Arnaques aux abonnements : astuces pour stopper les paiements récurrents par carte bancaire

In summary

| Section | Summary |

|---|---|

| Understanding the origins of subscription scams | Introductory offers (€1 / free trial) conceal a recurring subscription. Vague labels and foreign companies complicate identification and cancellation. |

| Operation of recurring card payments | Card authorization is often “permanent”: the merchant can periodically withdraw funds without new agreement. Cryptic descriptions (e.g., Cblm, Straceo…) hinder tracking. |

| Identifying and decoding recurring payments | Set up “subscriptions” alerts, monitor small recurring amounts (€3–15), recognize periodicity and obscure names, cross-check dates/amounts with actual purchases. |

| Steps to stop hidden subscriptions | Identify the creditor, log into the customer account, cancel online or via mail/email, keep proof of cancellation, verify cessation on bank statements in following weeks. |

| Blocking payments: advantages / limits | Bank opposition = immediate stop but total card blocking and replacement (fees/delay). Useful as a last resort or if the merchant is unreachable. |

| Recourse and refunds (chargeback) | Activate a chargeback through the issuer (Visa/Mastercard) in case of non-compliant or unauthorized service. Gather evidence (T&Cs, emails, screenshots) and respect deadlines. |

| Preventive tips | Read the T&Cs, avoid overly enticing offers, verify website security/HTTPS, use alert tools, regularly check statements, and react quickly to the slightest doubt. |

| Prioritize alternatives to cards | Prefer SEPA direct debit for subscriptions: revocable mandate, better legal framework, more control than often non-revocable card authorization. |

| FAQ (Key points) | What to do in case of unknown withdrawal? Identify → cancel → if unsuccessful, oppose/chargeback. Opposition blocks the card. Notify: T&Cs, SEPA, tracking tools. |

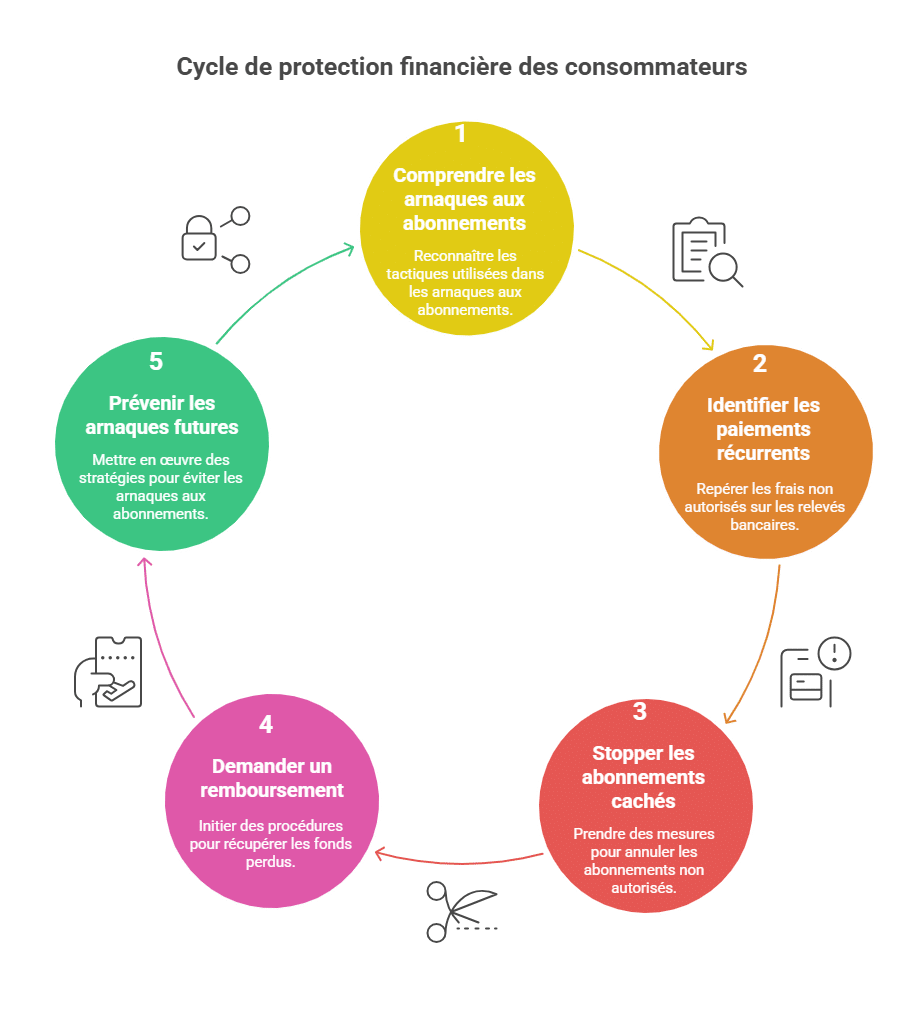

The hidden subscriptions behind a single payment or supposedly free trial pose an increasing threat to consumers. Each month, unexpected withdrawals appear on bank statements, often difficult to identify and stop. This situation can weaken personal finances, cause frustration, and raise questions about online transaction security. Understanding the mechanisms behind these scams and mastering the steps to stop these recurring payments is essential to ensure true financial transparency and effective subscription management.

Faced with such reality, it is crucial to arm oneself with good reflexes and suitable tools to counteract these unwanted withdrawals. Here, discover clear methods, practical advice, and regulatory solutions to control your subscriptions, activate effective subscription assistance, and ensure stronger bank security against these traps.

- Understanding the origins of card subscription scams

- Identifying and decoding recurring payments on your bank statements

- Steps to stop hidden or fraudulent subscriptions

- Blocking payments: advantages, limits, and impacts

- Recourse and procedures to get a refund

- Practical tips to prevent subscription scams

- Prioritize safer alternatives to cards

- FAQ: common questions about recurring payments and scams

Understanding the origin of card subscription scams

Seemingly harmless but recurring withdrawals can quickly become an unforeseen financial burden. These payments are not always the result of outright fraud, but often stem from a misunderstanding or lack of knowledge about the purchase conditions. Many are tempted by a low-cost offer, sometimes a single product like a €1 smartphone or a supposedly free service, only to discover a hidden subscription afterward.

This mechanism typically relies on an attractive call offer with a very low initial cost, followed by periodic billing that can be difficult to stop. For example, purchasing a free sample or paying shipping fees for an apparent offer can mask the creation of a subscription. This is observed in cases involving coffee machines, drones, or services like fortune-telling and dating.

Operation of recurring card payments

When subscribing to a service with payment by credit card, you give a recurring authorization often described as “permanent.” This authorization, in strict technical terms, is unrevokeable, which complicates the consumer’s task of stopping payments on their own. Practically, the provider can thus withdraw sums regularly without further consent.

The label of payments on bank statements is often intentionally vague or cryptic, preventing clear identification of the recipient. Partial names, acronyms, or non-explicit codes are common. For example, subscriptions appear under companies such as Cblm, Straceo, Medialump, or Reducpriv.com. These cryptic descriptions make immediate action difficult due to lack of precise information.

- Low-cost offers masking hidden subscriptions

- Subscriptions difficult to cancel due to unclear identification

- Recurring payment authorization given once and for all

- Bank labels often non-explicit or foreign

| Type of offer | Example | Nature of the subscription | Cancellation difficulty |

|---|---|---|---|

| Product with low initial cost | Smartphone €1 + shipping fees | Hidden monthly subscription of €5–10 | Difficult identification on bank statement |

| Free trial followed by subscription | Online fortune-telling service | Automatic withdrawal without warning | No clear contact for cancellation |

| Services related to games or lotteries | Online games with subscription | Monthly recurring payment | Vague label and foreign company based abroad |

Identify and decode recurring payments on your bank statements using an active subscription alert

The first step to regaining control of your finances is to set up a subscription alert. This involves regularly monitoring your account statements to detect any suspicious or unknown withdrawals. Today, many banks and apps offer tools to automatically categorize payments and flag active subscriptions.

Deciphering obscure bank operation labels is essential to prevent subscription management from becoming a headache. Platforms like ComparateurBanque provide practical sheets to recognize suspicious names and offer concrete help for the procedures.

How to detect a masked subscription?

To detect a subscription that was not consented to knowingly, here are some easy steps to adopt:

- Monitor low-amount withdrawals, often between €3 and €15.

- Look for payments appearing at regular intervals, monthly or quarterly.

- Note incomplete names or cryptic descriptions in the bank details.

- Compare dates and amounts with your actual purchases to identify inconsistencies.

| Suspicious payment indicators | Meaning | Practical advice |

|---|---|---|

| Low and recurring amount | Possible hidden subscription | Examine initial purchase conditions |

| Incomplete or cryptic label | Identification difficulty | Use billing management help sites |

| Withdrawals from foreign sites | Potential increased risk | Check the legitimacy and location of the site |

| Absence of a single withdrawal matching a purchase | Unrecognized subscription | Contact customer service or the bank |

For more information on fighting hidden subscriptions, the Boursorama Finance resource offers useful insights on this topic.

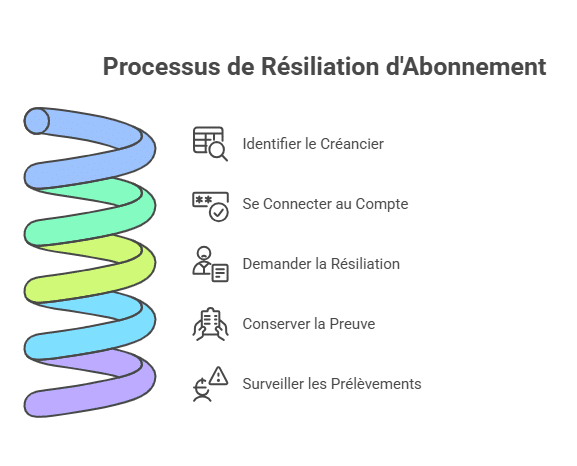

The effective steps to stop a hidden or fraudulent subscription

Once the recurring payment is identified, the priority is to attempt to cancel the subscription with the creditor. This easy cancellation is possible if the contact is findable and if the company offers a clear way to end the services.

Most often, you need to access a personal space on the website, deactivate the subscription, or even send a written request by email or registered mail. This step can be time-consuming but remains the first course of action.

- Precisely identify the provider or site originating the withdrawals

- Log into your customer account and look for the “cancel” or “unsubscribe” option

- Send an email or letter if unsubscribe is not visible online

- Keep proof of the cancellation request

- Check subsequent charges on your statement a few weeks after the request

| Cancellation steps | Recommended actions | Points of attention |

|---|---|---|

| Identifying the creditor | Analyze banking details and search online | Some names may differ from the commercial name |

| Logging into the customer account | Use the email address and passwords associated | Beware of non-secure sites |

| Request for cancellation | Online form or registered mail | Keep a written record in case of dispute |

| Monitoring withdrawals | Monthly control of the bank statement | React quickly if there is a new withdrawal |

For more in-depth information, the UFC Que Choisir Albertville website provides a comprehensive guide to fighting recurring payments.

Blocking payments: a radical solution against abusive recurring payments

If direct cancellation with the provider proves impossible or ineffective, the ultimate solution is to block the payments through your bank. This action blocks all future transactions with the associated card. It is part of bank security and is a powerful lever against unwanted withdrawals.

However, this option is not without consequences. Blocking the card completely requires ordering a new card, often with renewal fees. Some banks may offer a goodwill gesture if the cause is clearly an anti-fraud subscription.

- Immediately contact your bank to report the issue

- Request the procedure for blocking the card

- Prepare to receive a new card with a waiting period

- Consult your bank to negotiate possible compensation

- Activate payment tracking to monitor any future attempts

| Advantages of opposition | Disadvantages |

|---|---|

| Immediate stop of unwanted withdrawals | Total blocking of the bank card |

| Enhanced protection against fraudulent subscriptions | Possible fees for issuing a new card |

| Improved security | Temporary interactions limited with some services |

More detailed explanations are available on the MoneyVox site, providing a better understanding of this process and its implications.

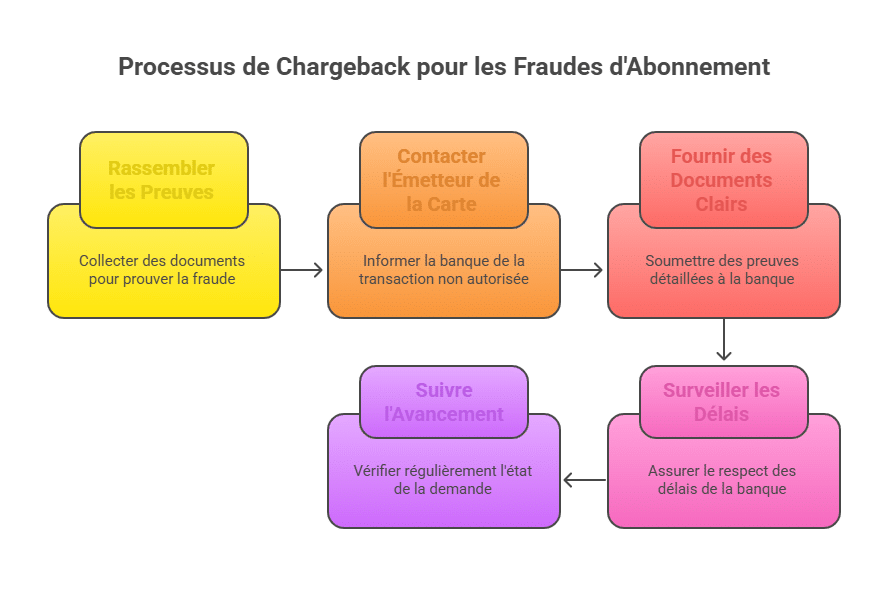

Recourse and steps to get a refund after a scam subscription

Obtaining a refund after being incorrectly charged or unknowingly withdrawn remains a significant challenge. The so-called chargeback procedure, which allows canceling an unauthorized or non-compliant payment, is rarely used because it is little known by consumers and banks. Yet, it is recognized by Visa and Mastercard in case of proven commercial misconduct such as non-delivery or non-conforming service.

The European Consumer Centre recommends engaging this process if you are victims of unjustified recurring payments, especially when the website is foreign and hard to reach. It is important to gather all evidence (screenshots, emails, sales conditions) before contacting the card issuer.

- Gather proof of non-consent or misunderstanding

- Contact the card issuer to activate the chargeback procedure

- Provide clear and precise documents to the bank

- Be vigilant about the time limits imposed for this request

- Follow the progress of the case diligently

| Conditions for a successful chargeback | Necessary actions | Limitations |

|---|---|---|

| Proof of non-consented subscription | Provide contractual documents and exchanges | The bank may refuse for various reasons |

| Service not conforming with the order | Describe precisely the defect or absence | Complex process in case of disguised fraud |

| Request within legal deadlines | Respect the time limits set by the issuer | Often ignored or poorly applied procedure |

Practical guides are available on PaiementCarte.com to help better understand and implement these steps.

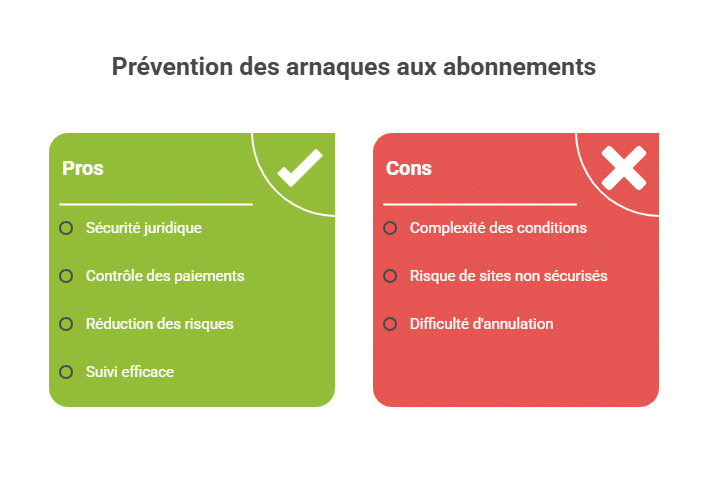

Practical tips to prevent and avoid hidden subscription scams

The best defense against these traps is prevention. Vigilance when entering bank details online is essential. Carefully reading the terms and conditions must be systematic to avoid being caught off guard by clauses at the bottom of a page, indicating automatic subscriptions.

Experts recommend avoiding card payments for subscriptions on poorly identified sites or those using unrecognized payment interfaces, called “exotic.” Using SEPA direct debit mandates offers better control since the customer can revoke the mandate at any time.

- Never enter your banking details without verifying the site’s security

- Avoid overly enticing or unknown offers

- Read the purchase and subscription conditions carefully

- Favor SEPA direct debit for recurring payments

- Regularly check your bank statements and report suspicious withdrawals immediately

| Preventive actions | Associated benefits |

|---|---|

| Careful reading of contractual conditions | Enhanced legal security |

| Preference for SEPA direct debit | Easier cancellation and better control |

| Rigorous verification of site identity | Reduced risk of scams |

| Use of alert tools for subscriptions | Effective and quick monitoring of payments |

For further details on these tips, the MoneyVox site offers tailored recommendations for modern consumers.

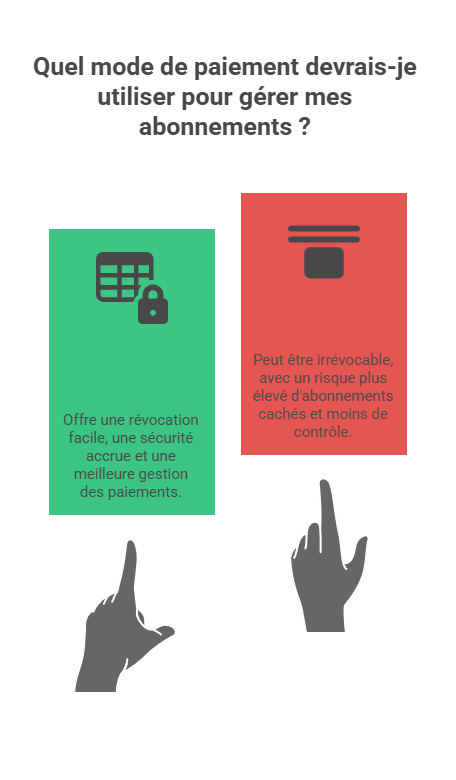

Prioritize direct debit payments for controlled subscription management

The choice of payment method heavily influences the ability to manage and control a subscription. SEPA bank direct debit allows periodic payments while leaving the consumer the power to revoke the mandate at any time, without necessarily stopping the associated bank card.

This option promotes financial transparency and reduces risks associated with fraudulent use of the bank card. In case of dispute, claiming an abusive SEPA direct debit is easier and better regulated legally.

- SEPA direct debit: possibility to revoke the mandate at any moment

- Bank card: authorization often non-revocable

- Prefer serious and transparent sites using these methods

- Avoid unknown or suspicious payment interfaces

- Regularly monitor your bills and active subscriptions

| Criterion | SEPA direct debit | Bank card |

|---|---|---|

| Possibility of cancellation | Easy revocation of mandate | Authorization often non-revocable |

| Security | Better legally regulated | Higher risk of hidden subscription |

| Management | Easy tracking of withdrawals | Less control over recurring payments |

| Bank intervention | Possible blocking in case of abuse | Opposition usually the only solution |

Official reference information can be consulted on the Aide BTS Assurance site, which covers the modalities and advantages of SEPA direct debit.

FAQ: common questions about subscription scams and recurring card payments

| Question | Answer |

|---|---|

| What should I do if I find an unknown withdrawal on my account? | Quickly identify the creditor and attempt to cancel the subscription via their customer service. If impossible, contact your bank to block the payment. |

| Does opposition to the bank card cancel all my subscriptions? | Yes, it blocks all future payments on that card but requires ordering a new card, often with fees. |

| Can I get a refund in case of hidden subscription? | The chargeback process can allow a refund, but it is often complex and not always accepted. |

| How to avoid being tricked during an online purchase? | Carefully read the subscription conditions, favor SEPA direct debit, and verify the site’s reliability. |

| Are there tools to track my subscriptions and payments? | Yes, many banking apps and comparison sites offer subscription alerts and simplified payment tracking. |

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.