Summary

| 📜 Section | 📝 Description |

|---|---|

| 🛑 Definition | Non-payment of insurance premium refers to the failure to pay the premium by the agreed deadline in the insurance contract. |

| 📉 Causes | 1. Financial Difficulties: Lack of financial resources. 2. Forgetfulness: Lack of reminders or distractions. 3. Unfamiliarity: Misunderstanding of deadlines or amounts. 4. Disagreement: Dissatisfaction with the terms of the contract. |

| ⚠️ Consequences | 1. Contract Termination: Loss of insurance coverage. 2. Penalties: Late fees and other financial penalties. |

| 🚗 The 10-30-10 Rule | Specific rule for motor vehicle insurance allowing contract termination if premiums are not paid within specified deadlines (10 then 30 then 10 days). |

| 💡 Solutions | 1. Choosing Payment Method: Adapt payment method to financial situation. 2. Payment Reminders: Use reminders to avoid forgetfulness. 3. Modifying Terms: Negotiate more flexible conditions with the insurer. 4. Negotiating Conditions: Adjust contract terms to reduce costs or improve coverage. |

Non-payment of insurance premium is an important issue affecting many policyholders. Indeed, various reasons may cause someone to fail to pay their premium on time. Non-payment can lead to serious consequences for both the insured and the insurer.

Definition of Non-Payment of Premium in Insurance

Non-payment of an insurance premium refers to the fact of not paying the premium due at the scheduled date in the insurance contract. The insurance premium is the amount the insured must pay to the insurer in exchange for the coverage provided by the insurance contract.

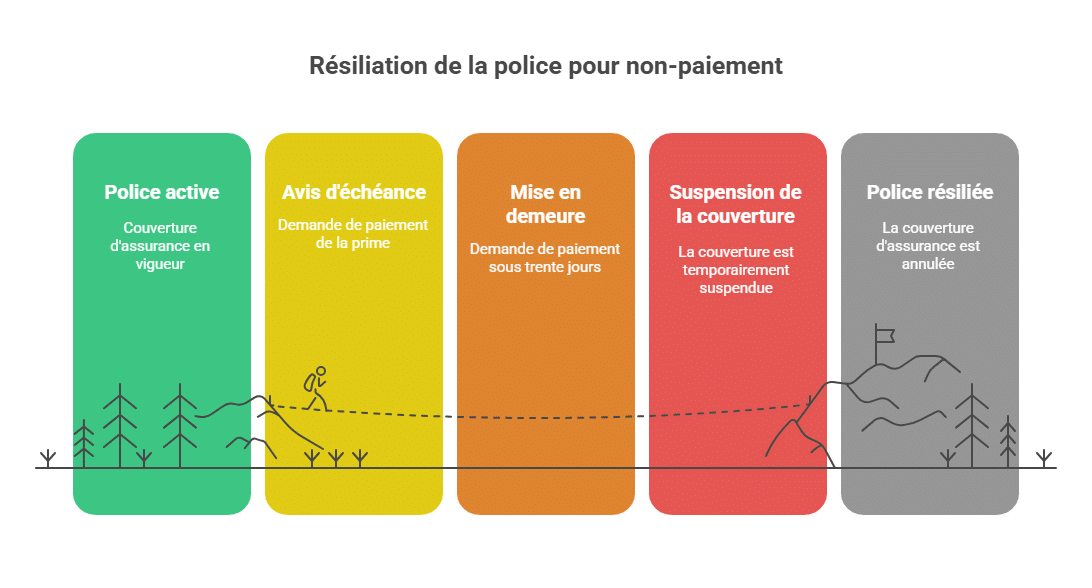

Legal Framework for Non-Payment of Premium in Insurance

Failure to pay an insurance premium is not only a matter of financial difficulty or forgetfulness: it is a situation regulated by law.

📌 Legal References

In France, it is Article L.113-3 of the Insurance Code that sets the procedure:

-

Formal Notice: The insurer must send a registered letter with acknowledgment of receipt to the client.

-

Suspension of Coverage: After 30 days without regularization, insurance is suspended. The insured is no longer covered.

-

Permanent Termination: If, after an additional 10 days, the premium is still unpaid, the contract is terminated.

⚠️ Without respecting these deadlines, termination can be legally challenged.

📊 Concrete Example

-

Scheduled deadline: March 1st.

-

Formal notice sent on March 10th.

-

Coverage suspended from April 10th.

-

Effective termination on April 20th if no payment is made.

👉 This framework protects the insured against abrupt termination, while providing the insurer a clear framework to act within.

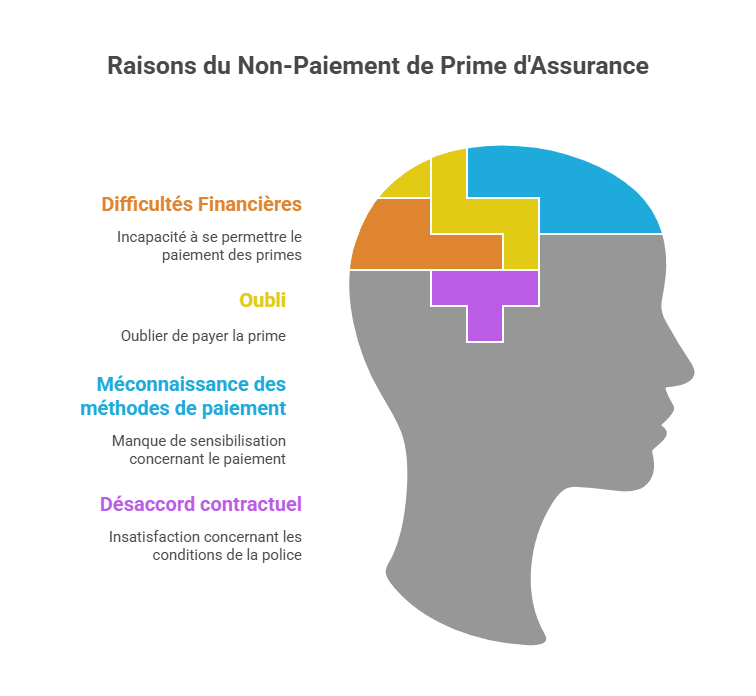

Causes of Non-Payment of Insurance Premium

Financial Difficulties

One of the main causes of non-payment is the difficulty in finding means to pay the premium. Policyholders may face financial difficulties for various reasons, such as loss of employment, a decrease in income, or unexpected expenses. These situations can prevent them from paying their insurance premium on time. For some, the budget is already <strong tight, and adding an insurance premium can be financially inaccessible.

Forgetfulness

Sometimes, policyholders forget to pay their insurance premium. This forgetfulness may be due to an obstacle such as illness or travel, a lack of vigilance, or simply a lack of knowledge of payment terms. People with busy schedules or those managing multiple finances can easily miss the due date. A simple forgetfulness can thus lead to unexpected and often costly consequences.

Unfamiliarity with Payment Methods

It happens that policyholders are unaware of the payment methods for their insurance premium. They might not know, for example, the due date of the premium or the amount to pay. This unfamiliarity can result from insufficient communication from the insurer or a poor understanding of the contract terms. In some cases, policyholders may be unaware of options available to facilitate payment, such as automatic withdrawals or installment payments.

Disagreement with Contract Terms

In some cases, policyholders may refuse to pay their insurance premium because they do not agree with the conditions of the insurance contract. They may think that the proposed coverages are insufficient or that the premium amount is too high. Policyholders may also be dissatisfied with the services provided or feel that they are not receiving good value for money. This dissatisfaction can lead them to delay or refuse to pay, hoping to obtain a better offer or an adjustment of the contract.

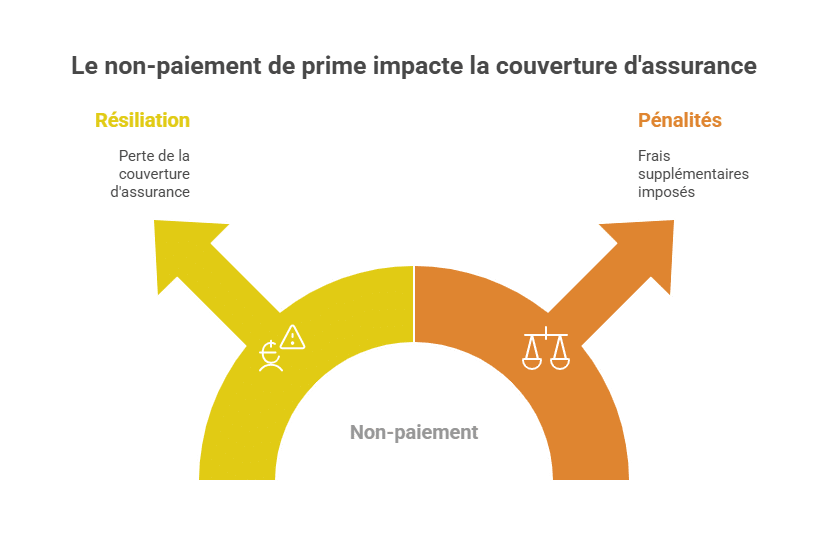

Consequences of Non-Payment of Premium in Insurance

Contract Termination

The non-payment of insurance premiums can lead to the termination of the insurance contract, meaning that the insured loses their coverage. This can be very detrimental in case of a claim, when the insured needs to benefit from the coverage provided by their policy. Without coverage, damages or repairs costs must be borne entirely by the insured, which can have financially devastating consequences. Losing coverage also means the insured can no longer benefit from protection against risks for which they originally purchased insurance.

Payment of Late Fees or Penalties

The non-payment of insurance premiums can also result in the payment of late fees or penalties, significantly increasing the insurance cost for the insured. These penalties are often imposed to compensate for late payment and can accumulate quickly, increasing the total amount owed. In addition to unpaid premiums, the insured must also pay additional charges, further complicating their financial difficulties. Late fees can also negatively impact the relationship between the insured and the insurer, making future negotiations for better terms more difficult.

Impact on Unpaid Files

When a contract is terminated for non-payment, the insurer may report the insured to the AGIRA (Association for Risk Information Management in Insurance).

Direct Consequences

-

Difficulty in obtaining a new policy from a traditional insurer.

-

Access only possible to specialized offers, often more expensive.

-

Example: in auto insurance, the insured may be forced to go through the Central Pricing Office (BCT) to obtain at least the mandatory civil liability coverage.

Financial Consequences

-

Application of surcharges (significant rate increases).

-

Refusal of promotional offers or payment facilities.

👉 Being listed as a “bad payer” in insurance is a lasting handicap, sometimes for several years.

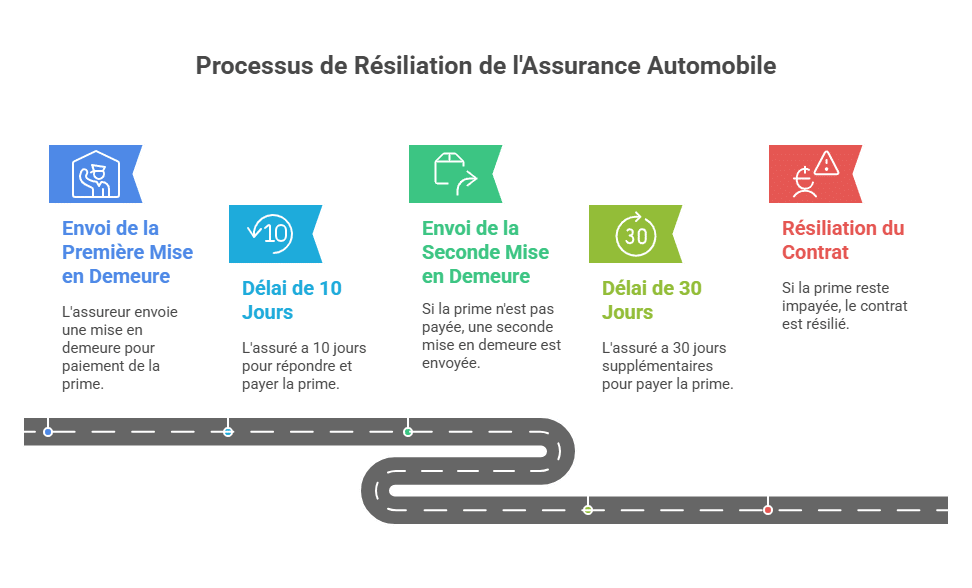

The 10-30-10 Rule in Auto Insurance

The 10-30-10 rule is a specific provision regarding non-payment of the premium in auto insurance. It allows the insurer to cancel the auto insurance policy if the insured does not pay their premium within the timeframes specified by the contract. According to this rule, the insurer must first send a formal notice to the insured, requesting payment of their premium within a period of 10 days. If the insured does not respond to this formal notice and does not pay their premium within this period, the insurer can then send a second formal notice requesting payment within a period of 30 days. If the insured still does not respond and does not pay within this second period, the insurer can then terminate the auto insurance contract. It is important to note that the 10-30-10 rule only applies to auto insurance contracts and that the notice and termination periods may vary depending on the insurance contracts and insurers. It is therefore recommended to inquire with your insurer to understand the payment procedures and the consequences of non-payment in insurance.

| Step | Insurer’s Action | Deadline | Consequences for the Insured |

|---|---|---|---|

| First Formal Notice | Sending a formal notice for premium payment | 10 days | Must pay the premium within this period |

| Second Formal Notice | Sending a second formal notice if the premium is not paid | 30 days | Must pay the premium within this period |

| Contract Termination | Contract termination if the premium still isn’t paid | After 30 days | Insurance contract is canceled, coverage lost |

Differences Between Types of Insurance

All insurances follow the Insurance Code, but some specificities exist.

Auto Insurance

-

Strict application of the 10-30-10 rule.

-

The insured remains responsible in case of an accident: they will have to compensate victims out of pocket if the contract is suspended.

-

Example: a material accident costing €15,000 can directly impact the policyholder for non-payment.

Home Insurance

-

Suspension results in the absence of coverage in case of fire, water damage, or theft.

-

Risk: having to finance repairs alone, which can reach several tens of thousands of euros.

Health and Provident Insurance

-

Coverage (medical expenses, daily allowances) ceases at the expiration of the legal period.

-

Particular case of group policies: some specify specific deadlines or temporary coverage continuity.

👉 This illustrates that the risk linked to non-payment varies depending on the contract, but it always has heavy consequences.

Pas le temps de ficher tout le programme ?

Découvre l'E-book de révision avec 100% des cours de 1ère et 2ème année synthétisés. L'outil indispensable, créé par un diplômé, pour valider ton BTS sans stress.

Découvrir l'E-bookCase Study: Cancellation for Non-Payment

Context

An insurer sent a due date notice for a premium payable before December 1, 2019, covering the period from December 1, 2019, to November 30, 2020. In the absence of payment, a formal notice was sent on December 23, 2019, requesting settlement before January 21, 2020.

Suspension and Termination

Since the premium was not paid within the thirty days following the formal notice, the contract’s coverage was suspended. Ten days after this suspension, and still without payment, the contract was terminated on January 31, 2024, in accordance with legal deadlines.

Regularization and Reinstatement Request

The insured settled their premium payment on February 5, 2024, after the contract was terminated. They then requested either the reinstatement of the contract or a refund of the paid premium.

Decision of the Mediator

According to Article L.113-3 of the Insurance Code, coverage may be suspended thirty days after an ineffective formal notice, followed by a contract termination ten days after this suspension. A non-terminated contract can resume its effects at noon the day after the overdue premium and those due during the suspension are paid.

However, once the contract is ended, the insurer is not obliged to reinstate it even after regularization. In this case, the insurer nonetheless refunded the premium for the period after the termination, which they were not required to do. The Mediator confirmed that the insurer was not obliged to reinstate the contract and that the refund was satisfactory.

Proactive Management by Insurers

Contrary to popular belief, insurers do not have an interest in terminating all late-paying clients.

Measures Implemented

Automatic reminders via SMS and emails before the deadline.

Personalized phone calls from advisors.

Payment facilities: monthly installments, exceptional deferments.

Loyalty offers: discounts for online or direct debit payments.

Concrete Example

A policyholder behind on their home insurance premium may be offered a 3-month installment plan instead of immediate cancellation. This allows the insurer to retain the customer and the insured to regularize their situation.

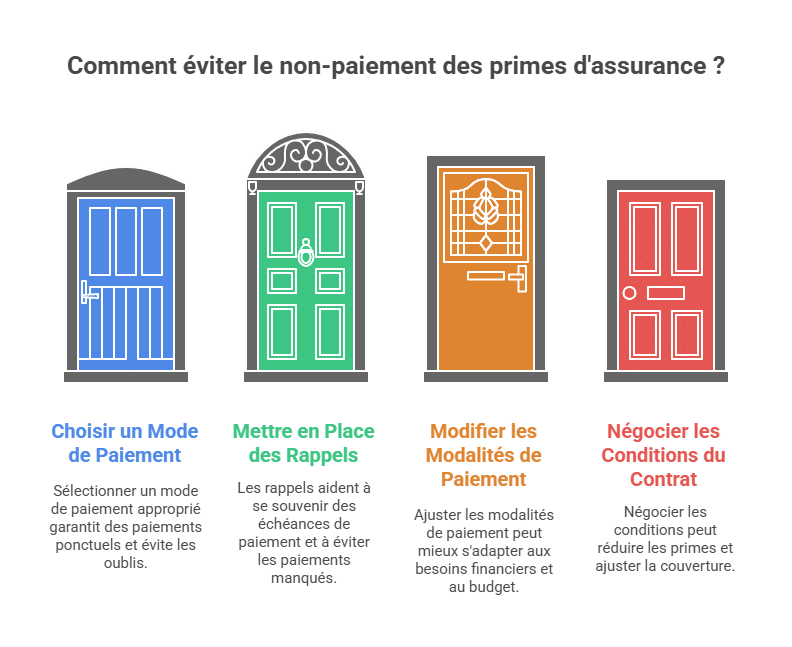

Solutions to Prevent Non-Payment of Insurance Premiums

Choose an Appropriate Payment Method

It is essential to select a payment method that suits your financial needs to prevent forgetting and ensure timely payment of premiums. The available payment options are varied and may include automatic withdrawals, check payments, or bank transfers. Automatic withdrawal is often the best solution for those who want to ensure their premium is paid regularly, without worrying about deadlines. By choosing the most appropriate payment method for your financial situation, you can minimize the risks of non-payment.

Implement Payment Reminders

Payment reminders can help prevent forgetting to pay your insurance premium on time by providing notifications before each deadline. These reminders can be in the form of SMS messages, emails, or even phone alerts. Many insurers offer this service for free, and it can be activated simply by contacting your insurer or using their online services. Payment reminders are especially useful for those with busy schedules or managing multiple accounts and payments simultaneously.

Modify Payment Terms

If current payment terms do not suit, it is possible to modify them with the insurer, for example by requesting installments or online payments. Some policyholders prefer monthly payments rather than annual ones to better manage their budget. By discussing these preferences with your insurer, it is often possible to find a flexible solution that allows you to spread costs more evenly throughout the year. Online payments also offer increased convenience and quickness, allowing policyholders to pay their premiums from anywhere and at any time.

Negotiate Contract Conditions

You can negotiate the terms of your insurance contract to reduce premium amounts or adjust the coverages according to your needs. Policyholders can compare offers from different insurers to find the best value for money. By discussing with your insurer, you can renegotiate aspects such as deductibles or included coverages, to obtain a more affordable premium. It may also be beneficial to review your risk profile and make improvements that could lead to discounts, such as installing security devices in a home or improving driving habits for auto insurance.

Choose an appropriate payment method

Automatic withdrawal = maximum security.

Monthly or quarterly payment = reduced budget effort.

Annual payment = possible discount but requires solid cash flow.

Set up reminders

SMS or email alerts before due date.

Mobile insurance apps with notifications.

Adjust your contract

Remove unnecessary coverages.

Review deductible level to lower premium cost.

Combine multiple contracts in the same company to benefit from multi-contract discounts.

Negotiate with your insurer

Request a special installment plan.

Discuss a reduction of temporary coverages.

Compare competing offers to put your insurer in competition.

Case Studies and Statistics

Numerical Data

6% of auto insurance cancellations are due to non-payment.

In home insurance, about 4% of contracts are affected.

The average cost of an unpaid premium is €350 for auto and €280 for home insurance (source: France Assureurs).

Real Example

An auto policyholder with an annual premium of €420 who did not pay saw their policy canceled. During a responsible accident, they had to pay out of pocket €8,500 in repairs.

👉 These figures highlight the importance of paying premiums on time.

Advice for BTS Insurance Students

Non-payment of premiums is a common practical issue in BTS Insurance, especially in the E5 (Claims Management and Customer Relations) exam.

Key points to remember

Cite Article L.113-3 of the Insurance Code.

Explain the 10-30-10 rule in auto insurance.

Explain the consequences for the insured: suspension, termination, listing, difficulties in re-insurance.

Propose practical solutions: installment plans, reminders, adjustment of coverages.

👉 Structuring your answer around the SWOT of the situation (strengths/weaknesses/opportunities/threats for the insurer and the insured) is a significant advantage in the exam.

Conclusion

Non-payment of an insurance premium is never just an overdue: it is a situation regulated by law, with serious consequences (suspension, termination, listing). However, solutions exist to prevent or regularize unpaid premiums: reminders, negotiations, suitable payment methods, or contract adjustments.

For professionals and students in insurance, this topic clearly illustrates the importance of client education: explaining, preventing, supporting. Because beyond the financial risk, it is about maintaining trust between the insured and their insurer.

FAQ – Non-payment of Insurance Premium

1. What is non-payment of insurance premium?

Non-payment of premium refers to the failure to settle the insurance premium by the specified date in the contract. This can be due to forgetfulness, financial difficulties, or disagreement with the insurer.

2. What does the law say about non-payment?

According to Article L.113-3 of the Insurance Code, the insurer must send a formal notice to the insured.

-

After 30 days, coverage is suspended.

-

After 10 additional days, the contract may be permanently canceled.

3. What are the consequences of non-payment?

The main consequences are:

-

Suspension then cancellation of the contract.

-

Loss of coverage in case of a claim.

-

Payment of late interest and penalties.

-

Possible listing in unpaid databases (AGIRA), making it difficult to subscribe to a new policy.

4. How to avoid non-payment of premium?

To prevent this situation, it is recommended to:

Opt for automatic withdrawal.

Set up SMS or email reminders.

Choose a monthly or quarterly payment plan suitable for your budget.

Negotiate with the insurer if facing financial difficulties.

5. What is the 10-30-10 rule in auto insurance?

It is a specific rule for auto insurance:

10 days to regularize after the first formal notice.

30 days of suspension if the premium remains unpaid.

10 days after this suspension, the contract can be canceled.

6. Can you recover your contract after cancellation for non-payment?

No, once canceled, the contract cannot be reinstated, even if the premium is paid afterwards.

However, the insurer must refund the portion of the premium corresponding to the uncovered period after termination.

7. Is it possible to find insurance after non-payment?

Yes, but it can be difficult. The insured may face refusals or surcharges. In auto insurance, they can contact the Central Pricing Office (BCT) to force an insurer to provide at least the minimum legal coverage (civil liability).

8. What are the tips for BTS Insurance students?

In a practical case, the steps are:

Cite Article L.113-3.

Explain the 10-30-10 rule.

Detail the consequences for the insured and the insurer.

Propose concrete solutions (installment plans, reminders, coverage adjustments).

For further reading

https://youtu.be/8dlDNtx0A_Y

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.