les pannes mécaniques

La garantie panne mécanique couvre les réparations imprévues après la garantie constructeur. Obtenez un devis personnalisé en 2 minutes.

Obtenir un devis gratuit →Lien sponsorisé

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.