In Summary

| 📌 Section | 📝 Detailed Content |

|---|---|

| 🧾 Definition | The IDA is a mechanism for direct compensation that allows an insured not responsible for an accident to be compensated by their own insurance company, without waiting for settlement between insurers via the IRSA agreement. |

| 👥 Involved Parties | Three actors are involved: the insured (victim), their insurer, and the responsible third party or their insurer. Each plays a specific role in the compensation and inter-company recourse procedure. |

| 📜 Application Conditions | For the IDA to apply, the following are necessary: an IDa clause in the insurance contract, a clearly established responsibility of the third party (by amicable report, report, witnesses), and material damages covered by the policy. |

| 🚗 Practical Case | Example: Marie, hit by a distracted driver, provides a clear report to her insurer. Thanks to the IDA clause, she is compensated in less than a week without further procedures, while insurers settle among themselves. |

| 🚀 Main Advantages | ✅ Speed: compensation delays often reduced to a few days. ✅ Simplicity: fewer forms, streamlined procedures. ✅ Efficiency: automated assessments, reduced administrative costs, fewer errors. |

| ⚠️ Limitations | ❌ Not applicable if responsibility is uncertain or shared. ❌ Unsuitable for complex or bodily injury claims. ❌ Indemnifications sometimes capped according to IRSA scales. ❌ Possible exclusion if the clause is not included in the contract. |

| 📝 Common Mistakes to Avoid | – Incorrectly filled report 📝 → vague responsibility. – Late declaration ⏰ → possible refusal. – Absence of IDA clause 📄. – Shared or uncertain responsibility ⚖️. – Lack of knowledge of caps 💰. |

| 🧭 IDA Procedure | 1️⃣ Report of damage + amicable report → 2️⃣ Exchange of info with insurer → 3️⃣ Damage assessment (often automated) → 4️⃣ Rapid payment of compensation → 5️⃣ Financial settlement between insurers via IRSA. |

| 🤝 Relationship between insurers | IDa is accompanied by mechanisms of compensation, co-insurance, and subrogation. The insured’s insurer first compensates, then recovers the amount from the responsible party’s insurer. |

| 🌐 Evolution and Future Perspectives | 📌 Legislation: reforms to promote IDA. 🤖 Technology: AI, automation, more precise processing. 🏡 Extension: possible adaptations to other fields (housing, health, travel). |

| ❓ FAQ | – Difference between IRSA / IDA? – Average compensation times? – Possibility of contestation? – Applicability to bodily injury? – Tiers without insurance? Answer: FGAO. |

When an accident occurs, the steps to obtain compensation can quickly become a real administrative journey. To prevent non-responsible drivers from waiting weeks before being compensated, French insurers have implemented a simple and quick mechanism: the Direct Compensation of Insureds (IDA). Framed by the IRSA convention, this system allows the insured to be reimbursed directly by their own company, without waiting for responsibility to be settled between insurers. This system, which has become a reference in auto insurance, relies on clear rules and offers considerable advantages, while also having some limits to be aware of.

Once the application of the IRSA convention, insurers can set up the Direct Compensation of Insureds (IDA). The IDA recourse is an indemnification mechanism in the insurance field. It allows policyholders to receive direct compensation from their insurance company, without complex administrative procedures. The IDA offers significant benefits, such as speed and efficiency of compensation, as well as reducing administrative steps. However, its application is subject to certain limits and requirements related to third-party responsibility. Moreover, the IDA affects the amount of compensation.

How the IDA Recourse Works

Explanation of the IDA concept

The IDA recourse is based on a fundamental principle: the insurer of the insured directly covers damages suffered by their policyholder, without waiting for civil responsibility procedures with the responsible third party to conclude. This means that the insured can receive compensation from their insurer even before the third party’s responsibility is determined.

Involved Parties: the insured, the insurer, and the responsible third party

Several actors are involved in the IDA recourse:

- The insured: The person who has taken out an insurance policy to protect against certain risks. In case of a claim, they are the beneficiary of the compensation provided by their insurance contract.

- The insurer: The insurance company that issued the policy contracted by the insured. Their role is to assess damages suffered by the insured and to pay appropriate compensation according to the terms and conditions of the policy.

- The responsible third party: The person or entity considered responsible for the claim and damages suffered by the insured. This could be another driver in a traffic accident, a property owner in case of material damage, etc.

Conditions Required for the IDA Recourse

The IDA recourse is subject to certain conditions to be applicable:

- Insurance contract: The insured must have taken out an insurance policy that includes a specific clause allowing the IDA recourse. This clause specifies the conditions and limits of the direct indemnity to the insurer.

- Clear responsibility of the third party: Clear evidence of the third party’s responsibility in the incident must exist. This can be established through an amicable report, police report, testimonies, etc.

- Damages covered by insurance: The damages suffered by the insured must be covered by the guarantees of their insurance contract. Specific coverage conditions are defined in the insurance policy.

Practical Example

Concrete example of the application of the IDA

Let’s imagine the following situation:

Marie is driving peacefully when another driver, distracted, hits her at an intersection. Her vehicle is damaged at the rear. An amicable report is immediately completed on the spot. Both parties sign the document, and the responsibility of the third party is clearly indicated in the designated box.

The next day, Marie contacts her insurer and sends them the report. Thanks to the IDa clause included in her contract, her insurer initiates the direct compensation procedure. In less than a week, damage assessment is completed, and compensation is deposited into her bank account.

Meanwhile, Marie’s insurer arranges direct payment with the responsible driver’s insurer within the framework of the IRSA convention. Marie does not have to wait or follow up with the other insurer. She benefits from a rapid, predictable, and administratively simple compensation.

This case perfectly illustrates the goal of the IDA: protecting the non-responsible insured and simplifying interactions between companies.

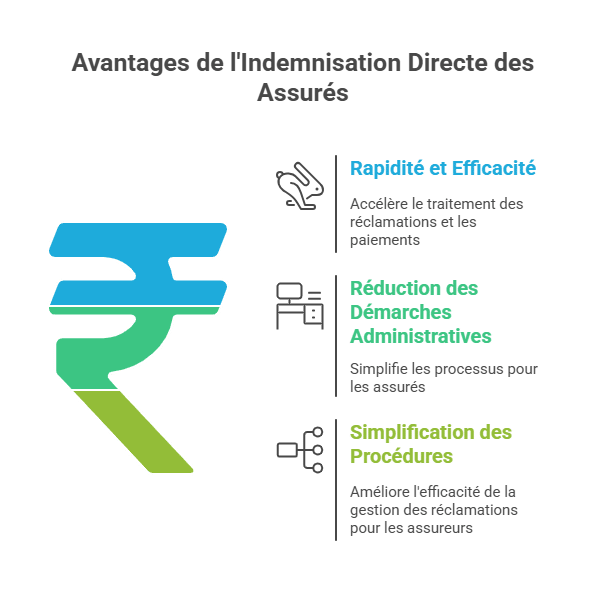

Advantages of the IDA Recourse

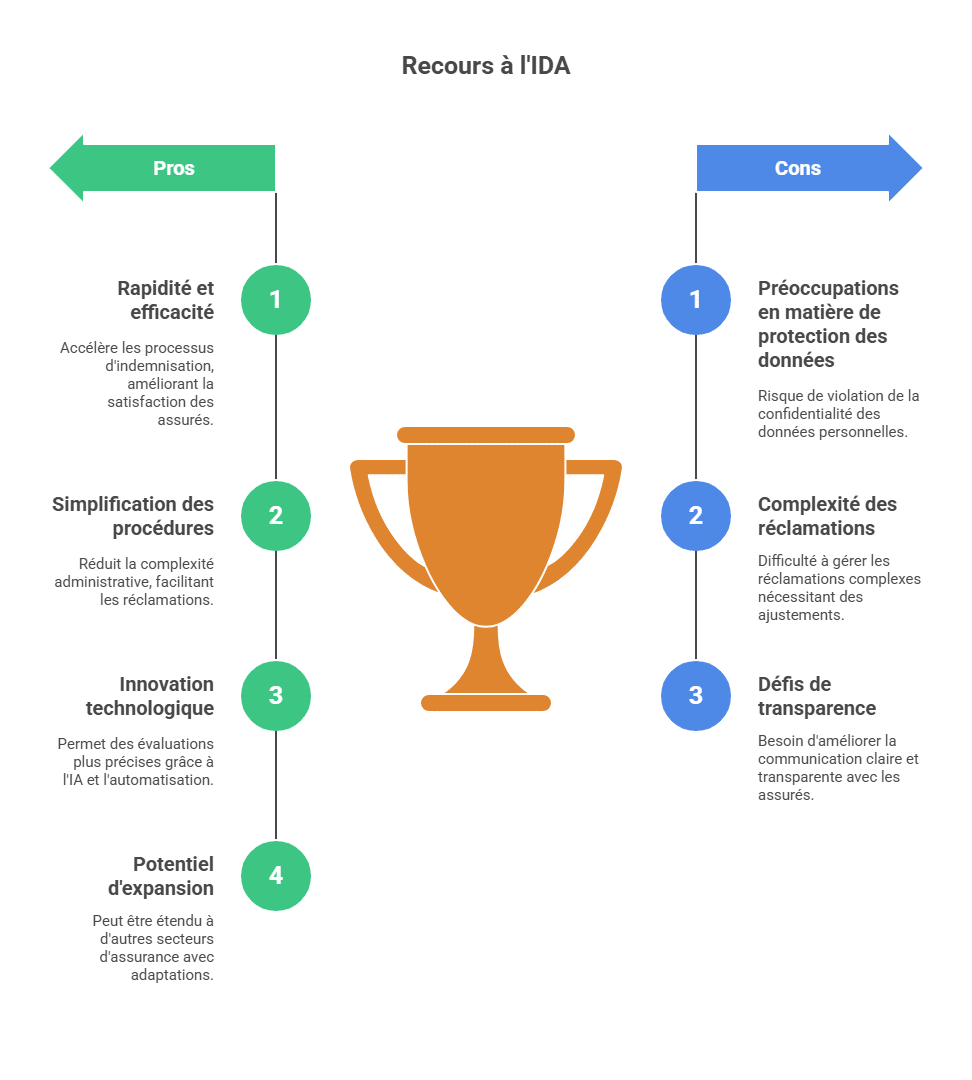

Speed and efficiency of compensation

Using the Direct Compensation of Insureds (IDA) offers multiple benefits in terms of speed and efficiency. Thanks to the IDA, claim processing and payout procedures can be automated, significantly reducing delays. Insurers can use advanced computer systems to quickly evaluate claims and make payments without extensive human intervention. This accelerates the overall process and ensures faster compensation for policyholders.

Reduction of administrative steps for the insured

The IDA also helps to reduce administrative steps for policyholders. Instead of filling out numerous forms and providing detailed documentation, insured individuals can benefit from a simplified procedure. Necessary information for the claim evaluation can be obtained directly from appropriate sources such as healthcare providers, police services, or auto repair shops. This spares policyholders from gathering and submitting these documents, greatly simplifying the process and lowering administrative burden.

Simplification for the insurer

The IDA also streamlines procedures for insurers. By automating certain claim steps, insurers can reduce administrative costs and improve claim management efficiency. Computer systems can be used to gather and analyze data for claim evaluation, enabling quicker and more consistent decision-making. Additionally, automation reduces human error and fraud risks, which is advantageous for insurers.

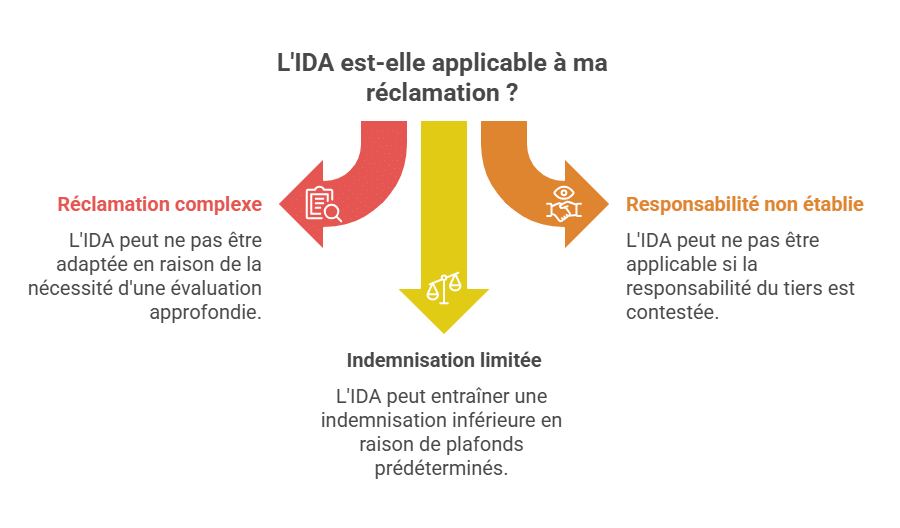

Limitations and Application Criteria of the IDA

Cases where the IDA is not applicable

The Direct Compensation of Insureds (IDA) can have limitations and may not be applicable in all situations. For example, in complex or contentious claims requiring detailed assessment, the IDA may not be suitable. Moreover, if the necessary information for claim evaluation is not available automatically or if additional evidence is needed, the IDA recourse can be limited. In such cases, traditional claim procedures involving more extensive human intervention may be necessary.

Requirements related to the responsibility of the third party

The IDA is generally applicable where the third party’s responsibility is clearly established. If the responsibility of the other involved party is not determined or is disputed, the IDA may be limited. The IDA is often used in situations where the third party’s responsibility is admitted or clearly proven without ambiguity, which facilitates direct indemnity processing.

Impact on the indemnity amount

Using the IDA can influence the amount of compensation. In some cases, the IDA may be associated with predetermined caps or scales for calculating indemnities. This could mean that the insured receives a lower amount than what might be obtained through traditional claim processing, where a more individualized assessment could be made. It is important to understand the specific calculation criteria applied within the IDA framework and to consider potential impacts on the compensation amount.

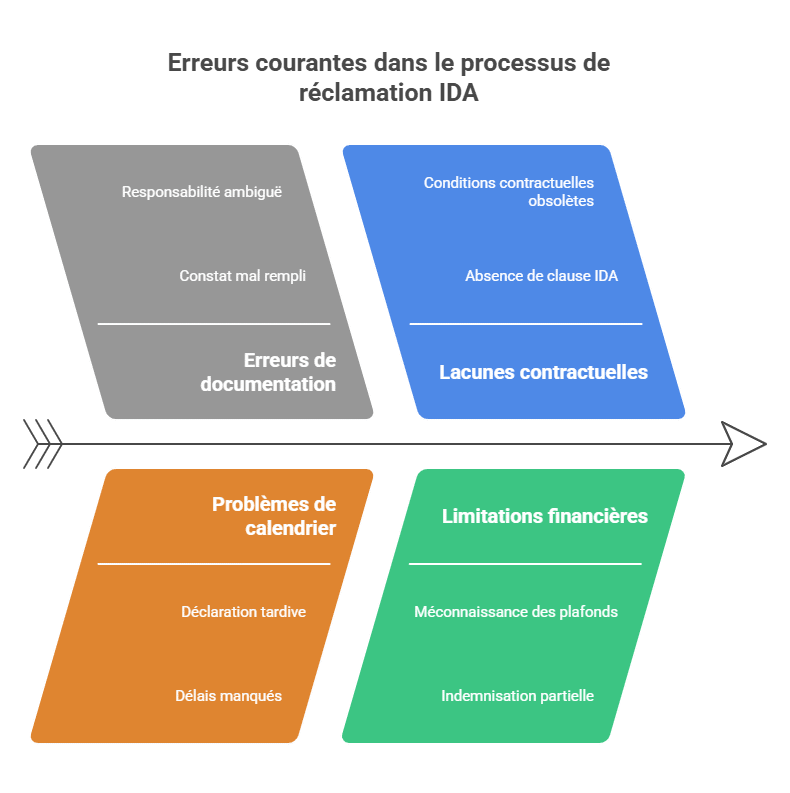

Common Mistakes and Points of Vigilance

Frequent mistakes to avoid with the IDA recourse

Even though the mechanism is designed to simplify life for policyholders, some errors can delay or even compromise compensation:

-

❌ Incorrectly filled report: an unchecked box or poorly expressed responsibility can lead the case into a gray area, causing delays.

-

⏰ Late declaration: most contracts impose a 5-business-day deadline to report the claim. Missed this deadline, the insurer may refuse compensation.

-

📄 Absence of IDA clause in the contract: some older or specific contracts do not include this clause. Without it, the IDA procedure cannot be applied.

-

⚖️ Shared or uncertain responsibility: the IDA requires responsibility to be clearly established. If the report is ambiguous, a more traditional procedure follows.

-

💰 Unawareness of limits: some IRSA scales cap indemnization for material damages. The insured may receive only part of the compensation if they do not verify these limits.

Understanding these points well helps avoid unpleasant surprises and optimizes claims management in case of a dispute.

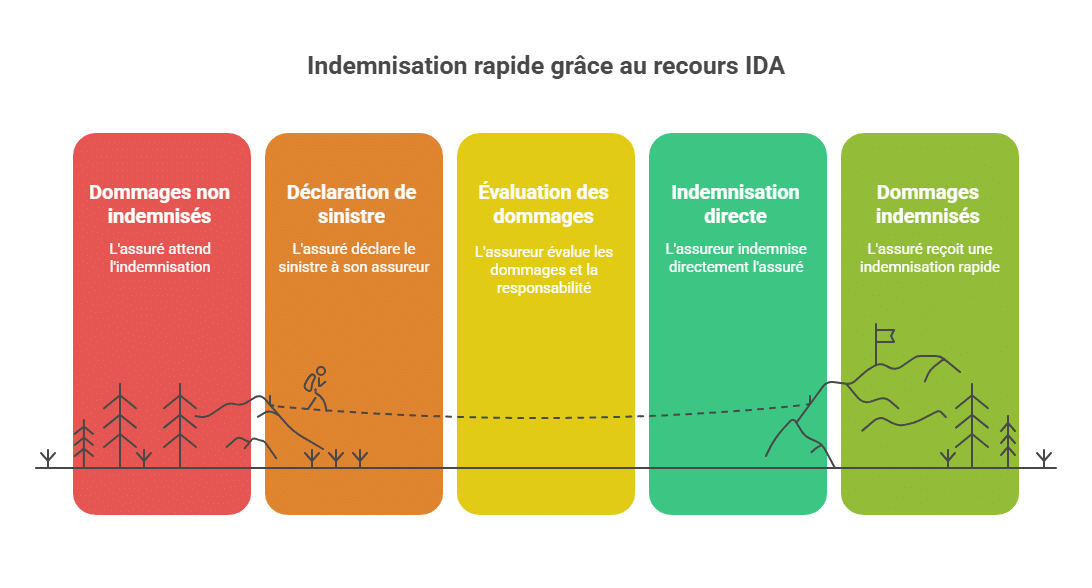

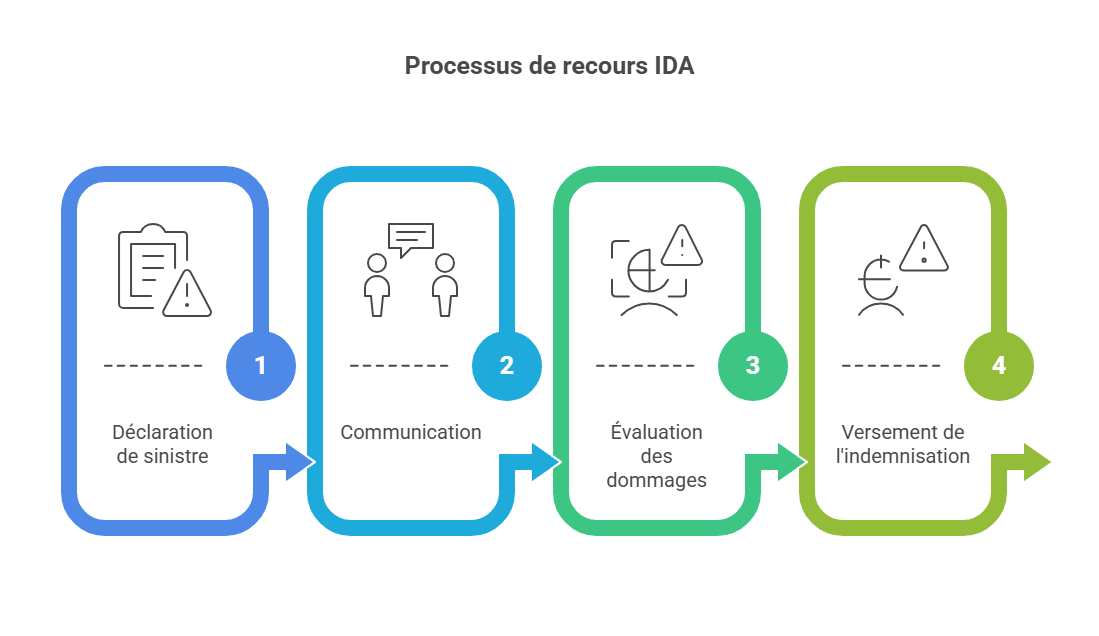

IDA Recourse Procedure

Declaration of damage and amicable report

The process of using the Direct Compensation of Insureds (IDA) typically starts with the insured reporting the incident to their insurer. The insured must promptly inform their insurer of the event, providing all relevant details such as date, location, and circumstances of the accident. In the case of a car accident, an amicable report can be filled out by the involved parties to document the facts and damages.

Communication between the insured and their insurer

Once the claim is reported, the insured and their insurer communicate to exchange additional information and clarify the claim details. This communication can be via phone, email, or other agreed methods.

Damage assessment and evaluation

Within the IDA framework, damage assessment can be performed automatically or semi-automatically. Insurers may use advanced computer systems to evaluate damages based on pre-established data and models. This may include images, videos, reference databases, and evaluation algorithms. The goal is to determine the amount of compensation based on predefined criteria.

Payment of compensation

Once damage evaluation is complete, the insurer proceeds with paying the compensation to the insured. Under the IDA, this process can be automated, allowing for faster payment. Compensation can be made via bank transfer or other agreed payment methods.

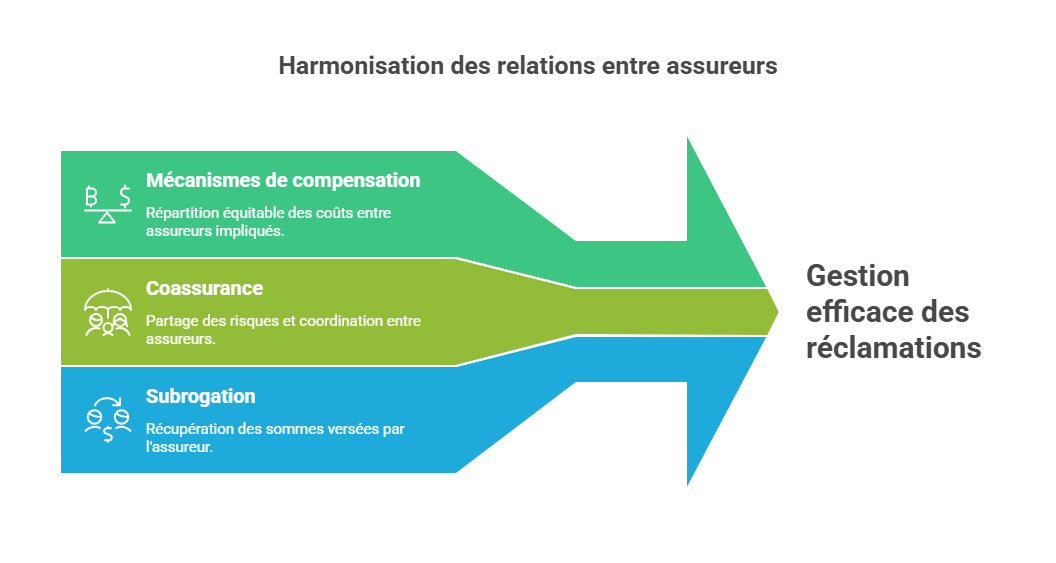

Recourse IDA and the Relationship Between Insurers

Mechanisms of compensation between insurers

In the context of IDA recourse, mechanisms of compensation may exist, especially when multiple insurance companies are involved in the same incident. When an insured benefits from the IDA, their insurer may engage in financial exchanges with the insurers of third parties involved to settle the indemnities. These compensation mechanisms help to distribute costs fairly among concerned insurers, according to respective responsibilities.

Co-insurance and subrogation

Co-insurance and subrogation are concepts related to the insurer relationships under the IDA:

The co-insurance occurs when multiple insurers share the risk of the same claim. For instance, in auto insurance, the insured might be covered by a primary policy and a supplementary policy issued by different insurance companies. When a claim is made, insurers can coordinate and use the IDA to simplify the indemnification process and split costs among themselves.

Subrogation involves transferring the rights and claims of a policyholder to their insurer after being compensated. When the insurer pays the insured under the IDA, they can exercise subrogation rights to recover the sums paid from the responsible third party. This allows the insurer to recover part or all of the indemnity paid to the insured, reducing overall costs.

These mechanisms facilitate claims management between insurers and enable proper sharing of responsibilities and costs.

Evolution and Future Perspectives of the IDA Recourse

Recent legislative developments

The use of the IDA has seen recent legislative changes in certain countries. Regulatory authorities and lawmakers have recognized the potential benefits of the IDA in terms of speed, efficiency, and procedural simplification. As a result, reforms have been introduced to promote and facilitate the use of the IDA. These may include adopting specific laws or regulations to encourage and regulate IDA use in sectors such as auto insurance.

Challenges and improvement prospects

Despite its advantages, the IDA still faces challenges and avenues for improvement. Major issues include:

- Data protection: Employing the IDA involves collecting and processing sensitive personal data. Ensuring data confidentiality, security, and compliance with privacy laws is crucial.

- Complexity of claims: The IDA is more suitable for straightforward, well-defined claims. For complex claims, such as those involving serious injuries or significant disputes, adjustments are needed to ensure fair and adequate assessment.

- Transparency and communication: Improving transparency and communication between insurers and policyholders is essential. Policyholders should be clearly informed about processes, criteria, and potential impacts on compensation amounts.

- Technological innovation: Rapid technological developments offer new opportunities for enhancing the IDA’s effectiveness. Use of AI, machine learning, and advanced automation can enable more accurate, faster claim evaluations and better data management.

- Extension to other insurance branches: Although commonly associated with auto insurance, the IDA’s potential adaptation to other fields (housing, health, travel) exists. This requires sector-specific adjustments and developments.

IDa Recourse in Summary

In conclusion, the IDA represents a significant advancement in insurance, offering a quick and effective solution for policyholder compensation. However, ongoing efforts are necessary to overcome existing limits and maximize benefits, ensuring a positive experience for insured parties and efficient claims management.

Conclusion

In summary, the IDA recourse is a major milestone in managing non-responsible material claims. Through this mechanism, policyholders benefit from a fast indemnification, a simplified process, and better visibility on reimbursement times.

However, to fully benefit from these advantages, it is essential to carefully fill out the amicable report, declare the claim promptly, and have a good understanding of the terms of your insurance contract. The IDA is based on specific rules: clear responsibility, an appropriate contractual clause, and defined compensation caps.

In the future, integrating AI, digitalizing declarations, and potentially expanding the mechanism to other insurance branches could further strengthen its efficiency.

❓ Frequently Asked Questions about the IDA Recourse

What is the difference between IRSA and IDA?

IRSA is the convention signed between insurance companies to organize the distribution of indemnities and simplify mutual recourse. In contrast, the IDA is the direct indemnity mechanism applied to non-responsible insured parties.

How long does an indemnification via IDA typically take?

On average, straightforward cases are processed within 5 to 10 working days. This can depend on the speed of declaration, clarity of the report, and the insurer’s management tools.

Can I dispute the compensation amount paid?

Yes. If you think the amount is insufficient, you can request a counter-expertise or contact an insurance mediator.

Does the IDA apply to bodily injury claims?

No. It only covers material damages not caused by responsibility. Bodily injury claims follow a different, often longer, procedural route, usually judicial.

What if the third party is uninsured?

In such cases, the IDA does not apply. The policyholder can turn to the Fonds de Garantie des Assurances Obligatoires (FGAO), which intervenes to compensate victims of accidents caused by uninsured or unknown vehicles.

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.