In summary

| Part Title | Summary |

|---|---|

| The banking market and history of Crédit Agricole | A historic player in the sector, Crédit Agricole has a solid foundation with 24 million clients, 7,000 branches, and a strong territorial presence. Its net banking product (2016) reached €31.8 billion, confirming its position as a banking pillar in France. |

| Strengths of Crédit Agricole in the French banking landscape | Strong brand image, a “green” reputation, leadership in agriculture and growing bancassurance. Its crisis management has reinforced customer trust, and its international coverage is a major asset. |

| Internal weaknesses and organizational challenges | Administrative heaviness, high costs related to physical networks, ecological criticisms, and delayed digital adaptation. These factors weaken its responsiveness and sustainable image. |

| Growth and diversification opportunities | Potential in digitalization, green financing, client innovation, international partnerships, and bancassurance. These levers can enhance its competitiveness and meet societal expectations. |

| Competitive and environmental threats | Intense competition from BNP Paribas, BPCE, and online banks. Persistent ecological criticisms and rapidly changing customer expectations threaten its reputation stability and market share. |

| Comparison with other key players | BNP Paribas dominates with higher results, Société Générale diversifies and digitalizes, while Caisse d’Épargne and Banque Populaire capitalize on regional proximity. Crédit Agricole remains locally anchored but needs to accelerate innovation. |

| Impact of online banks and sector digitalization | Digitalization is transforming the market: pure players attract a young and agile clientele. Crédit Agricole must succeed with its hybrid strategy by combining proximity and modernity to avoid losing ground. |

| Recommended strategies to strengthen its position by 2025 | Accelerate digital transformation, invest in sustainable development, diversify offerings, and transform branch networks into modern hubs. These axes are essential to maintain a competitive advantage. |

| FAQ on SWOT analysis of Crédit Agricole | Crédit Agricole remains a leader in agriculture thanks to its territorial presence. Its main weaknesses concern organizational heaviness and ecology. To counter online banks, it must focus on a high-performing digital offering and strong human relations. |

Crédit Agricole holds a key position in the French banking landscape. With its centenary history, a network of 7,000 branches, and over 24 million clients, the group establishes itself as a reference player for individuals, businesses, and the agricultural sector. Faced with increasing competition, the rise of online banks, and growing demands in digitalization and sustainability, it is essential to analyze its strengths, weaknesses, opportunities, and threats for the years ahead. This SWOT analysis helps understand Crédit Agricole’s strategy and the levers it can deploy to consolidate its position in 2025.

- The banking market and history of Crédit Agricole

- Strengths of Crédit Agricole in the French banking landscape

- Internal weaknesses and organizational challenges

- Growth and diversification opportunities

- Competitive and environmental threats

- Comparison with other key players: BNP Paribas, Société Générale, etc.

- Impact of online banks and sector digitalization

- Recommended strategies to strengthen its position by 2025

- FAQ on SWOT analysis of Crédit Agricole

The banking market and history of Crédit Agricole: a pillar of the French financial sector

In the French financial landscape, Crédit Agricole stands out as a highly crucial actor, with a long history dating back to industrialization and France’s particular culture regarding savings and real estate investment. Far from being just a banking establishment, it is one of the historical references, alongside Caisse d’Épargne, Banque Populaire, and Société Générale. Created through its holding, Crédit Agricole SA, it now has approximately 24 million clients worldwide, both individuals and professionals, thus ensuring a solid base to maintain its dominant position.

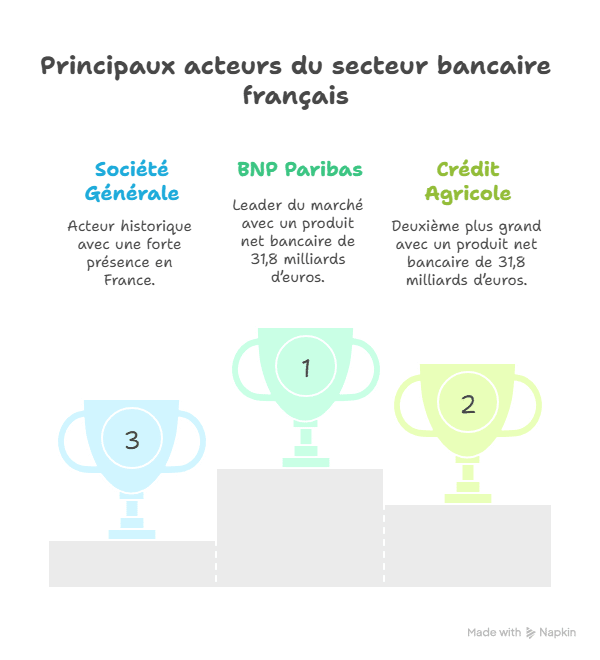

The banking market in France is valued between 150 and 160 billion euros, which is phenomenal, even with slight declines observed around 2015. This market is not assessed by traditional turnover but by the national banking product—a specific concept capturing all value-added by banks through various revenue sources: interest rates, commissions, management fees, etc. In 2016, Crédit Agricole reported a net banking income of €31.8 billion, positioning the group as the second-largest nationally, just behind BNP Paribas.

Regarding its presence, Crédit Agricole does not joke: around 7,000 branches are spread across France. It employs about 138,000 staff members, forming a dense and comprehensive network. Its strong local presence gives it a notable advantage, especially in the agricultural sector where it holds undisputed leadership, as well as among businesses and public authorities.

- 🌱 Long-standing history and territorial roots

- 📊 Extensive and diversified client base

- 🏦 Dense physical presence with 7000 branches

- 👨💼 Large staff with over 130,000 employees

- 💼 Leader in bancassurance despite late entry into this sector

| Element | Key Data 🌟 |

|---|---|

| Net banking income (2016) | €31.8 billion |

| Net profit (2016) | €4.825 billion |

| Number of branches | 7,000 in France |

| Number of employees | 138,000 |

| Number of clients | 24 million |

The richness of Crédit Agricole’s past and its current scope largely explain its strength, the solid foundations that allow the group to envisage the future with a certain capacity for adaptation. In a highly dynamic French market, this historic presence and diversity of activities give it a good chance to compete against Banque Populaire, Société Générale, La Banque Postale, or the rapid emergence of digital banks like Hello Bank! or ING Bank.

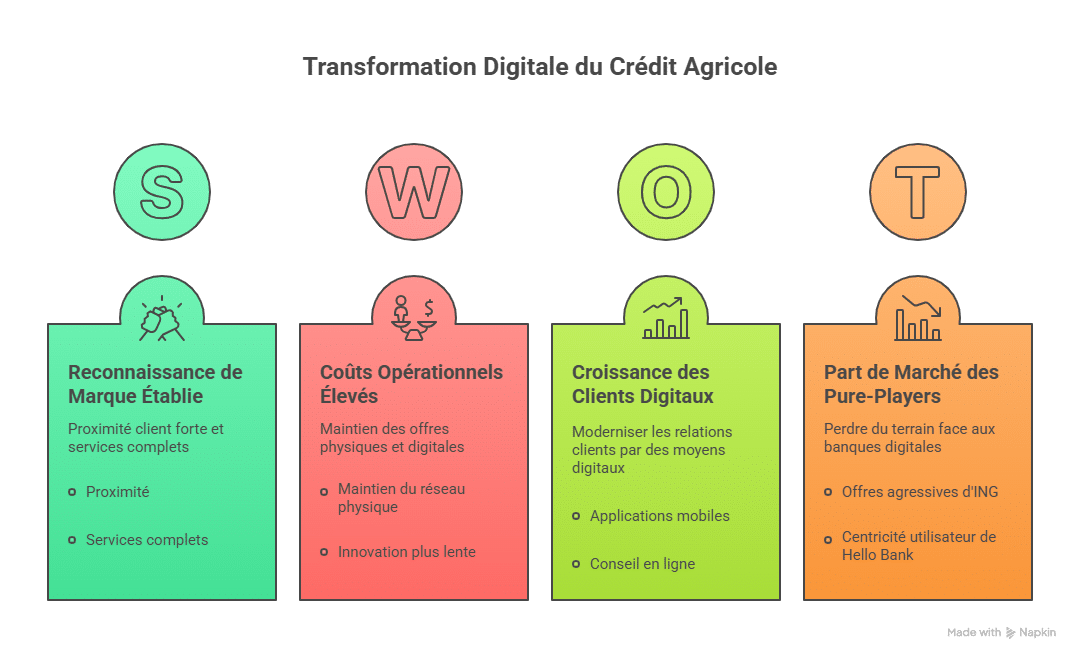

Strengths of Crédit Agricole in the French banking landscape in 2025

In an increasingly competitive banking world, Crédit Agricole exercises strengths based on several very solid pillars. Firstly, the historic identity with a well-established brand, notoriety that inspires confidence, and a deep territorial vocation. Its slogan “A whole bank for you” resonates with the human and close role the group seeks to embody—a positioning that remains highly relevant to retain customer loyalty.

The group is an undisputed leader in certain key segments: notably for the agricultural sector, for businesses, and also for local authorities. Its diversification into bancassurance was late but successful, illustrating its ability to catch up and gain market shares in sectors where competition is fierce.

Credit Agricole has maintained a somewhat responsible stance, especially after the economic crisis of 2008 and its consequences. A rapid repayment process to the state and a clear position regarding controversial issues such as the Panama Papers in 2016 demonstrate a desire to safeguard its image and avoid mistakes that could tarnish its reputation.

Here is a summary of the major assets:

- 💚 Solid brand image and “green” reputation

- 🌍 Extensive coverage with 24 million clients internationally

- 🌾 Leadership in the agricultural sector and among businesses

- 🔄 Constantly growing bancassurance

- 🤝 Crisis management fostering customer confidence

| Main Strengths | Description and Important Data |

|---|---|

| Visual identity & marketing | “Green bank” style, calming colors, humanist message |

| International client base | 24 million clients |

| Position in the agricultural market | Undisputed leader |

| Bancassurance | Second place, recent growth |

| Crisis responsiveness | Rapid repayment of government loans |

Public trust remains a decisive factor. While other actors like BNP Paribas or Société Générale may suffer from scandals, this legacy of integrity is a strong lever. Crédit Agricole also aims to capitalize on its relationships with public authorities to ensure a stable flow of business. This responsible stance could weigh heavily in the years to come.

Internal weaknesses and organizational challenges of Crédit Agricole

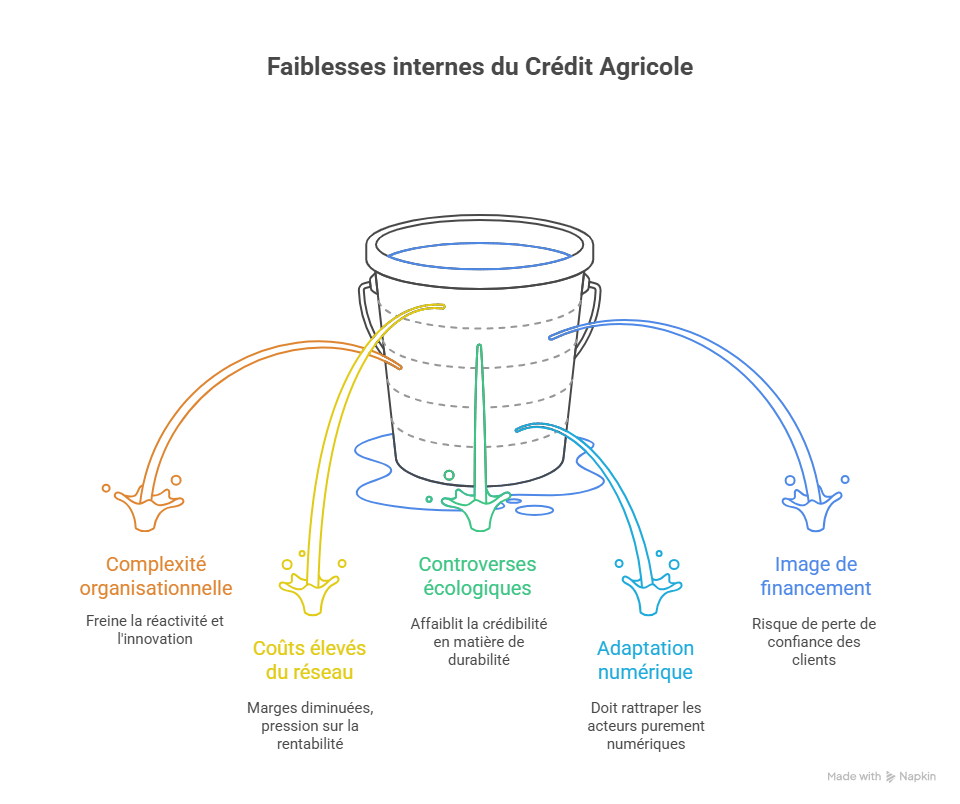

Despite notable assets, Crédit Agricole must deal with certain weaknesses that hinder its growth and could cause friction for its future development. Among these, organizational complexity is one of the most critical. The extent of the group, with its numerous subsidiaries and regional components, can sometimes lead to inefficiencies and a lack of agility in decision-making.

The strong physical presence, with 7,000 branches, also presents an increasingly delicate challenge: managing these customer service points at high costs amid rising digitalization. More agile banks like Hello Bank! or ING Bank attract a younger clientele with significantly lower operational costs. From this perspective, Crédit Agricole must juggle between modernization and maintaining proximity services.

Furthermore, on the environmental front, the group is often criticized. Associations like Les Amis de la Terre accuse it of having too heavy an ecological footprint. Its financing of sensitive sectors such as nuclear energy fuels ongoing controversies, which damage its image among increasingly environmentally-conscious clients.

- ⚠️ Organizational complexity and administrative heaviness

- 🏦 High costs related to maintaining an extensive physical network

- 🌱 Ecological impact controversies

- 📉 Difficulties in rapidly adapting to new technologies

- 🔍 Sometimes negative perception due to sensitive financing

| Internal weaknesses | Effects and implications |

|---|---|

| Organizational heaviness | Hinders responsiveness and innovation |

| Network maintenance costs | Margin reduction, profitability pressure |

| Ecological controversies | Weakens credibility in sustainable development |

| Digital adaptation | Needs to catch up with pure players |

| Image concerning financing | Risk of losing customer trust |

It is essential for Crédit Agricole to address these weaknesses to prevent competitors from taking market share in an already tense environment. Currently, although the group remains largely dominant, its complex internal functioning limits the speed at which it can deploy innovations or adjust strategies.

Growth and diversification opportunities for Crédit Agricole in 2025

In the face of challenges, Crédit Agricole also has promising opportunities to move forward and strengthen its position in a rapidly evolving banking sector. Digitalization of the banking sector is an essential lever to seize. Integrating technological innovations and offering services tailored to a connected public are major challenges and obvious growth avenues.

The rise of neo-banks and pure players compels Crédit Agricole to reinvent itself, for example by developing its online banking activities while leveraging its physical network to offer a hybrid service combining proximity and digital technology. Banks like ING Bank or Hello Bank! have successfully taken advantage of the loss of trust associated with traditional banks after 2008, notably through aggressive offers such as sign-up bonuses.

Sustainable development can also become a real marketing lever if managed concretely. In stark contrast to its critics, the group has the capacity to direct its financing towards ecological projects and to revise its internal policies to become a more “green” bank in the true sense of the term.

- 📱 Expansion of digital services and online banking

- ♻️ Investments in environmental initiatives and energy transition

- 🌐 International development through strategic partnerships

- 💡 Technological innovation to enhance customer experience

- 📈 Growth of bancassurance sector

| Opportunities to explore | Potential Impact |

|---|---|

| Increased digitalization | Attracting young clients, reducing costs |

| Green financing | Enhancing image, meeting societal expectations |

| International partnerships | Expanding clientele and influence |

| Client innovation | Customer loyalty and market differentiation |

| Bancassurance | Source of revenue and diversification |

These avenues are not just options but strategic axes to build the future. By 2025, quick adaptation to these market shifts will be a survival issue to maintain a leading position in the French banking landscape and beyond.

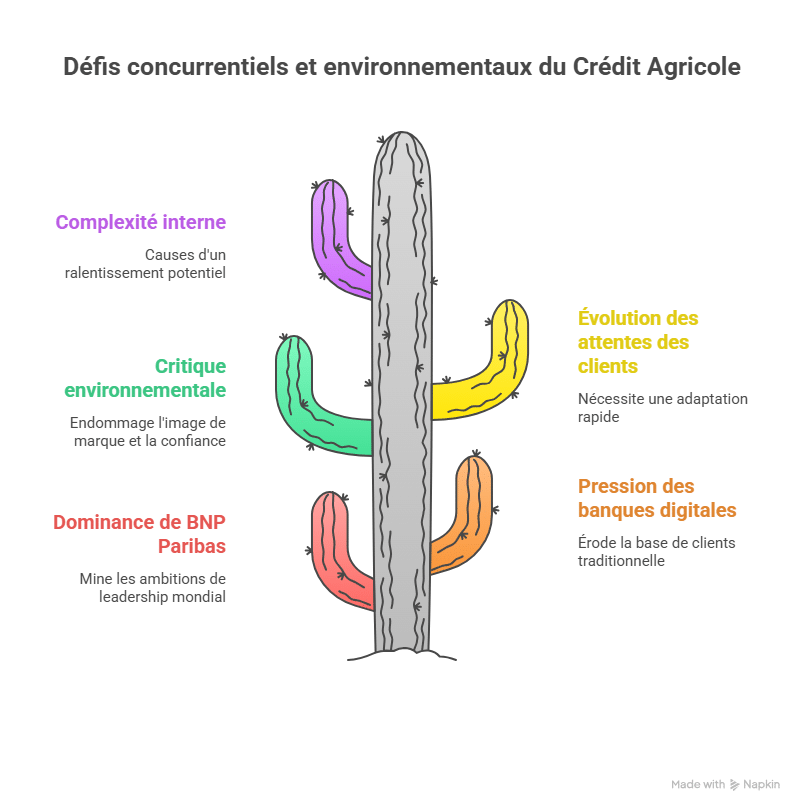

Competitive and environmental threats for Crédit Agricole

The shadow of competition heavily looms over Crédit Agricole, particularly with a giant like BNP Paribas on the market. The Parisian bank achieves nearly double the net result of Crédit Agricole, making the consolidation of a global leader position almost impossible. However, subtlest threats also arise from the ground, concerning trust, ecology, and rapidly evolving customer expectations.

The threat also comes from the rising strength of online banks and new entrants, pushing traditional banks to thoroughly overhaul their offerings. The example of ING Direct, the leading online bank in France with one million clients, clearly illustrates how a digital actor can attract a more youthful, connected clientele. Another factor to consider is the narrower gap between Crédit Agricole and Caisse d’Épargne (BPCE), the third-largest French banking group, indicating that the battle for the podium could intensify.

The group is also frequently criticized for its ecological impact (funding nuclear power, resource exploitation, etc.), which affects its image among a more environmentally-conscious public. Satirical awards, such as the “Pinocchio Prize,” have highlighted these flaws and could weigh on the trust placed by certain market segments.

- ⚔️ Fierce competition with BNP Paribas and BPCE

- 🌐 Growing pressure from online banks and pure players

- 🌍 Environmental criticisms and reputation repair often needed

- 🔄 Rapid and changing customer expectations

- 📉 Potential slowdown due to internal complexity

| Threats | Associated Risks |

|---|---|

| Intense competition | Loss of market share to BNP Paribas and BPCE |

| Digital banks | Decreased traditional clientele |

| Environmental issues | Brand image weakening |

| Market volatility | Need for rapid adaptation |

| Internal complexity | Inertia against change |

In this context, Crédit Agricole must carefully monitor its environment and adapt swiftly. The ability to stay agile and listen to weak signals in the market will be a key factor in preventing loss of ground to La Banque Postale, LCL, or AXA Banque which are also strengthening their digital offerings.

Comparison with other key players: BNP Paribas, Société Générale, and challengers

The real battle for leadership is fought between several behemoths. BNP Paribas leads the pack with a net result twice that of Crédit Agricole, exerting constant pressure. Société Générale, Caisse d’Épargne, and Banque Populaire form the top tier of the French banking scene shaping the competition. Each has its own specifics, strengths, and weaknesses, but none has yet succeeded in definitively outpacing the others.

To better understand this dynamic, it is enough to look at their strategies and profiles. BNP Paribas, for example, focuses heavily on investment banking and international markets, with a more global clientele. Crédit Agricole, by comparison, remains rooted locally and focuses on individual and SME services. Société Générale also emphasizes diversification while seeking to gain ground digitally against pure players.

- 🏦 BNP Paribas : market leader, strong in investment banking

- 🌍 Crédit Agricole : local roots and leadership in agriculture

- 🌐 Société Générale : diversification, digital development

- 🏢 Caisse d’Épargne and Banque Populaire : strong regional presence and proximity clientele

| Banks | Strengths | Positioning |

|---|---|---|

| BNP Paribas | Leader with double net result, international | Global investment bank |

| Crédit Agricole | Strong historical roots, agricultural clientele | Proximity bank, bancassurance |

| Société Générale | Diversified and digital strategies | Direct competition in retail banking |

| Caisse d’Épargne & Banque Populaire | Strong regional network | Proximity services |

The challenge for Crédit Agricole will be to balance its heritage with the necessities of innovation and efficiency. The competition, especially from digital banks, now demands a faster pace, continuous evolution of offerings, and refined communication tailored to current consumer expectations.

The impact of online banks and sector digitalization in France

The digital revolution in the banking sector is profoundly disrupting traditional players like never before. Among the banks that have benefited from this trend, ING Bank and Hello Bank! stand out with aggressive commercial offers and a customer-centric approach focused on connected users. These pure players have succeeded in attracting a young, connected clientele seeking simple, quick, fee-free, fully online solutions.

For Crédit Agricole, digital transformation is a significant opportunity but also a constraint. The group must successfully integrate modern technologies while maintaining its traditional offerings, a difficult balance to strike. The risk is twofold: either losing ground to fully digital banks or diluting its historic model with excessively high costs.

- 📊 Rapid growth of digital clients

- 💻 Implementation of innovative and ergonomic platforms

- ⚖️ Necessity for a dual offer: digital and physical

- 🎯 Precise targeting of young and urban segments

- 🛡️ Enhanced security and digital trust

| Element | Crédit Agricole | Online banks (e.g., ING) |

|---|---|---|

| Number of online clients | Growing but still behind | 1 million for ING Direct |

| Operational costs | High for maintaining the network | Generally low costs |

| Service offerings | Comprehensive, blending physical and digital | Primarily digital |

| Innovation | Progressive but sometimes slow | Fast and often disruptive |

| Customer relations | Strong proximity | Digital focus |

The good news is that Crédit Agricole is beginning to adopt initiatives to modernize its customer relations through improved mobile apps, online advisory services, and partial digitalization of its branches. It remains to be seen whether this hybrid strategy will be enough to keep it competitive against digital banks that are steadily gaining ground.

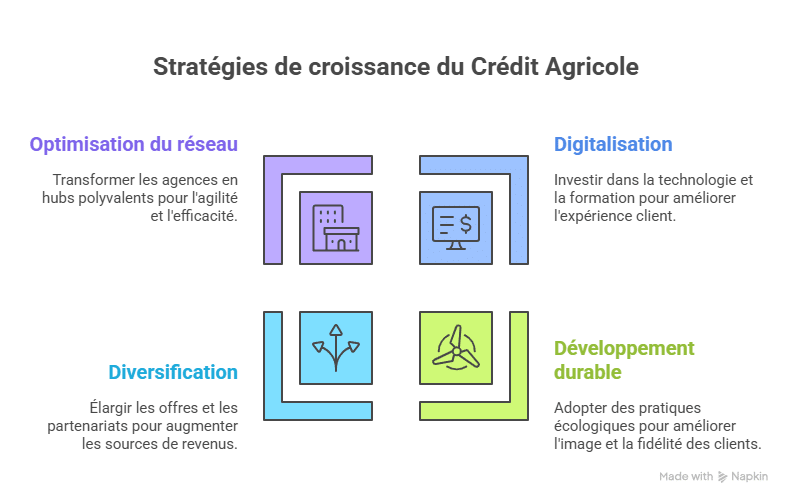

Recommended strategies to strengthen Crédit Agricole’s position in 2025

To stand out in 2025 and continue to be a dominant player in the French banking landscape, Crédit Agricole must leverage its strengths, mitigate its weaknesses, and seize opportunities with agility.

Primarily, heavily investing in digitalization while preserving the advantages of human relations at the core of its services remains crucial. Developing a hybrid banking offer that combines the practicality of digital technology with the warmth of human interaction will play a major strategic role. This involves:

- 📲 Developing high-performing and user-friendly digital tools

- 👩💼 Training staff for digital support

- 🏪 Reorganizing branch networks towards greater versatility and modernity

Second, the group must reinforce its ecological commitments to meet growing customer expectations and improve its long-term image. The focus should be on responsible investments, refusing risky financings, and increasing transparency. This will help differentiate Crédit Agricole in a competitive sector often perceived as cold and impersonal.

Finally, developing strategic international partnerships and diversifying offerings, especially in bancassurance and services for professionals, are fundamental pillars that must not be neglected to continue generating robust revenues.

| Strategic Axis | Key Actions | Target Objectives |

|---|---|---|

| Digitalization | Invest in technologies, train staff, modernize branches | Improve customer experience and reduce costs |

| Sustainable development | Channel financing towards green projects, ecological transparency | Enhance image, foster client loyalty |

| Diversification | Strengthen bancassurance, international partnerships | Expand revenue sources |

| Network optimization | Transform branches into versatile hubs | Enhance agility, reduce fixed costs |

In a market where the competition includes giants like BNP Paribas or Société Générale, but also disruptive players like Hello Bank!, every euro invested in innovation and customer trust will pay off in the long run.

Conclusion

Ultimately, Crédit Agricole remains a cornerstone of the French banking sector thanks to its historical roots, extensive network, and leadership in key segments such as agriculture and bancassurance. However, organizational complexity, ecological criticisms, and increasing pressure from online banks are major challenges to overcome. To remain competitive in 2025, the group will need to accelerate its digitalization, strengthen its commitment to sustainable development, and diversify its activities. The future of Crédit Agricole will depend on its ability to combine heritage and innovation to continue meeting the expectations of a rapidly evolving clientele.

FAQ on SWOT analysis of Crédit Agricole

Because it offers specialized services and has a strong long-standing presence in rural areas, addressing the specific needs of this sector.

Organizational complexity, high costs of the physical network, and ecological impact controversies are urgent challenges to manage.

By developing a high-performing digital offering while maintaining human contact, the group can leverage its physical network as an advantage.

Digitalization, green investments, diversification, and the rise of bancassurance are key drivers.

Intense competition forces the group to innovate constantly, improve responsiveness, and adapt its offerings according to market trends.

In-depth SWOT analysis of Crédit Agricole

Detailed SWOT and PESTLE analysis

Strengths and weaknesses of Crédit Agricole

SWOT analysis of Crédit Agricole by Banque Habitat

Complete case study on Crédit Agricole

📊 Analyses SWOT similaires

📊 Voir aussi : notre hub centralisé de toutes les analyses SWOT & PESTEL (206 études) classées par secteur — Tech, Auto, Mode, Distribution, Finance.

Tu prépares le BTS Assurance ?

Cette analyse SWOT fait partie des thèmes abordés dans les épreuves. Notre E-book de révision couvre l'intégralité du programme en fiches claires et synthétiques.

- 100 % du programme BTS Assurance

- Fiches 1ère et 2ème année

- Créé par un diplômé

- Téléchargement immédiat

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.