- Politics and regulation play a crucial role in the banking landscape in 2025.

- Impact of interest rates on borrowing

- Reduction of profit margins

- Strategies to offset revenue loss

- Increasing consumer demand for digital services

- Growing importance of social and ESG values

- Trust and reputation of banking institutions

- Integration of artificial intelligence into services

- Growing use of blockchains for secure transactions

- Development of intuitive mobile applications

- Implementation of green initiatives within investment portfolios

- Commitment to rapid and effective decarbonization

- Assessment of environmental impact of financing activities

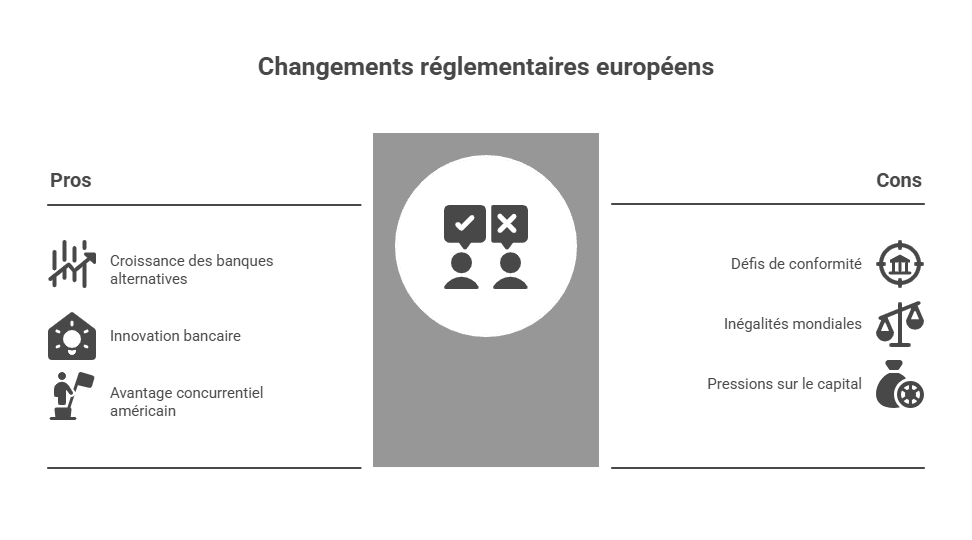

- Evolution of European regulatory framework

- Challenges for banks facing common policies

- Opportunities for growth in alternative banking

In Summary

| PESTEL Factor | Key Challenges 2025 |

|---|---|

| Political & Regulatory | Implementation of Basel IV → increased capital costs, enhanced oversight by the ECB, geopolitical tensions influencing regulation. |

| Economic | Global economic slowdown, net interest margins under pressure, fluctuating interest rates (2.5% → 3%), partnerships to diversify income sources. |

| Social | Growing customer expectations for digital, ethical, and inclusive services, rise of ESG values, trust/reputation at the core. |

| Technological | Digital transformation: AI (personalization, loyalty), blockchain (security, speed), mobile applications (simplicity, accessibility). |

| Environmental | Pressure from climate change, net-zero carbon neutrality by 2050, reduction in fossil fuel finance, growth in green investments. |

| Legal | Strengthening of data protection and cybersecurity standards, adaptation to diverging regulations Europe/USA, strict monitoring of ESG obligations. |

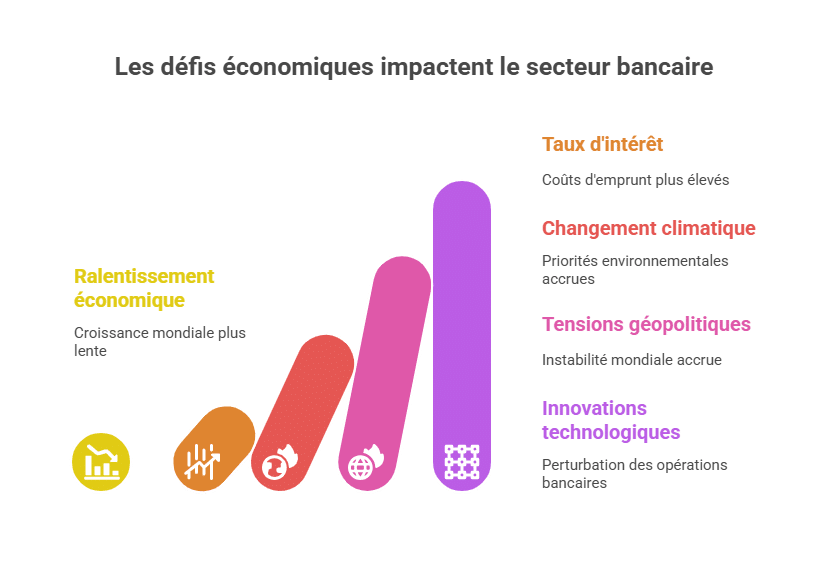

At the dawn of 2025, the banking sector faces a complex set of challenges that redefine its practices and strategic orientations. The slowdown of the global economy, coupled with rising interest rates, suggests a challenging environment for banks. Additionally, issues related to climate change and geopolitical tensions require constant reevaluation of priorities. In this context, technological innovations significantly influence traditional banking operations. How can each sector actor, whether BNP Paribas, Société Générale, or Crédit Agricole, navigate this new economic reality? This article offers an in-depth analysis of the PESTEL environment of the banking sector in 2025, to highlight challenges and future perspectives.

- Analysis of political and regulatory challenges

- State of economic forces and the impact of interest rates

- Social and behavioral challenges amidst a changing landscape

- Emerging technologies and digital transformation

- Environmental impact and climate change

- Assessment of regulatory trends in Europe

- Opportunities and threats for banking actors

- Future perspectives and strategic direction

Analysis of Political and Regulatory Challenges

Politics and regulation play a crucial role in the banking landscape in 2025. Varied regulatory regimes between Europe and the United States influence banks’ competitiveness. The framework of Basel IV, expected to be fully implemented by 2033, appears as a major concern for institutions like Crédit Agricole, Société Générale, and La Banque Postale. Political tensions, especially those generated by recent elections, could also bring about significant regulatory changes.

At the European level, the ECB could maintain a strict stance, which could seriously affect how European investment banks operate. Discussions currently underway on regulations regarding capital incorporation and liquidity indicate that enhanced oversight might become standard.

| Regulation | Impact on institutions | Examples |

|---|---|---|

| Basel IV | Increased capital costs | BNP Paribas, Crédit Agricole |

| Sector consolidation | Reduce competition | LCL, Société Générale |

| Better risk management | Portfolio optimization | HSBC France, Nova Bank |

Major Political Challenges in 2025

Beyond Basel IV, several global policies also impact the sector. The revision of monetary policies by many central banks, aiming to stabilize the economy but also driven by increasing geopolitical tensions, forces banks to adapt quickly.

Regulatory Impact on Competitiveness

To remain competitive, banks need to develop robust strategies to manage these regulations. For example, Boursorama Bank and Fortuneo, digital players, could benefit from this complexity by offering more flexible services tailored to consumer needs. Traditional institutions, meanwhile, must reconsider their approach to maintain a strong market position.

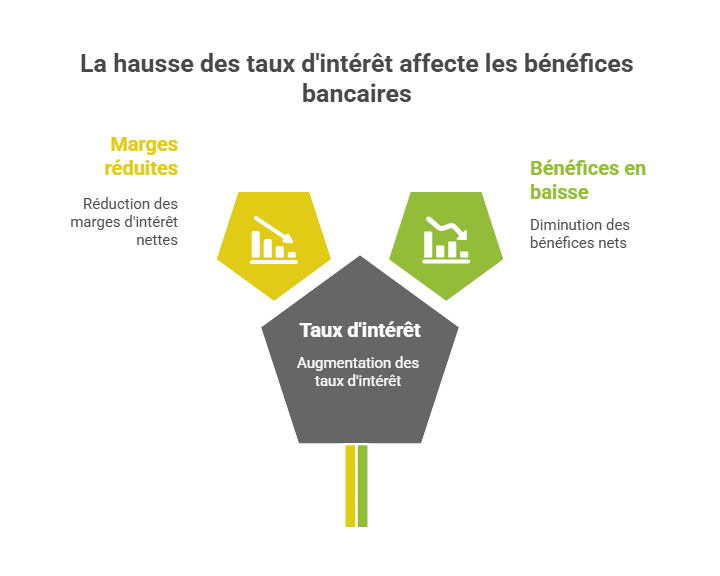

State of Economic Forces and the Impact of Interest Rates

The global economic slowdown is exerting pressure on the European banking sector. Forecasts indicate that growth could remain modest, making revenue generation even more challenging. Rising interest rates could also affect net interest margins, crucial for banks. A 50 basis point decrease could reduce these revenues by 3%, additionally impacting net profits dramatically.

- Impact of interest rates on borrowing

- Reduction of profit margins

- Strategies to offset revenue loss

| Year | Estimated Interest Rate (%) | Impact on Profits |

|---|---|---|

| 2023 | 2.50 | Stable |

| 2024 | 3.00 | Decreasing |

| 2025 | 2.50 | Slightly rebounds |

Actor Adaptations in the Sector

In response to this situation, banks must develop new ways of thinking. Partnerships and collaborations with technology companies could prove to be effective ways to diversify revenue streams and refine cost structures. Crédit Mutuel and HSBC France are investing, for example, in digitizing their services to stay ahead in the competitive arena.

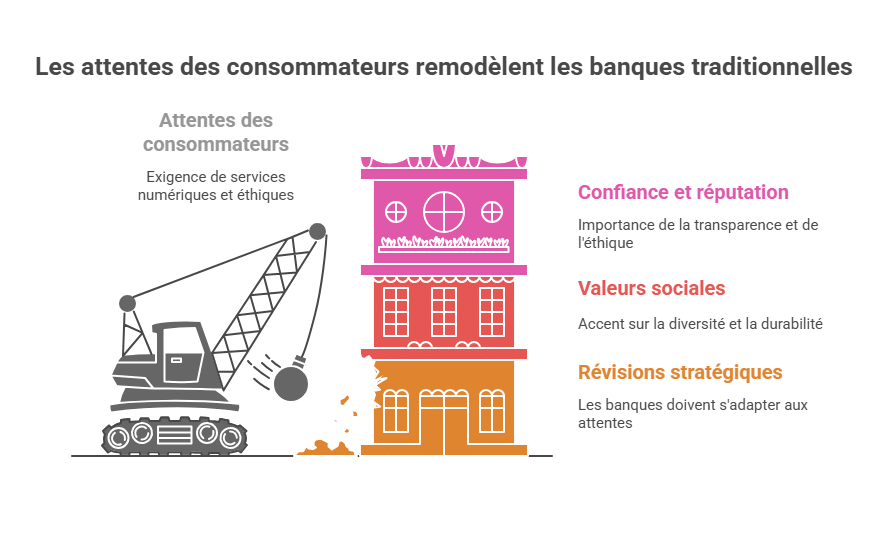

Social and Behavioral Challenges Amidst a Changing Landscape

In 2025, consumers are changing their approach to banking services. The rise of fintechs and the digitization of services prompt traditional banks to rethink their operational models. Growing customer expectations for ethical, transparent, and easily accessible services force these institutions to develop tailored products.

- Increasing consumer demand for digital services

- Growing importance of social and ESG values

- Trust and reputation of banking institutions

Customer Expectations in 2025

Customers, especially younger generations, seek complete transparency in banking services. Boursorama Bank, for instance, has adapted quickly by offering products tailored to the specific needs of generations Z and Y. AI-based services also enable adequate personalization, attracting young borrowers.

Social Challenges and Impacts on Traditional Banks

Banks such as La Banque Postale and LCL need to align with these expectations and consider strategic revisions. Social issues related to diversity, inclusion, and sustainability are becoming key elements in attracting new clients.

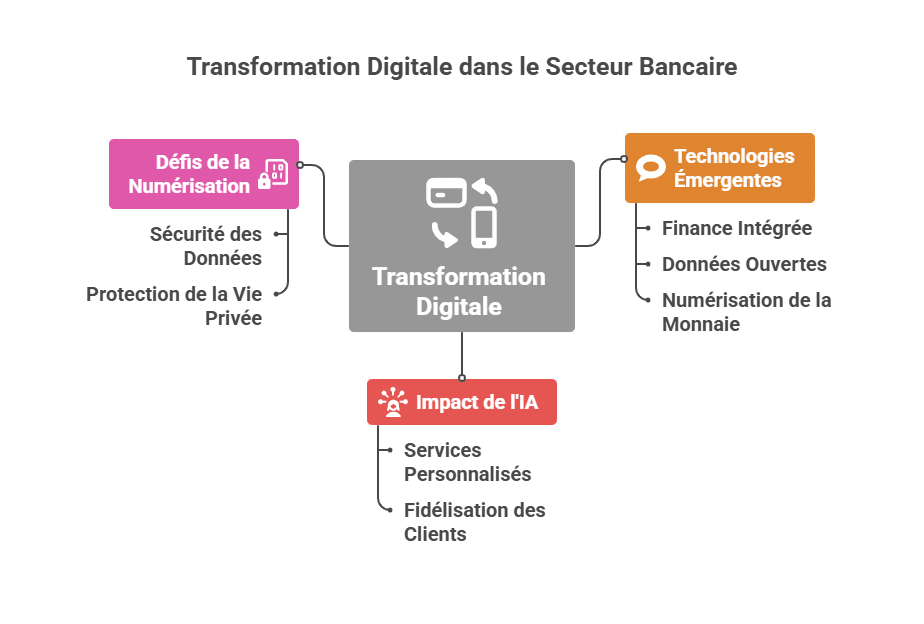

Emerging Technologies and Digital Transformation

Technological innovations continue to reshape the banking landscape. Innovations such as integrated finance, open data, and digital currency redefine client-bank interactions. Many institutions, including Crédit Agricole and Nova Bank, are investing heavily in these technologies to optimize client interactions and strengthen their market position.

- Integration of artificial intelligence into services

- Growing use of blockchains for secure transactions

- Development of intuitive mobile applications

| Technology | Potential Impact | Participating Banks |

|---|---|---|

| AI | Enhancement of customer experience | HSBC France, Crédit Mutuel |

| Blockchain | Rapid and secure transactions | BNP Paribas, Nova Bank |

| Apps | Simplification of banking operations | Boursorama Bank, Fortuneo |

The Impact of AI on Banking Operations

AI tools enable banks to offer personalized services that increase customer loyalty. The conflicting demands of technology and traditional practices cause a market repositioning. Banks must all engage in these transformations to stay ahead of the competition.

Challenges of Digitization

Despite these advances, digitization also presents challenges. Data security and customer privacy protection have become paramount in a context where cybercrime is increasing. Société Générale and Crédit Agricole are investing in cybersecurity solutions to address these concerns.

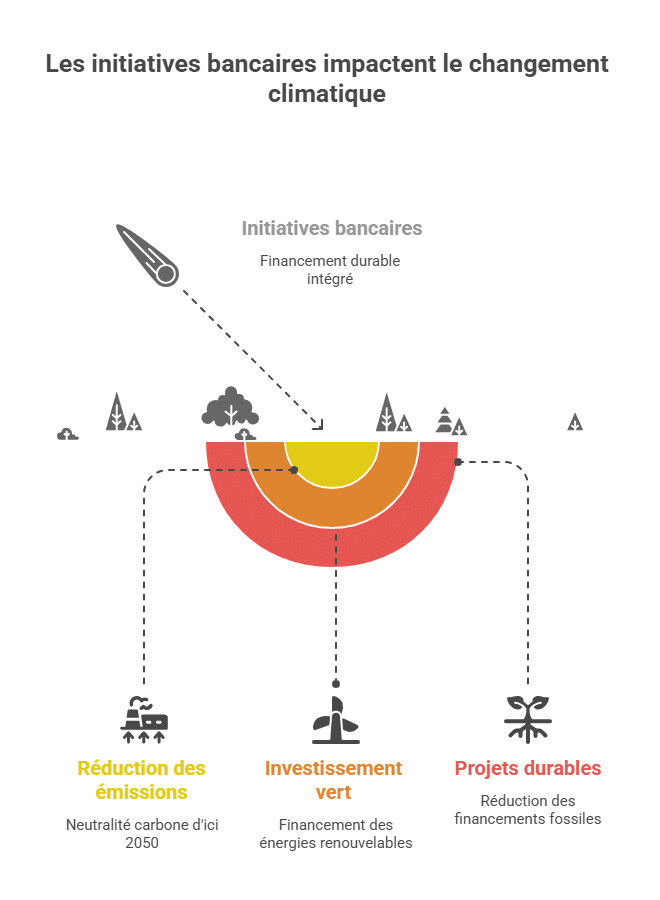

Environmental Impact and Climate Change

Within the context of climate issues, banks are compelled to rethink their strategies in response to the climate emergency. Understanding how institutions like BNP Paribas and HSBC France integrate sustainability goals into their operations is essential. The Net Zero Banking Alliance is a prominent example of this awareness.

- Implementation of green initiatives within investment portfolios

- Commitment to rapid and effective decarbonization

- Assessment of environmental impact of financing activities

| Environmental Goal | Participating Banks | Projected Impact |

|---|---|---|

| Carbon neutrality by 2050 | BNP Paribas, Crédit Agricole | Reduction of CO2 emissions |

| Financing renewable energy | HSBC France, Nova Bank | Increase in green investments |

| Reducing fossil fuel financing | Fortuneo, La Banque Postale | Growth of sustainable projects |

Bank Initiatives Addressing Climate Change

Banks are increasingly aware of their environmental responsibilities. By integrating sustainable finance into their core strategies, they can not only meet customer expectations but also enhance their reputation and market position.

Risks of Slow Transition

Time is pressing, and delays in implementing these strategies can have adverse consequences. Studies show that banks with irrelevant emission reduction goals jeopardize not only their reputation but also their long-term viability.

Assessment of Regulatory Trends in Europe

Amid debates on regulation accounting for divergent European and American market contexts, each actor must navigate skillfully. Discussions on simplifying IPO processes could also affect banks such as Société Générale and Crédit Agricole.

- Evolution of European regulatory framework

- Challenges for banks facing common policies

- Opportunities for growth in alternative banking

Expected Changes with Basel IV

The implementation of Basel IV could significantly transform the regulatory landscape. For American banks, the lack of full adoption of these rules might give them a competitive advantage, potentially widening global competitive disparities.

Impacts of Regulation on the Banking Sector

To withstand these capital requirements, banks must innovate and adjust their cost structures. Established players like Crédit Agricole and BNP Paribas need to continue exploring innovative solutions to secure their positions in this evolving environment.

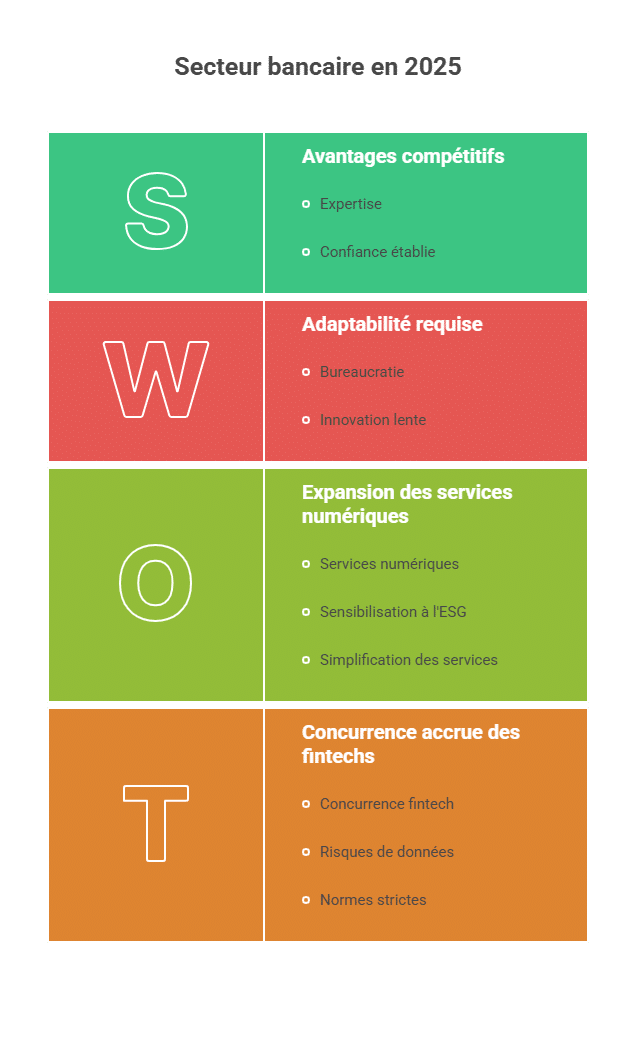

Opportunities and Threats for Banking Sector Players

The banking sector in 2025 is a landscape filled with opportunities and risks. While banks such as Crédit Mutuel and HSBC France explore new market segments, they also face significant challenges. Evolving consumer expectations, the rising role of fintechs, and the importance of social engagement are crucial elements to consider.

- Competitive advantages of traditional players over fintechs

- The importance of innovation to stay relevant

- Threats of a consumer trust crisis

| Opportunity | Threat | Affected Banks |

|---|---|---|

| Expansion into digital services | Increased competition from fintechs | Crédit Agricole, Boursorama Bank |

| Growing awareness of ESG | Strict regulatory standards | BNP Paribas, La Banque Postale |

| Simplification of services | Cybersecurity and data risks | Société Générale, LCL |

How Are Banks Responding to Threats?

The key for banks will be adaptability. For institutions like Crédit Mutuel and HSBC France, diversification alone will not suffice; they must also develop innovative and improved solutions to remain relevant.

Future Perspectives and Strategic Alignment

The prospect of institutional renewal will be a necessary condition for banks to survive and thrive. With increased focus on innovation and social engagement, the potential for transformation in the banking sector is enormous. Committing to a sustainable path could not only strengthen long-term viability but also increase consumer confidence in their financial institutions.

FAQ

What are the main challenges facing the banking sector in 2025?

The banking sector must manage rising interest rates, increasingly strict regulations, environmental concerns, and growing customer expectations for digitized services.

How do technologies influence the banking sector?

Technologies such as artificial intelligence and blockchain facilitate the digital transformation of the banking sector, enabling secure transactions and enhanced customer experiences.

Which are the main banks involved in the move towards sustainable practices?

Institutions like BNP Paribas, HSBC France, and Crédit Agricole are implementing decarbonization strategies and financing renewable energy projects.

What is the importance of regulation for the banking sector in 2025?

Regulation is crucial as it determines banks’ competitiveness and their ability to manage economic crises.

How can banks remain competitive against fintechs?

To stay competitive, banks must constantly innovate, diversify their services, and adapt to new customer expectations to maintain relevance in the market.

📊 Voir aussi : notre hub centralisé de toutes les analyses SWOT & PESTEL (206 études) classées par secteur — Tech, Auto, Mode, Distribution, Finance.

Tu prépares le BTS Assurance ?

Cette analyse PESTEL fait partie des thèmes abordés dans les épreuves. Notre E-book de révision couvre l'intégralité du programme en fiches claires et synthétiques.

- 100 % du programme BTS Assurance

- Fiches 1ère et 2ème année

- Créé par un diplômé

- Téléchargement immédiat

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.