Summary

What is a municipal mutual?

A municipal mutual is a health complementary scheme implemented by a town or an intercommunal authority to provide its residents with accessible and affordable health protection. Unlike standard mutuals, these schemes are specifically negotiated to meet the particular needs of local populations. They rely on the principle of membership pooling, meaning that collective groupings of residents enable obtaining preferential rates from insurance providers.

An adapted solution for various profiles

Municipal mutuals mainly target people without mandatory mutual insurance, often excluded from employer-provided collective schemes. Among the most affected profiles are:

- Retirees: Often facing fixed income, they benefit from guarantees tailored to age-related needs, such as hospitalization or dental care.

- Self-employed workers: Without a collective contract, they can enjoy advantageous rates and customized guarantees, often eligible under the Madelin law.

- Students: With limited budgets, they find in municipal mutuals an economical solution to cover medical expenses.

- Job seekers and micro-entrepreneurs: These groups, particularly vulnerable to health uncertainties, can access basic essential guarantees.

A solidarity and accessible scheme

One of the key strengths of municipal mutuals is their universal accessibility. They are open to all residents of the municipality, regardless of income, age, or medical condition. This means:

- No health questionnaire: No discrimination based on medical history.

- No age limit: Seniors can join easily.

- No income conditions: Equal access for all residents, whether employed or not.

📊 Comparison between municipal mutual and individual mutual

Choosing between a municipal mutual or an individual mutual depends on your personal situation. Each option offers specific advantages and limitations to consider. The following table summarizes the main differences 👇

| Criteria | Municipal mutual | Individual mutual |

|---|---|---|

| 💰 Price | Often 30 to 60% cheaper thanks to collective negotiation | Generally higher unless targeted promotional offers |

| 📋 Membership conditions | Open to all, no medical questionnaire or age limits | Often subject to conditions, especially health status |

| 🧩 Personalization | Standardized guarantees for most needs | Contract tailored to personal profile and specific needs |

| 🏢 Management | Simplified via town hall or CCAS | Directly with insurer, sometimes more complex |

In summary, the municipal mutual is best suited for those seeking a cost-effective and simple solution, while the individual mutual allows for maximum customization for specific needs.

A partnership between municipalities and insurers

To establish a municipal mutual, town halls act as mediators between residents and insurers. By negotiating contracts tailored to local needs, they enable residents to benefit from comprehensive guarantees while significantly reducing costs. This also strengthens the social bond within the community, creating a supportive environment where everyone can access essential care.

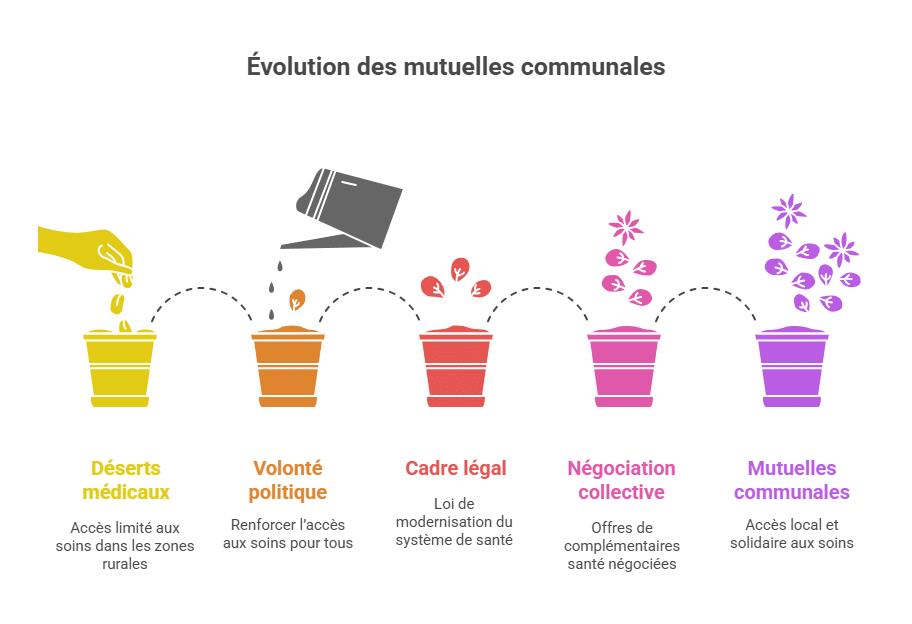

🧠 Historical and legal framework of municipal mutuals

The idea of municipal mutuals originated from a political desire to enhance access to healthcare for all, especially in small towns. This scheme developed during the 2010s, following initial experiments carried out in rural communities facing medical deserts.

The legal framework is based on the law of January 31, 2014, relating to the modernization of the health system, which encouraged local authorities to take an active role in social protection. This law allows local entities to collectively negotiate health insurance offers with insurers, while membership remains optional.

Over the years, numerous circulars and practical guides have been published to assist elected officials in implementing these schemes. Today, more than 3,000 municipalities have established a municipal mutual, demonstrating the effectiveness of this local and solidarity-based approach.

How municipal mutuals operate

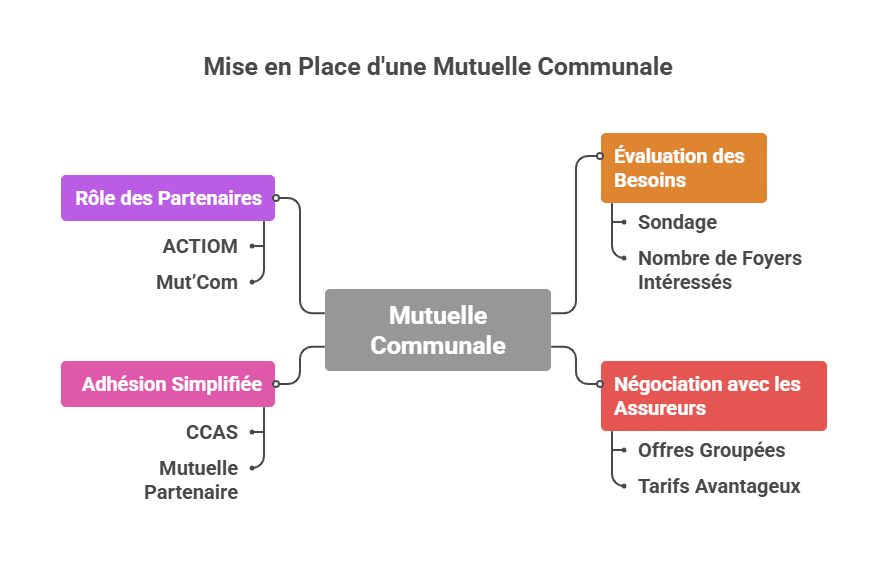

The process of establishing a municipal mutual follows a series of key steps. These ensure effective organization and a proper match between residents’ needs and the guarantees offered by partner mutuals.

Key implementation steps

- Needs assessment: The first step involves conducting a survey among residents. This surveys helps determine the number of interested households and their specific needs (routine care, optical, dental, etc.). The higher the potential membership, the stronger the negotiation leverage for the town hall.

- Negotiation with insurers: Once needs are identified, the town hall or inter-municipal authority contacts insurance providers to negotiate group offers. The goal is to obtain the best guarantees while maintaining advantageous rates for residents. This includes comparing proposals and selecting the most suitable offer.

- Simplified membership: After finalizing the offer, residents can join the municipal mutual via the Centre Communal d’Action Sociale (CCAS) or directly through the partner mutual. The process is voluntary, non-compulsory, and characterized by the absence of complex conditions, such as medical questionnaires or age limits.

| Steps | Description |

|---|---|

| 🗳️ Survey | Identify residents’ needs. |

| 🤝 Negotiation | Secure attractive rates through group effect. |

| 📋 Simplified membership | Make signing up easier without restrictive conditions. |

The role of partners in the scheme

To assist municipalities in establishing a mutual, specialized associations intervene to simplify procedures and maximize benefits for residents. Among them:

- ACTIOM: One of the most active associations, with over 1,700 partner municipalities. ACTIOM helps negotiate guarantees and rates while ensuring administrative follow-up.

- Mut’Com: Offers tailored support, emphasizing solidarity and purchasing power of residents.

These partners play a key role in:

- Facilitating negotiations with insurers.

- Providing expertise in health and pooling.

- Ensuring simplified management for the municipality and residents.

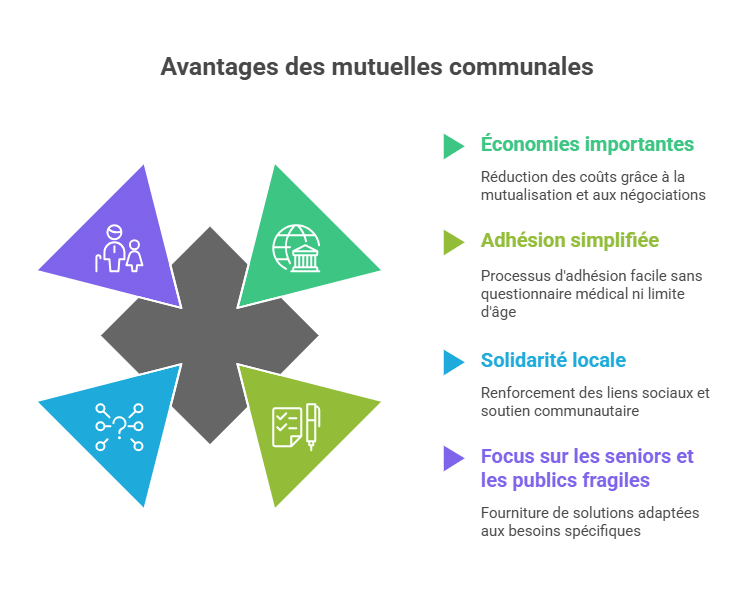

Advantages of municipal mutuals

The municipal mutuals provide numerous benefits, both financially and socially. This scheme improves healthcare access while strengthening community ties within towns.

1. Significant savings

One of the major strengths of municipal mutuals is cost reduction. Through membership pooling and negotiations by municipalities, contributions are often 30% to 60% lower than traditional mutuals. This saving allows families, retirees, and self-employed workers to benefit from comprehensive health coverage without straining their budgets.

2. Simplified procedures

Municipal mutuals are characterized by easy membership, making the scheme accessible to everyone:

- No medical questionnaire: No discrimination based on health background.

- No age limit: Retirees can join freely.

- Streamlined procedures: Registration can be completed directly at the town hall or CCAS.

This system avoids complex administrative formalities often seen as barriers to joining.

3. Local solidarity

Municipal mutuals strengthen the social bond among residents by offering a supportive and community-oriented solution. This scheme promotes mutual aid and allows everyone access to health coverage, regardless of their situation. Additionally, by relying on local structures like the town hall or CCAS, residents benefit from proximity services and personal assistance.

| Benefits | Description |

|---|---|

| 💰 Lower tariffs | Enable significant savings on contributions. |

| 📋 Simplified membership | No complicated administrative procedures. |

| 🤝 Community link | Strengthen solidarity among residents. |

🧓 Focus on seniors and vulnerable populations

Seniors and vulnerable individuals are among the primary beneficiaries of municipal mutuals. These schemes offer a tailored solution for specific medical needs related to age or financial hardship.

For retirees, the absence of medical questionnaires and age limits is a significant advantage. They can access a comprehensive and affordable coverage, even after their company mutual ends. Guarantees are often enhanced for areas like hospitalization, dental, or optical care.

People experiencing unemployment, low-income self-employed workers, and beneficiaries of CSS (Complementary Health Solidarity) also find in municipal mutuals a reliable alternative to maintain quality health protection without breaking their budget.

These schemes play a crucial social role by reducing inequalities in healthcare access across the territory.

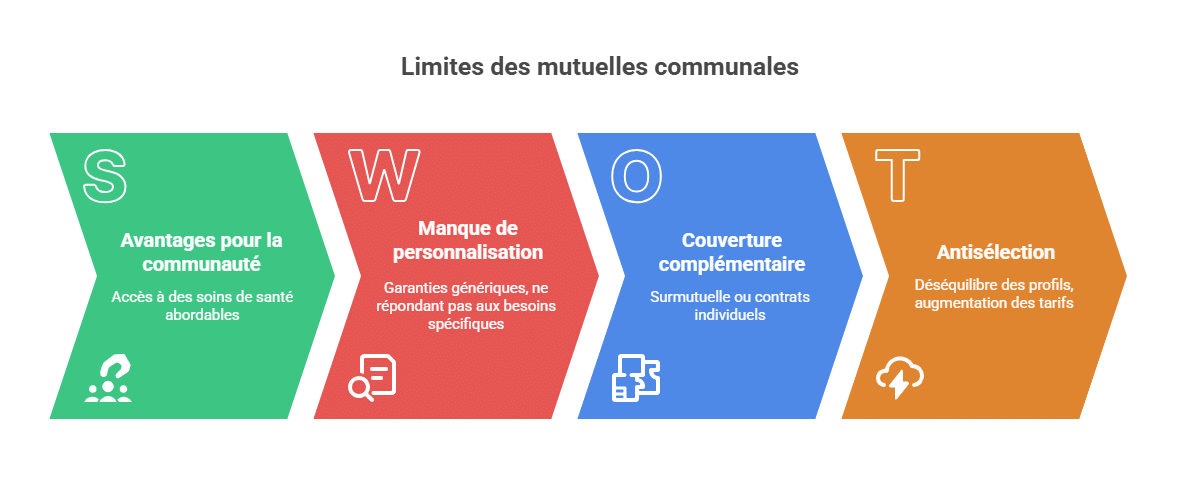

Limitations of municipal mutuals

Although municipal mutuals offer many advantages, they also have certain limitations that should be considered before subscribing.

1. Lack of guarantee personalization

The guarantees provided by municipal mutuals are often standardized, as they are negotiated for a large number of people. This means they aim to cover common needs but may not meet specific requirements, such as:

- Complex optical care (glasses with high correction).

- Expensive or non-standard dental prostheses.

- Specialized treatments not included in the overall contract.

Members with particular medical needs may need to supplement their coverage with a top-up or an individual contract, which can incur additional costs.

2. Risk of increasing contributions

The limited diversity of profiles among members is another disadvantage. Municipal mutuals often attract:

- Retirees, whose healthcare needs are higher.

- People with high-risk profiles (chronic illnesses, disabilities).

This low diversity can create an imbalance, as expenses incurred by some members may exceed the contributions collected, leading to a rate increase over time. This phenomenon, known as adverse selection, is especially pronounced in small towns with limited membership numbers.

| Limitations | Description |

|---|---|

| 🚫 Lack of personalization | Guarantees usually tailored to the majority but not to specific needs. |

| 📈 Risk of increases | Premiums may rise due to profile imbalance. |

List of municipal mutuals in France

Municipalities offering a municipal mutual

Municipal mutuals are expanding across many communes in France, allowing residents to benefit from advantageous rates and tailored guarantees. Here is a non-exhaustive list of towns and their specificities.

| Municipality | Partner mutual | Particularities |

|---|---|---|

| 🏘️ Béziers | Mon Béziers, Ma Santé | No medical questionnaire, free from the 3rd child. |

| 🌞 Nice | Nice Santé Proximité | Rates fixed for two years, no age limit. |

| 🌇 Toulouse | Actiom | Extended guarantees for retirees and students. |

| 🌊 Fréjus | Fréjus Solidarité | Enhanced coverage for optical and dental care. |

| 🏔️ Pessac | Pessac Mutualité | Six adapted plans, reductions of 40% on contributions. |

| 🌳 Bauvin | Bauvin Solidarité | Up to 30% savings, offers tailored for seniors. |

Municipal mutuals by region

| Region | Examples of towns |

|---|---|

| Île-de-France | Paris, Cergy, Orvault |

| Occitanie | Toulouse, Montpellier, Béziers |

| Nouvelle-Aquitaine | Pessac, Mérignac, Bordeaux |

| Provence-Alpes-Côte d’Azur | Nice, Fréjus, Saint-Raphaël |

| Grand Est | Reims, Metz, Strasbourg |

📝 How to convince your town hall to implement a municipal mutual

If your town does not yet offer a municipal mutual, it is entirely possible to initiate the process as a resident. Local elected officials are often receptive when a collective request is clearly and structurally presented.

Here are the key steps to persuade your town hall 👇

-

Gather information about the scheme: Understand its advantages and limitations to argue effectively with officials.

-

Build a small group of interested residents: The more the request is supported collectively, the more credible it is.

-

Write an official letter to the mayor or the inter-municipal council president.

-

Suggest a contact with a specialized association (e.g., ACTIOM) to facilitate implementation.

📄 Sample simple letter to address to the town hall:

Dear Mayor,

We are several residents of the town interested in establishing a municipal mutual. This scheme would allow everyone to access a health supplement at a preferential rate, while reinforcing local solidarity.

We thank you in advance for considering this possibility and remain available to discuss it.

Sincerely,

[Name, address]

How to join a municipal mutual?

Joining a municipal mutual is voluntary, simple, and open to all residents of the relevant town. Here are the steps and conditions needed to benefit from it.

Steps to join

- Visit the CCAS or town hall

The Centre Communal d’Action Sociale (CCAS) or your town hall is the first contact point. You will find all necessary information about the mutual offered and the procedures to follow. - Contact the partner mutual

Once informed, you can directly contact the partner mutual chosen by your town. They will explain the guarantees, contributions, and included services. - Fill out a simple registration form

Membership only requires filling out a basic form, without the need to provide complex proofs or medical questionnaires.

Membership conditions

Membership to a municipal mutual is accessible under flexible conditions that make it open to most people:

- Reside in the relevant municipality: Only residents of the municipality or inter-municipalities can subscribe.

- No age limit: Seniors, young people, and children are all eligible.

- No income limit: The scheme is open to everyone, regardless of income.

- Optional membership: You are not obliged to join even if you reside in a town offering a municipal mutual.

Why choose a municipal mutual?

- Easier accessibility: Short procedures and no restrictive conditions.

- Local proximity: Support directly within the town.

- Economy and solidarity: Reduced-cost health coverage supporting collective initiative.

🧮 Concrete cost-saving examples

Municipal mutuals allow for significant savings. Here are concrete examples illustrating the differences between an individual mutual and a municipal mutual 👇

| Profile | Town | Individual rate | Municipal rate | Annual savings |

|---|---|---|---|---|

| 👴 Retiree, 72 years old | Toulouse | 135 €/month | 85 €/month | 600 € |

| Family of 4 | Pessac | 310 €/month | 200 €/month | 1,320 € |

| Independent, 35 years old | Nice | 120 €/month | 80 €/month | 480 € |

These figures demonstrate the concrete financial impact that a municipal mutual membership can have, especially for profiles with modest incomes or retirees.

Conclusion

Municipal mutuals represent an innovative and solidarity-based solution to improve healthcare access while reducing coverage costs. By offering guarantees adapted at competitive rates, they enable many residents, especially retirees, self-employed workers, and students, to benefit from accessible health protection.

Easy to implement thanks to collaboration between towns and partner mutuals, they also strengthen the social bond and local solidarity. However, it is essential to carefully analyze the guarantees offered and ensure they match your specific needs.

If your town has not yet implemented a municipal mutual, consider proposing it to your town hall. These schemes are gaining popularity and could soon become a standard approach to improving health access at the local level.

🌐 Useful links and practical resources

To deepen your understanding or find the most suitable municipal mutual for your situation, here are some reliable resources:

-

🏛 ACTIOM — Association specialized in setting up municipal mutuals.

-

🤝 Mut’Com — Committed actor in local solidarity and collective negotiation.

-

📚 Public Service — Practical guides on health supplements and local schemes.

-

📝 PDF Guide for Municipalities — Support document for local elected officials (French National Federation of Mutual Societies).

❓ FAQ – Municipal Mutuals

📝 Can a municipal mutual be combined with an employer mutual?

Yes, it is possible to combine both under certain conditions. Employer mutuals remain mandatory for employees, but you can join a municipal mutual as a complement if you want to enhance certain coverage areas (optical, dental, hospitalization). This combination allows for better coverage for non-covered expenses.

👨👩👧 Are municipal mutuals reserved only for seniors?

No, these schemes are open to all residents of the town, regardless of age or income. Seniors make up a significant portion of members because they often lose their company health insurance, but students, self-employed workers, and families can also join for advantageous rates.

🏡 What happens if I move to another town?

In case of relocation, you must inform the municipal mutual. If your new town offers a similar scheme, you can transfer your membership easily. Otherwise, you can terminate your contract according to the specified terms (often with a one-month notice) and subscribe to another health supplement.

⏳ Are the costs of municipal mutuals guaranteed over time?

Generally, the rates are negotiated for a fixed period (usually 1 to 3 years) with the partner insurer. Afterward, a collective renegotiation is carried out to maintain the best conditions. However, like any health supplement, rates can adjust slightly depending on healthcare utilization and the profile of members.

🧮 Is it compatible with the Solidarity Health Complement (CSS)?

Yes, in some cases. If you benefit from free CSS, you typically do not need a municipal mutual. But if you are eligible for CSS with participation, the municipal mutual can sometimes be more advantageous depending on your profile and local rates. It is recommended to compare both options before making a choice.

📋 Is a medical questionnaire required to join?

No ✅, one of the main advantages of municipal mutuals is the absence of a medical questionnaire. No medical information is requested, which facilitates a simple and quick membership, even for high-risk profiles or those with chronic illnesses.

📅 When can I join a municipal mutual?

You can generally join at any time during the year, with no specific period. Some towns organize information campaigns at specific dates to centralize registrations and facilitate collective management.

Further information

Entraîne-toi avec nos Quiz de révision

Fini les lectures passives. Pour retenir les notions clés du BTS Assurance, teste-toi ! Inscris-toi pour recevoir 1 quiz par jour directement dans ta boîte mail.