The compensatory principle is at the heart of damage insurance operations and constitutes a universal rule governing the relationship between the insurer and the insured. Its purpose is simple but fundamental: to restore the insured to the financial situation they were in prior to the occurrence of a loss, without resulting in unjust impoverishment or abusive enrichment. In other words, the compensation must repair the damage incurred but never exceed its true value.

This principle is based on a logic of contractual justice and economic proportionality, thus avoiding excesses in both directions: insufficient compensation that does not cover the actual loss, or conversely, excessive compensation that transforms insurance into a source of profit.

In practice, it applies to most property insurances (home, car, professional…) and to certain personal insurances, particularly in case of bodily harm. It differs from the lump-sum principle, used in personal insurances (life, death, funeral), where the amount paid is predefined in the contract regardless of the damage suffered.

Understanding the indemnity principle is therefore essential for every insured, as it determines not only the amount of compensation in case of loss but also the conditions under which it is paid. It is an essential key to decipher insurance mechanisms and make informed choices when subscribing to a contract.

Definition of the indemnity principle

According to article L121-1 of the Insurance Code, property insurance is a contract of indemnity. This means that the compensation paid must always correspond to the actual value of the property at the time of the loss, without the possibility of fraudulent overvaluation.

The goal of this principle is to place the insured back into their original financial situation, as if the loss had never occurred, without causing them a unfair loss or a abusive profit.

Practically, this means that a victimized insured must receive a fair compensation covering their damage but never exceeding the objective amount of their loss.

Therefore, this principle guarantees contractual justice between the insurer and the insured, ensuring a sustainable fairness and protecting the market against any voluntary fraud.

Legal basis of the indemnity principle

The indemnity principle finds its source in the Insurance Code, and more specifically in article L121-1. It states that damage insurance is a contract of indemnity, and that the indemnity paid to the insured cannot exceed the actual value of the insured object at the time of the loss.

| 📜 Article | 📌 Key Content |

|---|---|

| L121-1 | The indemnity cannot exceed the actual value of the property at the time of the loss. |

| L121-3 | Fraudulent over-insurance leads to contract nullity and sanctions. |

| L121-4 | Cumulative insurances do not allow double compensation. |

| L121-5 | The insured remains their own insurer for the excess of the declared value. |

This legal basis ensures a legal security and a uniform application of the indemnity principle in France.

Comparison with other insurance principles

The principle of good faith

In insurance, the good faith principle requires the insured to make a sincere declaration of risks at the time of subscription. It complements the indemnity principle by guaranteeing a transparent relationship with the insurer.

The principle of chance

The insurance contract relies on the chance principle, meaning uncertainty regarding the occurrence of the loss. Without chance, a valid contract cannot exist, as risk must be uncertain and unpredictable.

These principles, combined with the indemnity principle, form the fundamental pillars of insurance law.

Objectives of the indemnity principle

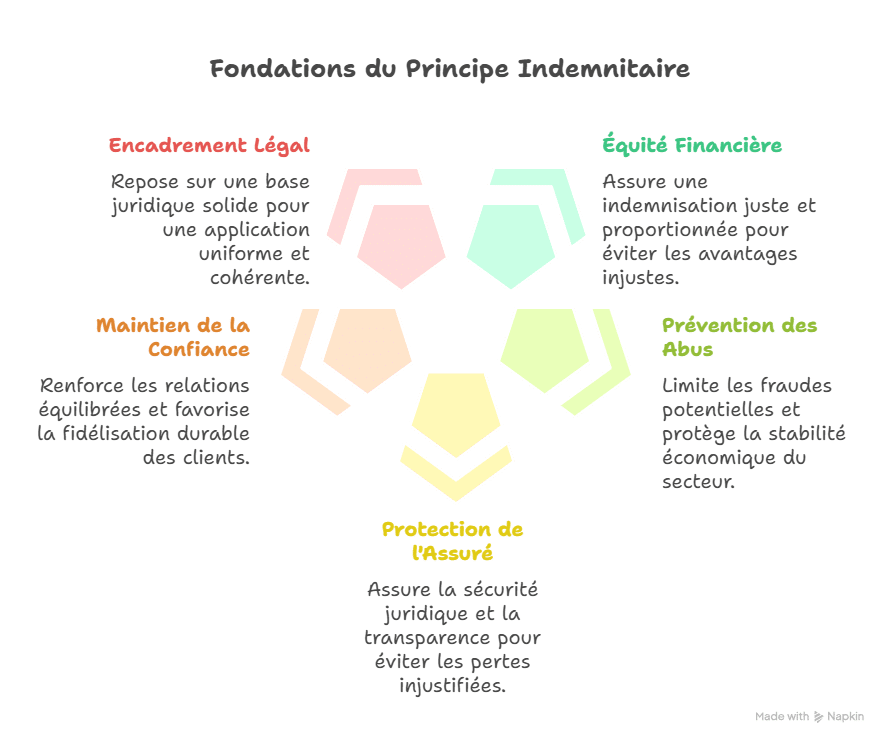

The indemnity principle pursues several key objectives that ensure the stability of the insurance system. It aims to protect insured parties while maintaining a long-term stability for insurance companies.

| 🎯 Goal | 📋 Detailed Explanation |

|---|---|

| Financial fairness | The principle guarantees a fair compensation proportional to the true value of the damage, to avoid any unwarranted advantage or overcompensation. |

| Prevention of abuses | It helps to limit potential frauds, such as false declarations or voluntary over-insurance, thereby protecting the economic stability of the sector. |

| Protection of the insured | It ensures legal security and full transparency in managing claims, preventing the insured from facing an unjust loss. |

| Maintaining trust | By applying this principle, insurers strengthen the balanced relationship with their clients, fostering better long-term loyalty. |

| Legal framework | This principle relies on a solid legal basis, encoded in the Insurance Code, ensuring a uniform and consistent application. |

Each objective demonstrates the desire to preserve a fair justice and a balanced relationship between insurer and insured. In this sense, the indemnity principle acts as a foundational pillar of insurance law, guaranteeing a healthy practice and a more reliable and secure market.

Mechanisms related to the indemnity principle

The indemnity principle hinges on several key mechanisms that regulate compensation and ensure fair and balanced application of insurance rules. These mechanisms aim to protect honest insureds and limit contractual abuses.

Enrichment without cause

The insured cannot receive an indemnity exceeding the actual value of their loss. This mechanism prevents any false declaration or attempt at illegal enrichment.

Example: if a television worth 400 € is destroyed, the insured cannot claim an indemnity of 800 €, even if the initial purchase price was higher. The indemnity must remain proportional and fair.

Over-insurance

Over-insurance occurs when the declared value of a property is greater than its actual value. It can result from good faith (estimation error) or from voluntary fraud. In all cases, the insurer never pays beyond the effective value.

Example: if a house is insured for 300,000 € when its real value is 200,000 €, the compensation will never exceed 200,000 €, even if the premium was calculated on a higher basis.

Cumulative insurances

A policyholder can subscribe to multiple insurance contracts to cover the same property. In such cases, they must inform each relevant company to maintain transparency. However, indemnification remains single and proportional, to prevent double compensation.

Example: a car insured by two different companies will not be eligible for double reimbursement. Insurers share the burden proportionally, and the insured receives only a fair indemnity matching the actual damage.

Practical example of the indemnity principle

The indemnity principle is clearly illustrated through straightforward and concrete examples. These situations help better understand how a fair compensation is calculated based on the real value of the property.

Example 1: smartphone

A smartphone purchased for 1,000 € has a current value of 500 € at the time of the accident. The insurer pays only 500 €, because the indemnity must reflect the real value of the item, not its initial price.

Example 2: car

A new car purchased for 20,000 € suffered an accident three years later. Its market value is estimated at 12,000 € by an expert. The indemnity will be 12,000 €, not 20,000 €, since insurance covers the actual loss incurred and not the purchase price.

Example 3: home

An old piece of furniture insured is destroyed in a fire. While its sentimental value is high, the compensation corresponds only to its market value, estimated at 1,500 €. The insured receives 1,500 €, adhering to the principle of strict proportionality.

Example 4: loan insurance

A borrower loses 50% of their income following an accident and cannot fully repay their mortgage loan. The insurance covers the missing share proportional to the loss, i.e., 500 € if the monthly payment is 1,000 €. The compensation is thus fairly adjusted based on the actual damage.

These examples demonstrate that the indemnity principle guarantees a fair repair of the damage, while preventing the undeserved enrichment of the insured.

Case law examples of the indemnity principle

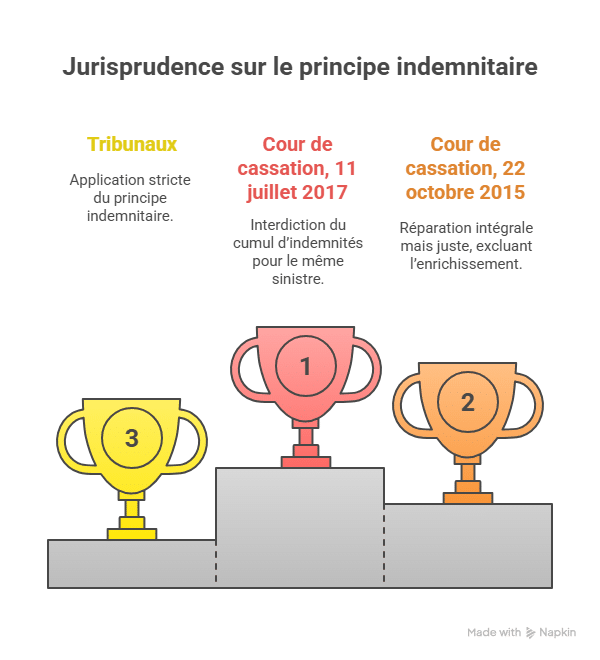

Case law regularly reminds that the insured cannot receive an indemnity exceeding their actual damage.

-

Supreme Court, July 11, 2017: the High Court recalls that cumulative indemnities are forbidden. An insured who has received a sum from one organization cannot seek a new compensation for the same loss.

-

Supreme Court, October 22, 2015: the Court specifies that the compensation must be full but fair, excluding any unjustified enrichment beyond the damage incurred.

These decisions reinforce the idea that the indemnity principle is a binding concept, rigorously enforced by the courts.

Advantages of the indemnity principle

The indemnity principle offers many major advantages for both insurance companies and policyholders. It promotes a system that is more just and more reliable.

1. Fair compensation

It guarantees a fair indemnity that respects financial justice. The insured receives an amount corresponding to the actual value of their property, allowing for a proportional and transparent repair.

2. Protection against abuses

It effectively protects against voluntary abuses and fraudulent declarations. By preventing the insured from claiming an amount higher than the actual loss, it reduces the risks of contractual fraud.

3. Better risk management

It enables insurers to exercise better control over financial risks and ensures long-term stability in contract management. Thanks to this framework, companies can calculate appropriate premiums and avoid excessive unforeseen charges.

4. Strengthened trust

It helps maintain a mutual trust between insurers and insureds, ensuring a balanced and loyal relationship. This transparency fosters client loyalty and enhances the credibility of the insurance market.

These benefits demonstrate that the indemnity principle is a cornerstone of insurance law, combining economic justice and legal protection.

Pas le temps de ficher tout le programme ?

Découvre l'E-book de révision avec 100% des cours de 1ère et 2ème année synthétisés. L'outil indispensable, créé par un diplômé, pour valider ton BTS sans stress.

Découvrir l'E-bookLimitations of the indemnity principle

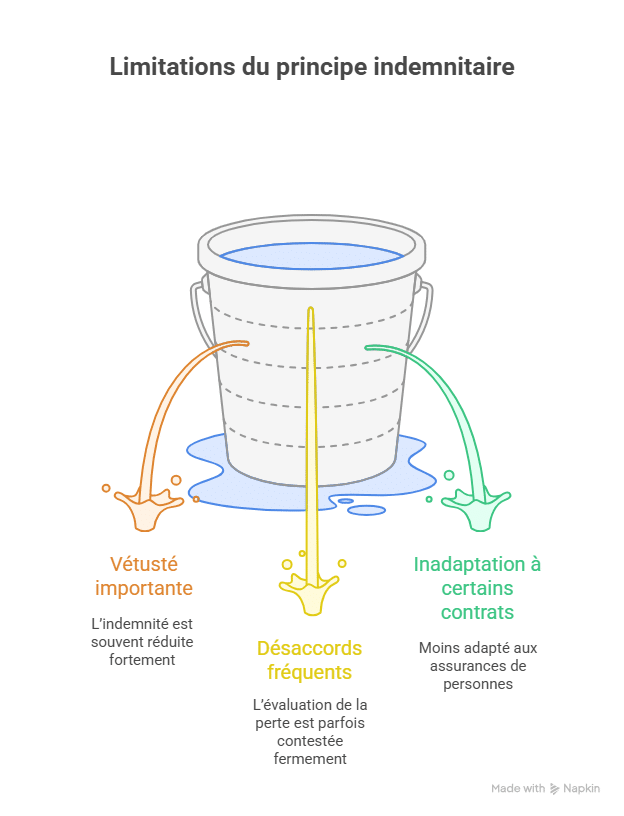

While the indemnity principle guarantees true equity, it nonetheless has certain notable limitations that can cause frustrations and disputes.

| ⚠️ Limitation | 📌 Detailed Consequence |

|---|---|

| Significant wear and tear | The indemnity is often substantially reduced because it accounts for the natural deterioration of the property. This can create a legitimate frustration for the insured, especially if the usage value differs from the initial purchase price. |

| Disagreements often arise | The assessment carried out by the insurer can generate persistent disputes, as the evaluation of the loss is sometimes strongly contested by the insured. These divergences can lead to a lengthy process and tensions with the insurance company. |

| Unsuitability for certain contracts | The principle is less naturally suited for personal insurances, like life or death coverage, which rely on fixed benefits. In those cases, applying the indemnity principle would be unjust or difficult to implement. |

These limitations highlight that the indemnity principle, although a central concept, can sometimes be a source of practical disagreements and requires specific adaptations depending on the insurance type.

Indemnity principle vs. lump sum principle

The indemnity principle and the lump sum principle are two distinct methods of compensation, which follow different logics depending on the nature of the insurance contract. Understanding their specifics allows insured parties to make an informed choice suited to their needs.

| 🏷️ Criterion | ⚖️ Indemnity principle | 💰 Lump sum principle |

|---|---|---|

| Compensation method | Based on the actual value of the property at the time of the loss, without exceeding the amount of the loss. | Based on a fixed amount predefined in the contract, regardless of the actual damage. |

| Relevant fields | Mainly applied to material damages, such as auto, home, or professional insurance. | Mostly used in personal insurances, such as life, death, or funeral insurance. |

| Main advantage | Ensures a fair and just indemnity, proportional to the loss suffered. | Provides a quick, simple, and immediate indemnity, without complex assessment. |

| Main limitation | Can create financial disputes related to assessment disagreements or wear and tear effects. | May lead to actual undercoverage if the fixed sum does not match the precise cost of the damage. |

| Concrete example | A car bought for 20,000 € has a market value of 12,000 € at the time of an accident. The indemnity will be 12,000 €, reflecting the actual value. | A funeral insurance provides a guaranteed capital of 5,000 €. Upon the insured’s death, the beneficiaries receive this fixed amount, regardless of the actual funeral costs. |

Application based on insurance types

The indemnity principle does not apply identically across all branches of insurance.

Home insurance

In case of fire or water damage, the compensation covers the actual value of the furniture or damaged goods. Companies apply a deduction linked to wear and tear.

Car insurance

In case of total loss, compensation is based on the market value of the vehicle, not the original purchase price. Some contracts include a new value option to offset this depreciation.

Loan insurance

The indemnity principle covers only the income loss of the insured. Compensation is proportional and can never generate an additional profit.

Professional insurance

Within a company, this principle applies to all material damages (machines, buildings). The indemnity must cover the actual loss, calculated on an expert assessment.

Claims settlement procedure

Applying the indemnity principle follows a well-defined process.

| 🔎 Step | 📋 Description |

|---|---|

| 1. Reporting the loss | The insured informs their insurer promptly after the event (legal deadline of 5 days). |

| 2. Damage assessment | An expert appointed by the insurer assesses the actual value of the damaged property. |

| 3. Calculate compensation | The amount is determined based on the use value, wear and tear, or the new value as per the contract. |

| 4. Payment of compensation | The insurer pays within a regulatory deadline, respecting the proportionality principle. |

This process guarantees total transparency and legal fairness for all parties involved.

Particular cases and exceptions

The indemnity principle is not universal and has specific exceptions.

-

Life insurance: the fixed amount corresponds to the guaranteed capital, regardless of the damage incurred.

-

Death or funeral insurance: the indemnity is a set sum in advance within the contract.

-

Agreed value: some contracts specify a fixed value at the time of subscribing, notably for works of art or collector vehicles.

These exceptions rely on a logic of pre-established fixed amount, rather than proportional repair.

FAQ on the indemnity principle

What is the indemnity principle in insurance?

The indemnity principle means that the amount paid by the insurer corresponds solely to the actual value of the loss incurred, without generating profit for the insured.

How does it differ from the lump sum principle?

The indemnity principle is based on the property’s value at the time of the loss, whereas the lump sum principle provides a fixed, known sum upfront, regardless of damage.

Does the indemnity principle apply to all insurances?

No, it mainly pertains to damage insurances (auto, home, professional). Personal insurances (life, death, funeral) often follow the lump sum approach.

How is the indemnity calculated?

The indemnity is calculated based on the use value of the property, taking into account wear and tear and the conditions specified in the insurance contract.

Conclusion

The indemnity principle is a foundational rule in insurance law, defining precisely how claims should be calculated. It is based on an economic fairness that prevents any form of unjust enrichment or excessive loss for the insured.

This principle provides durable protection to individuals and businesses because it ensures each indemnity is fair and proportional to the actual damage. In this way, it strengthens the mutual trust between insurance companies and their clients, while stabilizing the insurance market.

Even though some practical limitations exist, notably related to the wear and tear of goods or disagreements during expert assessments, the indemnity principle remains the cornerstone of damage insurance. Its implementation helps preserve contractual justice and legal security essential to the system’s durability.

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.